The FTSE 100 is defying the gravitational pull of a sluggish Wall Street today, climbing 0.51% to trade at a record-breaking 10,233.82 as of mid-afternoon on January 15, 2026. While US tech stocks lick their wounds following a "clobbering" in the previous session, London has found its own rhythm, powered by a triple threat of resilient economic data, powerhouse banking earnings, and a de-escalation of geopolitical tensions.

The "Why" Behind the Rally: Key Drivers

1. The GDP Surprise

The primary catalyst was this morning’s release from the Office for National Statistics (ONS). UK GDP grew by 0.3% in November, comfortably beating the 0.1% consensus. This reversal of October’s stagnation suggests the UK economy is navigating the "higher-for-longer" rate environment with surprising grit.

2. Banking & Asset Management Tailwinds

While US banks disappointed, UK financials are thriving. Schroders set the tone today, surging over 6.4% after announcing that annual profits would exceed market expectations. This "halo effect" spread across the sector, with heavyweights like Barclays, Lloyds, and HSBC all tracking significantly higher.

3. The "Trump Peace Dividend"

Global markets caught a breather after U.S. President Donald Trump signaled a de-escalation regarding military action in Iran. This cooled the "fear trade," sending oil and gold prices lower, which—paradoxically—helped the broader FTSE by lowering input cost fears and stabilizing the pound.

Sector Heatmap: Winners and Losers

Source: Kalkine Group

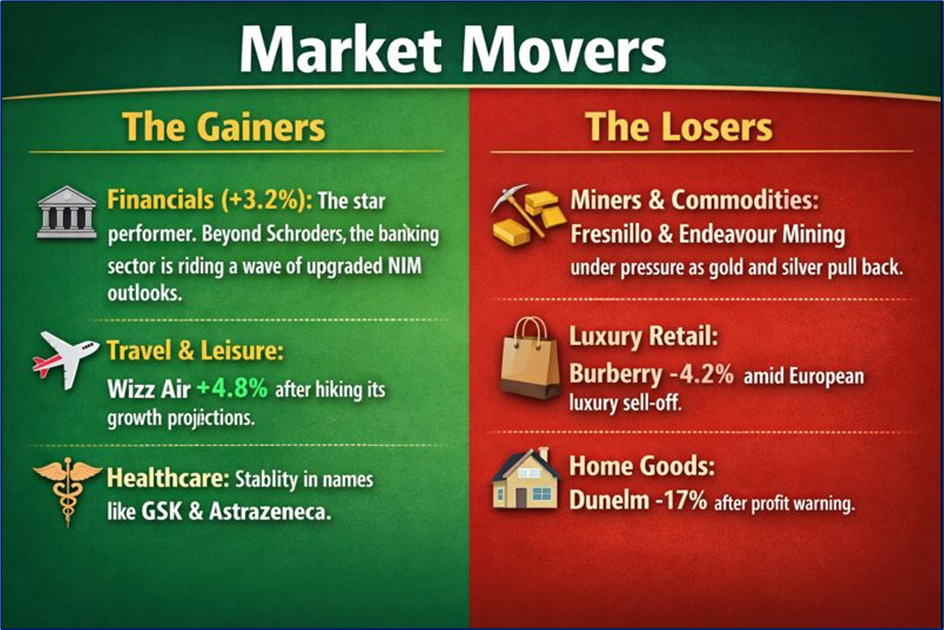

The Gainers

- Financials (+3.2%): The star performer. Beyond Schroders, the banking sector is riding a wave of upgraded net interest margin (NIM) outlooks.

- Travel & Leisure: Wizz Air climbed 4.8% after hiking its growth projections, signaling robust consumer demand for travel despite the macro-headwinds.

- Healthcare: Stability in names like GSK and AstraZeneca provided the defensive bedrock for the morning’s gains.

The Losers

- Miners & Commodities: A pullback in gold and silver hit the "safe haven" plays. Fresnillo and Endeavour Mining saw selling pressure as investors rotated back into growth.

- Luxury Retail: Burberry fell 4.2%, caught in a broader European luxury sell-off amid concerns over long-term discretionary spending.

- Home Goods: Dunelm cratered nearly 17% after a profit warning, citing a "challenging macroeconomic environment" and cautious shoppers.

Smart Money & Institutional View

The "Smart Money" is currently rotating. Hedge funds have reportedly been trimming "Mag Magnificent 7" exposure in the US and moving into "unloved" UK value stocks.

- J.P. Morgan Global Research: Remains positive on UK equities for 2026, citing a 3.4% forward dividend yield and a record £85.6 billion in expected dividend payments this year.

- AJ Bell: Russ Mould notes that the FTSE 100 is finally behaving as a "play on both global growth and inflation," packed with the cyclicals and commodity plays that thrive in the current environment.

Technical Analysis Summary

Source: Trading View

The FTSE 100 is in uncharted territory.

- Support: Firm support has formed at the psychological 10,000 level.

- Resistance: With the index hitting all-time highs, technical resistance is thin, though some analysts point to 10,250 as a short-term exhaustion point.

- RSI: The Relative Strength Index is creeping toward 75, suggesting the index is becoming "overbought," which may invite minor profit-taking by the week’s end.

Conclusion: Is the 10,500 Mark Next?

Today’s price action confirms that the FTSE 100 is no longer the "laggard of Europe." Between a massive buyback bonanza (over £7bn already announced for 2026) and a resilient UK consumer, the path of least resistance appears to be up. While individual retailers like Dunelm act as a warning sign, the index's heavy tilt toward banking and energy is currently its greatest strength.

Please wait processing your request...

Please wait processing your request...