International Consolidated Airlines Group (LSE: IAG) kicked off 2026 with a confident ascent, seeing its shares climb ~1.38% to reach 420 GBX during the Jan 2 trading session. This follows a blockbuster 2025 where the stock surged nearly 40%, recently touching a new 52-week high of 430.60 GBX.

For retail investors, the story isn't just about "post-pandemic recovery" anymore—it’s about a high-margin, cash-generative machine that is outperforming the broader FTSE 100.

Key Drivers: What Pushed the Needle on Jan 2?

Source: Kalkine Group

The New Year rally was fueled by a combination of sector-wide optimism and specific financial milestones:

- Sector Momentum: Broader European airline strength provided a tailwind as travel demand for the 2026 summer season showed early signs of record-breaking bookings.

- Technical Breakout: Shares consistently stayed above the 200-day moving average, triggering "buy" signals for algorithmic and momentum traders as the stock approached its 52-week peak.

- Cheap Valuation: Despite the 40% gain in 2025, IAG entered 2026 with a P/E ratio of approximately 6.4x–7.9x, significantly lower than historical averages and its US peers, making it a "Value Score B" favorite for institutional buyers.

- Shareholder Returns: The completion of a €1 billion share buyback program and a 45% increase in interim dividends (paid out in late 2025) have fundamentally re-rated the stock as a "yield play" rather than just a cyclical gamble.

The 2026 Business Model: More Than Just Planes

IAG has moved away from the traditional airline model to a "Platform Structure."

- Portfolio Diversification: Instead of a single brand, IAG operates a "house of brands" including British Airways (Premium/Global), Iberia (Latin America lead), Vueling (Low-cost Europe), and Aer Lingus (North Atlantic value).

- The Avios Engine: IAG Loyalty is now a powerhouse. By decoupling loyalty from seat sales, they’ve created a high-margin, recurring revenue stream through 125+ partners and 40 million+ collectors.

- Transatlantic Dominance: IAG controls the most profitable "corridor" in the world—the North Atlantic—accounting for roughly 40% of its revenue.

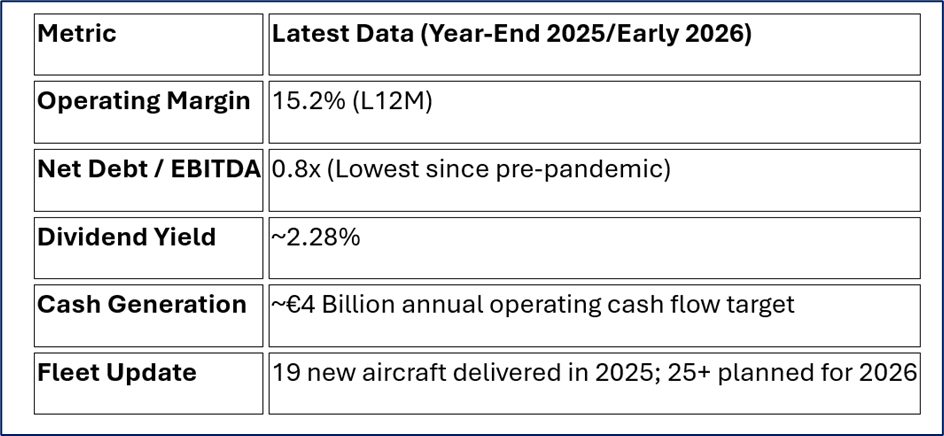

Financial & Operational Pulse Check

Source: Company Data

SWOT Analysis: The 2026 Outlook

Source: Kalkine Group

Strengths

- Unrivaled Hubs: Dominance at London Heathrow and Madrid Barajas.

- Balance Sheet: Leverage at 0.8x is "best-in-class" for European legacy carriers.

- Cost Discipline: Non-fuel unit costs have remained flat despite global inflation.

Weaknesses

- Transatlantic Concentration: 40% revenue reliance on one corridor makes it vulnerable to US economic shifts.

- Labor Relations: Complex multinational unions (BA and Iberia) remain a constant risk for industrial action.

Opportunities

- Sustainable Aviation Fuel (SAF): Strategic investments (e.g., OXCCU) position IAG to lead as EU regulations tighten.

- Digital Transformation: A €1.5 billion tech overhaul is currently streamlining baggage and check-in to boost margins.

Threats

- Regulatory Squeeze: Rising costs at Heathrow (Third Runway project) and EU "Green" taxes.

- Geopolitical Volatility: Recent bans in Venezuela and tensions in the Middle East affect specific route yields.

The Risk Radar

While the stock is "flying high," three main clouds sit on the horizon:

- Yield Softening: While premium cabins are full, "Economy Leisure" pricing has shown signs of softening as the "revenge travel" era finally cools.

- Fuel Volatility: Any spike in Brent Crude could eat into the record 20% margins.

- Infrastructure Costs: The Civil Aviation Authority (CAA) is currently reviewing the "JFK model" for Heathrow, which could lead to higher airport charges for BA.

Conclusion

IAG enters 2026 no longer as a "recovery play," but as a lean, cash-generative leader in the FTSE 100. The 1.4% bump on Jan 2 reflects a market that is beginning to price in a permanent shift in the company's profitability profile. With low valuation multiples and high shareholder returns, the "ceiling" for this stock may still be higher than 2025's peaks.

Please wait processing your request...

Please wait processing your request...