Why Investors Are Obsessed with BAB Stock Right Now

The defense sector has shifted from a stable background industry into a high-octane growth engine, and Babcock International (BAB) is sitting at the absolute epicenter of this transformation. As geopolitical tensions recalibrate global budgets, this British engineering powerhouse has evolved from a restructuring story into a genuine FTSE 100 outperformer.

With a staggering 600% share price surge under outgoing leadership and a multi-billion pound contract backlog, the question isn’t just whether Babcock is growing—it’s how high the ceiling goes in a world demanding "Sovereign Defence" and "Industrial Resilience." This is the breakdown of the latest financial updates, the CEO transition, and the strategic drivers making BAB the stock everyone is talking about in January 2026.

Will the Defence Super-Cycle Keep Propelling Babcock Higher in 2026?

- The short-term outlook for the defense sector over the next 3 to 6 months remains exceptionally robust as European and UK governments prioritize strategic autonomy. With NATO members pushing toward a 3% or even 3.5% GDP spending target, the "total addressable market" for firms like Babcock is expanding at an unprecedented rate.

- Babcock’s specific sector coverage highlights a "Golden Era" for Nuclear and Marine divisions. The Nuclear sector is currently the group's "star pupil," hitting a 9.1% margin driven by submarine support and clean energy projects (Babcock Q3 Trading Update).

- In the Marine sector, the Type 31 Frigate programme at Rosyth is moving at pace, with the third ship, HMS Formidable, having its keel laid recently. This steady execution is providing the "predictable growth" that institutional investors crave in a volatile market.

- Aviation is finally stepping into the spotlight, fueled by the ramp-up of the French Mentor 2 contract, proving that Babcock's turnaround is firing on all cylinders across its diversified portfolio.

Source: Kalkine Group

What Should Retail Investors Watch Closely as the CEO Guard Changes?

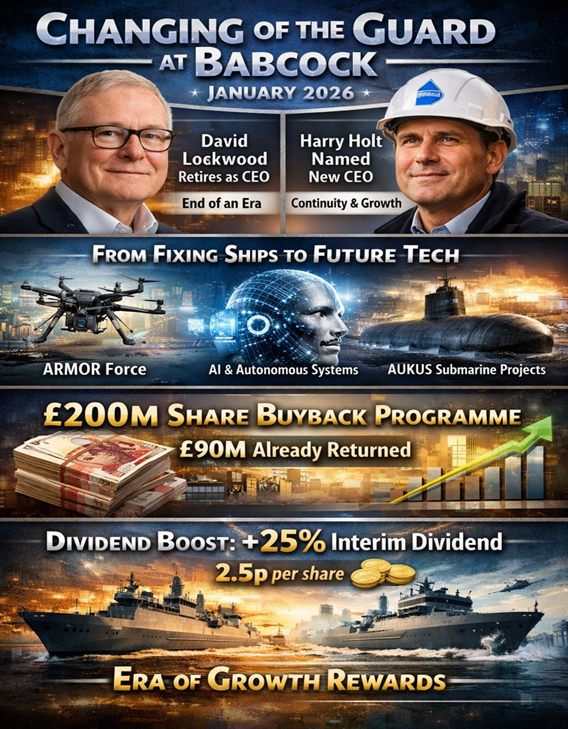

- The biggest news of January 2026 is the retirement of CEO David Lockwood and the appointment of Harry Holt, the current Nuclear chief, as his successor. For retail investors, this transition is a "continuity play" rather than a pivot, as Holt has already led the company's highest-performing division.

- The current business model is shifting toward high-margin, technology-led engineering. Babcock isn't just "fixing ships"; it’s integrating AI, autonomous systems like the ARMOR Force initiative, and complex submarine assemblies for the AUKUS partnership.

- Actionable insights for observers: The company is currently halfway through a £200 million share buyback programme, with £90 million already returned to shareholders (Company Source: Q3 Trading Update). This indicates a management team confident in its cash flow and committed to "shareholder value creation."

- Dividend growth is a key driver. The interim dividend was recently hiked by 25% to 2.5 pence, signaling that the era of "restructuring caution" is over and the era of "growth rewards" has begun.

Is the Bull Case Overwhelming the Bear Fears for BAB?

- The Bullish View: Analysts are largely leaning bullish, citing the company’s "Strong Buy" technical signals and an average price target nearing 1,525p. The momentum is supported by a £9.9 billion contract backlog and a clear path to an 8% operating margin by the end of FY26.

- The Neutral/Bearish View: Some analysts remain cautious, pointing to the "subdued" activity in the Land (Rail) sector and the inherent risks of long-term government contracts where cost overruns can eat into margins.

- Operational Momentum: The recent selection of Babcock as the prime partner for Indonesia’s £4 billion Maritime Partnership Programme adds a significant "international upside" that wasn't fully priced in by some laggard models.

What Are the Latest Financial and Operational Breakthroughs?

- Revenue Growth: Organic revenue grew by 7% in the first half of the year, underpinned by a 31% jump in submarine support activity (Source: HY2026 Results).

- Margin Expansion: Underlying operating margins have climbed to 7.9%, a 90-basis point increase, putting the company within touching distance of its medium-term 9%+ target.

- Operational Wins: Beyond the UK, the partnership with HII to build components for US Virginia-class submarines marks a massive step into the American supply chain, diversifying revenue away from purely UK Ministry of Defence (MoD) spending.

How Does the Latest SWOT Analysis Shape the Outlook?

- Strengths: Massive "moat" in nuclear and naval engineering; record order intake in the LGE business; strong relationship with the UK MoD.

- Weaknesses: Subdued performance in the Land/Rail division; transition risks associated with the CEO change.

- Opportunities: Expansion into the AUKUS supply chain; further Arrowhead 140 license sales to international navies; AI-driven maintenance diagnostics.

- Risks: Geopolitical shifts that could alter defense priorities; high sensitivity to UK government fiscal policy; skilled labor shortages in specialized engineering.

Can Babcock Maintain Its Viral Momentum Throughout 2026?

The narrative surrounding Babcock has fundamentally changed. No longer a struggling legacy firm, it is now a lean, high-tech defense leader with its sights set on global expansion. With the Indonesia deal providing a potential "valuation kicker" and the AUKUS partnership providing a decade-long floor for revenue, the market is watching closely to see if Harry Holt can accelerate the momentum David Lockwood started. Whether it's the 25% dividend hike or the £200m buyback, the signals coming out of Rosyth and Devonport suggest a company that knows exactly where it’s going.

Please wait processing your request...

Please wait processing your request...