Hostelworld Group PLC (LON: HSW) enjoyed a festive boost on December 24, 2025, with its shares climbing approximately 3.78% to close the half-day session at GBX 123.50. In a year of volatile leisure equities, this "social-first" travel agent is proving that its pivot from a simple booking engine to a community-driven platform is paying off for shareholders.

Key Drivers: Why the Stock Popped on Dec 24

The Christmas Eve rally wasn't just seasonal cheer; it was the culmination of several strategic tailwinds:

Source: Kalkine Group

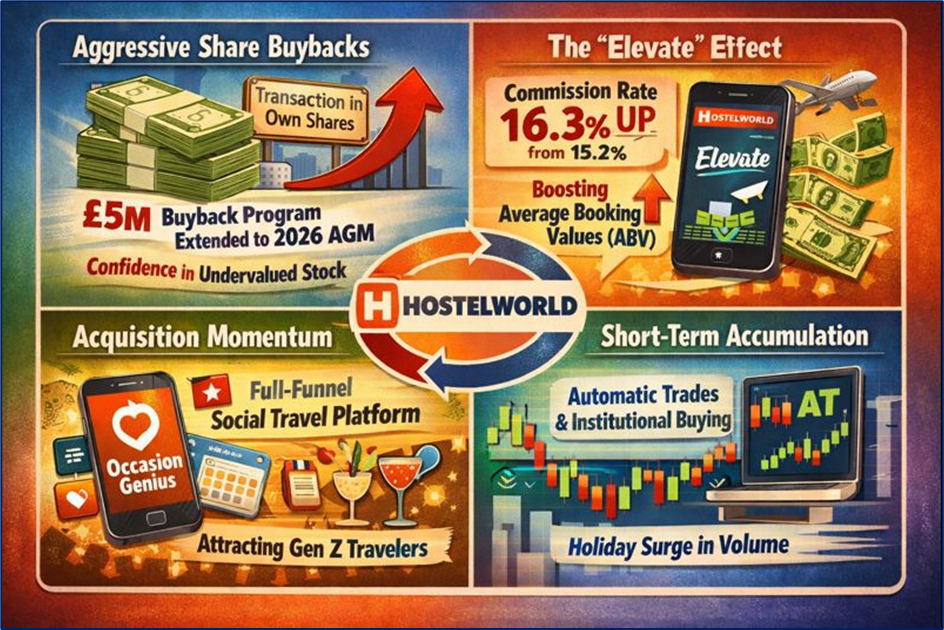

- Aggressive Share Buybacks: The company has been a consistent buyer of its own stock. On December 22 and 23, 2024, the Group executed further "Transaction in Own Shares" as part of its £5 million buyback program, which was recently extended until the 2026 AGM. This reduces share supply and signals management’s confidence that the stock is undervalued.

- The "Elevate" Effect: Hostelworld’s new marketplace tool, Elevate, has successfully pushed commission rates to 16.3% (up from 15.2% the previous year). This higher take-rate has boosted Average Booking Values (ABV), helping the stock shrug off a weaker US Dollar.

- Acquisition Momentum: The market is still digesting the October 2025 acquisition of OccasionGenius. By integrating event discovery into the app, Hostelworld is evolving into a full-funnel "Social Travel Platform," increasing the reasons for Gen Z travelers to stay within the ecosystem.

- Short-Term Accumulation: Market data indicates "Automatic Trades" (AT) and institutional accumulation during the thin holiday trading volume, amplifying the upward price movement.

Latest Business Model: More Than a Booking Site

Hostelworld has undergone a radical transformation. It no longer just sells beds; it sells connections.

Source: Company Data

2025 Financial & Operational Snapshot

The Group's recent trading update (Q3 2025) and interim results highlight a lean, cash-generative machine:

- Revenue Growth: Q3 generated revenue grew 5% YoY, driven by improved marketing efficiency.

- Profitability: Reaffirmed full-year Adjusted EBITDA guidance of ~€19.8m.

- Efficiency: Marketing costs fell to 47% of revenue in Q3, down from 51% in H1, as social features drive "organic" app-based bookings.

