The FTSE 250 (MCX) faced a challenging session today, trading down approximately 0.60% to 22,888.60 by midday. While the blue-chip FTSE 100 showed relative resilience, the more domestically focused mid-cap index buckled under the weight of mounting geopolitical tensions and a cautious "wait-and-see" approach from investors ahead of critical US inflation data.

The Market Pulse: Why is the FTSE 250 Falling?

The primary catalyst for today’s slide is a cocktail of US Federal Reserve uncertainty and domestic retail woes.

- The "Powell Probe" Rattles Sentiment: Markets globally are digesting news of a Justice Department investigation into Fed Chair Jerome Powell. The potential for political interference in US monetary policy has spiked volatility, hitting the sentiment-sensitive mid-cap space harder than the defensive heavyweights.

- Inflation Jitters: Investors are moving to the sidelines ahead of the US Consumer Price Index (CPI) release. With UK services inflation remaining "sticky," any upside surprise in the US could signal "higher-for-longer" rates globally, a nightmare scenario for mid-cap growth stocks.

- Retail Sector Drag: Dismal updates from the high street, notably a profit warning from Shoe Zone, have cast a shadow over consumer-facing stocks.

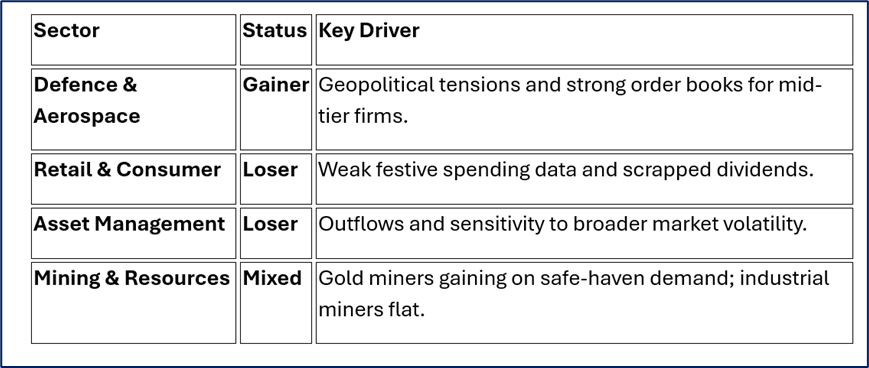

Sectors in Focus: The Tug-of-War

Source: Kalkine Group Analysis

Stock Scoreboard: Gainers and Losers

Source: Kalkine Group

Top Gainers

- Atalaya Mining (+5.2%): Benefiting from a slight recovery in copper sentiment and robust production forecasts.

- Ceres Power (+2.7%): Picking up momentum as green energy tech sees a speculative bid.

- Chemring Group (+1.3%): Continues its "defence super-cycle" rally with record order backlogs.

- Avon Technologies (+1.7%): Investor confidence remains high in protective equipment demand.

Top Losers

- THG (The Hut Group) (-4.6%): Despite reporting revenue growth, the stock succumbed to profit-taking after an initial early-session spike.

- B&M European Value (-4.1%): Retail sentiment soured following sector-wide concerns over 2026 margin pressures.

- Currys (-3.5%): Faced heavy selling as data showed a year-on-year decline in UK consumer spending.

- Close Brothers (-3.2%): Financial services remain under pressure amid regulatory uncertainty in the motor finance space.

Latest Analyst Intel: Upgrades & Downgrades

Institutional desks are recalibrating their portfolios for the first quarter of 2026:

- Upgrade: Rentokil Initial received a boost from Morgan Stanley, moving to 'Overweight' with a view that organic growth in North America will drive a re-rating.

- Downgrade: Auto Trader was cut to 'Hold' by Jefferies, citing limited catalysts for the used car market in the short term.

- Downgrade: DCC was moved to 'Equal Weight' by Morgan Stanley as the group transitions its energy business model.

Technical Analysis Summary: The 23,000 Battleground

Source: Trading View

From a technical perspective, the FTSE 250 is testing critical support levels.

- Resistance: The 23,036 level (yesterday's close) has turned into immediate resistance.

- Support: The index is currently hovering just above the 22,790 mark. A break below this could see a rapid descent toward the 22,500 psychological floor.

- RSI: The Relative Strength Index is trending toward 70, suggesting the index is losing its bullish momentum.

Conclusion: A Mid-Cap Crossroads

Today’s 0.60% drop reflects a market that is fundamentally "on edge." While the FTSE 100 flirts with five-figure records, the FTSE 250 is being squeezed by its closer ties to the UK consumer and its sensitivity to global interest rate ripples. For the index to rebound, we need to see a cooling of the Trump-Powell tensions and a US inflation print that allows the Bank of England to remain on its easing path.

Please wait processing your request...

Please wait processing your request...