The FTSE 250 Index is trading up 0.22% (approximately 22,941.07), showing resilience even as its blue-chip sibling, the FTSE 100, grapples with a massive retail slump. While the headlines are dominated by a potential "mega-merger" between mining giants Glencore and Rio Tinto, the mid-cap index is finding its own legs through robust shipping data and investment trust reshuffles.

Key Drivers: What’s Moving the Needle?

The primary catalyst today is a "risk-on" sentiment ahead of the US Non-Farm Payrolls report. Investors are cautiously optimistic that a "Goldilocks" jobs print could solidify expectations for further central bank rate cuts in 2026.

Closer to home, the mining sector is providing a halo effect. Although the Glencore-Rio talks are centered in the FTSE 100, the broader optimism for commodities has trickled down to mid-cap miners and resource-heavy investment trusts. Furthermore, a surprise profit upgrade from Clarkson has reinvigorated faith in global trade recovery.

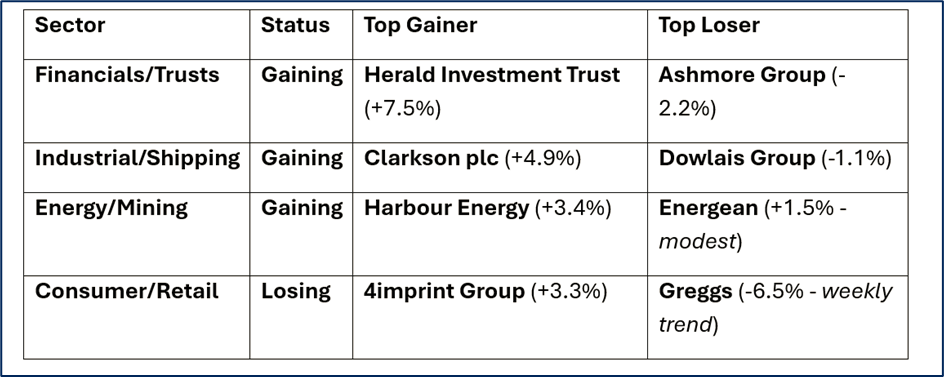

Winners & Losers: Sector Breakdown

Source: EODHD/Others, Kalkine Group

Stock Spotlight: The Biggest Movers

Source: Kalkine Group

The Gainers

- Herald Investment Trust (HRI): Up 7.52%. The standout performer after proposing a tender offer to buy back up to 100% of shares, a move aimed at narrowing its discount and satisfying activist shareholders like Saba Capital.

- Clarkson plc (CKN): Up 4.89%. The shipping services provider surged after guiding for 2025 underlying pretax profit "not less than £90 million," citing a very strong second half of the year.

- 4imprint Group (FOUR): Up 3.27%. Catching a bid on positive momentum in the advertising and promotional products space.

- Atalaya Mining (ATYM): Up 2.08%. Benefiting from the sector-wide mining rally and rising copper prices.

The Losers

- Greggs (GRG): Despite a flat daily start, the bakery remains under pressure (down 6.5% over the last 24 hours) after forecasting 2026 profits below analyst consensus earlier this week.

- Bellway plc (BWY): Down 1.28%. Housebuilders are seeing minor profit-taking today as investors rotate out of domestic cyclicals into global resource stocks.

- Derwent London (DLN): Down 1.54%. Real estate investment trusts (REITs) are dragging slightly as bond yields remain sensitive to upcoming US inflation data.

Analyst Corner: Upgrades & Downgrades

- Antofagasta: While a large-cap, its Goldman Sachs upgrade (Neutral to Buy, PT raised to 4,000p) has lifted the sentiment for all UK-listed copper miners, specifically aiding Atalaya Mining.

- Sainsbury’s: Facing heavy pressure after a holiday trading update showed General Merchandise sales fell 1.1%, leading to cautious notes from Citi and JP Morgan on the wider retail landscape.

- Greggs: Peel Hunt noted their 2026 outlook was "OK without being great," contributing to the stock's recent de-rating.

Technical Analysis Summary

Source: Trading View

The FTSE 250 is currently testing the upper bound of its 22,750 – 22,950 range.

- Support: Immediate support sits at 22,800. A break below this could see a retest of the 50-day SMA at 22,640.

- Resistance: The psychological barrier is 23,000. A daily close above this level would signal a technical breakout toward 52-week highs.

- RSI: Currently hovering around 75, suggesting the index is in "neutral-to-bullish" territory—not yet overbought.

Conclusion: A Tale of Two Markets

The FTSE 250 is successfully navigating a "split" market. While UK supermarkets and high-street bakers are feeling the pinch of a post-Christmas hangover, the more globally-exposed mid-caps—shipping, specialist mining, and investment trusts—are thriving. All eyes now turn to the US jobs data at 1:30 PM GMT, which will determine if this 0.22% gain holds or evaporates before the weekend.

Please wait processing your request...

Please wait processing your request...