- Social Dominance: Social members reached ~3 million by late 2025. Impressively, 85% of all bookings are now made by social members, significantly lowering the cost of customer acquisition (CAC).

- Debt-Free Strength: The company returned to a net cash position (approx. €6.6m as of Q3), having repaid its pandemic-era debt early.

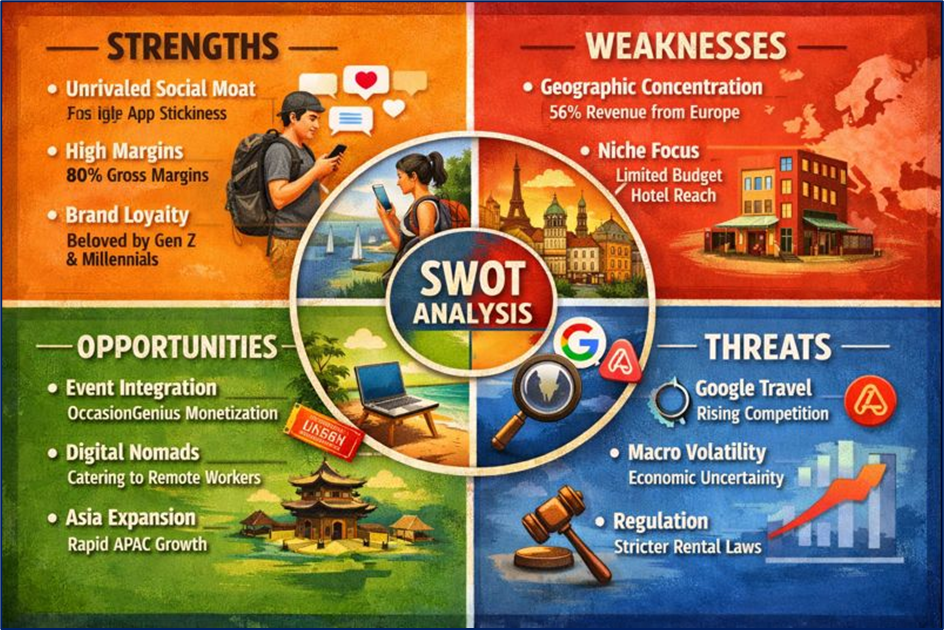

SWOT Analysis 2025

Source: Kalkine Group

Strengths

- Unrivaled Social Moat: The only OTA that effectively connects travelers socially, creating high app stickiness.

- High Margins: Asset-light model with gross margins near 80%.

- Brand Loyalty: Strong resonance with Gen Z and Millennial "solomooners."

Weaknesses

- Geographic Concentration: Over 56% of revenue is tied to Europe, making it sensitive to regional economic shifts.

- Niche Focus: While dominant in hostels, it faces uphill battles in the broader "budget hotel" segment.

Opportunities

- Event Integration: Monetizing the OccasionGenius acquisition via ticket sales and localized ad spend.

- Digital Nomads: Tailoring inventory for long-stay remote workers who prioritize community.

- Asia Expansion: Asia-Pacific remains the fastest-growing hostel market globally.

Threats

- Google Travel: Increased competition in the search funnel from Google and Airbnb.

- Macro Volatility: Inflation affecting the discretionary spending of young travelers.

- Regulation: Changing short-term rental laws in major European cities (e.g., Barcelona, Lisbon).

Key Risks to Watch

Investors should remain cautious regarding:

- Consumer Sentiment: A potential 2026 slowdown in the UK/EU could hit booking volumes.

- Tech Execution: The successful rollout of "Social Monetization" in Q4 2025 and Q1 2026 is critical to meeting growth targets.

- M&A Integration: Ensuring the OccasionGenius platform scales without diluting the core user experience.

Conclusion

Hostelworld’s 3.7% jump on Christmas Eve reflects a company that has successfully navigated its post-pandemic recovery and is now leaning into its unique "social" identity. By combining a share-buyback floor with rising commission rates and a debt-free balance sheet, HSW is positioning itself as a premium small-cap play in the travel sector. While macro risks persist, the data suggests that for the youth travel market, the "social" strategy is the engine of the future.

Please wait processing your request...

Please wait processing your request...