The Intelligent Investor’s Pulse: Analysts Weigh in on WTB’s Rally

Whitbread PLC (WTB) has emerged as a standout performer in the FTSE 100 today, jumping over 5% following a robust third-quarter trading update. Fund managers and investment banks are closely scrutinizing the stock as it navigates a complex macro environment. The sentiment from major institutions like Morgan Stanley and Deutsche Bank leans toward a "Moderate Buy," driven by better-than-expected resilience against UK tax headwinds and a surging German division.

While activist investor Corvex Management has previously pushed for strategic changes, the latest data suggests management is already squeezing higher efficiencies out of the existing portfolio. For retail investors, the central question is whether this rally is a "relief bounce" or the start of a sustained re-rating as the company nears a critical profitability milestone in Germany.

Key Drivers and Strategic Catalysts

Source: Kalkine Group

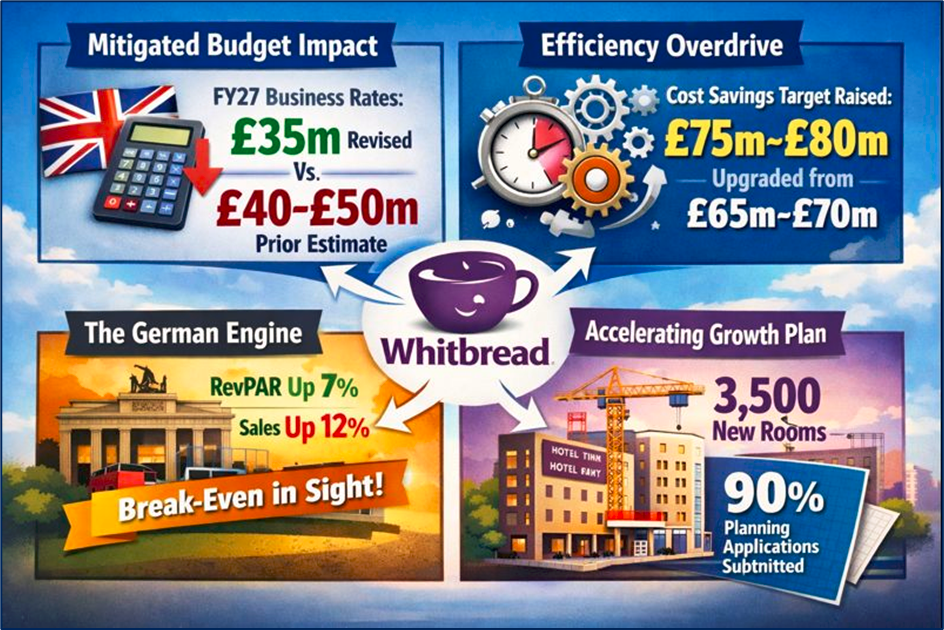

- Mitigated Budget Impact: A primary driver for today’s spike is the downward revision of expected UK business rate costs. Management now anticipates a £35 million hit for FY27, significantly lower than the prior fear-inducing estimate of £40–£50 million.

- Efficiency Overdrive: Whitbread has upgraded its FY26 cost-efficiency target to £75m–£80m (up from £65m–£70m), proving its ability to protect margins through procurement and technology despite labor cost inflation.

- The German Engine: Premier Inn Germany is no longer just a "future hope." With RevPAR (Revenue Per Available Room) up 7% and accommodation sales surging 12%, the division is on the cusp of break-even, a massive psychological and financial win for the group.

- Accelerating Growth Plan (AGP): The strategic pivot to convert lower-returning restaurants into high-margin hotel extensions (aiming for 3,500 new rooms) is ahead of schedule, with 90% of planning applications already submitted.

Technical Analysis: Breaking the Resistance

From a technical perspective, Whitbread has staged an aggressive breakout from its recent consolidation zone. The stock had been languishing near the 2,550p support level but today’s high-volume move has pushed it toward the 2,700p mark.

The Relative Strength Index (RSI) is trending upward but remains below overbought territory, suggesting there is still "room to run." Traders are eyeing the 2,820p level—a previous area of structural resistance—as the next major target. A sustained close above this could open the door for a retest of the 52-week high near 3,300p. However, the 50-day moving average remains a key trailing indicator to watch for any signs of momentum exhaustion.

Analyst Scorecard: Upgrades, Downgrades, and Targets

- Morgan Stanley: Reaffirmed Buy rating with a price target of 3,100p, citing "improving trading momentum and earnings upside."

- Deutsche Bank: Recently adjusted to Hold (down from Buy) due to broader UK budget concerns, but acknowledged the strong operational execution.

- JPMorgan: Maintains a Neutral/Hold stance with a price target of 2,815p, taking a more cautious view on UK consumer discretionary spending.

- Consensus View: Out of 7 major analysts, the consensus remains a Moderate Buy with an average price target of approximately 3,194p, representing a potential upside of over 15% from current levels.

Business Model and Financial Health

Whitbread operates a vertically integrated model, which is rare in the hotel industry. Unlike "asset-light" competitors like IHG or Marriott, Whitbread owns the majority of its property, giving it total control over the customer experience and the ability to extract value through sale-and-leaseback transactions.

- Latest Dividend: The board maintained a steady interim dividend of 36.4p, with analysts forecasting a full-year payout of approximately 101p (a 4.1% increase).

- Valuation: WTB currently trades at a forward P/E of roughly 19x, which is a premium to some peers but reflects its dominant UK market share and property-backed balance sheet.

- Share Buybacks: The company is aggressively returning capital, currently executing a £250 million share buyback program slated for completion by April 2026.

- Operations: Total Group sales rose 2% in Q3 to £781 million, with UK RevPAR climbing 3% (led by a 7% surge in London).

The Risks: What Could Trip Up the Bull Run?

- UK Consumer Fatigue: While travel demand has been "sticky," any sharp downturn in UK household disposable income could impact the high-margin leisure segment.

- Labor Inflation: The hospitality sector remains highly sensitive to minimum wage increases, which continue to pressure the bottom line.

- Execution Risk in Germany: While momentum is positive, the German market is highly competitive; any delay in reaching full-year profitability could sour investor sentiment.

- Regulatory Pressure: Management continues to lobby against UK government business rate changes, but further fiscal tightening remains a persistent threat.

Conclusion: The Smart Money Verdict

The "smart money" appears to be rewarding Whitbread for its operational discipline and its proactive stance on cost-cutting. By successfully navigating the UK budget fallout better than feared, Whitbread has repositioned itself as a defensive growth play within the FTSE 100. For investors seeking a combination of property backing, a growing dividend, and a clear international expansion story, the current entry point remains attractive to those with a medium-to-long-term horizon. However, the stock's sensitivity to UK fiscal policy means it is not without volatility.

Please wait processing your request...

Please wait processing your request...