On Jan 2, 2026, Kingfisher PLC (LSE: KGF) shares gained 1.18% to close at GBX 316.40, outperforming the broader FTSE 100 which rose by a modest 0.20%. This movement signals a resilient start to the year for the home improvement giant behind B&Q and Screwfix.

The retail sector has been a battlefield of shifting consumer sentiment, but Kingfisher is emerging as a "lean, green, digital machine." Here is the breakdown of why the stock is moving and what the business looks like in early 2026.

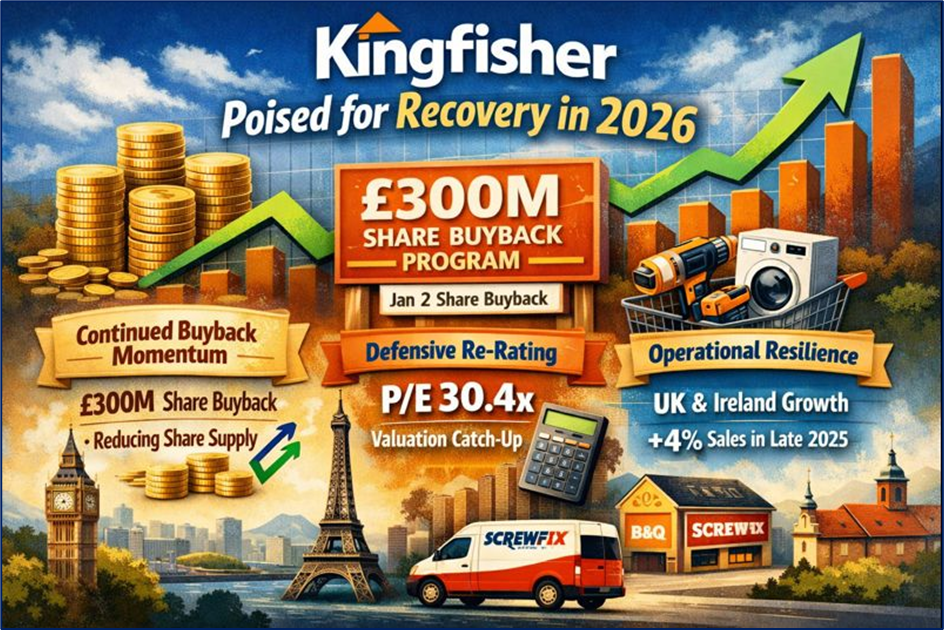

1. Key Reasons & Drivers (Jan 2, 2026)

Source: Kalkine Group

The 1.18% uptick was primarily driven by:

- Continued Buyback Momentum: Kingfisher confirmed a "Transaction in Own Shares" on Jan 2, part of its £300 million share buyback program. This consistent reduction in share supply continues to support the stock price.

- Defensive Re-rating: After a "Reduce" consensus from analysts in late 2025, the stock started 2026 with a valuation catch-up. Trading at a P/E ratio of approximately 30.4x (based on trailing earnings), investors are beginning to price in a recovery in "big-ticket" items.

- Operational Resilience: While markets in France and Poland remain soft, the UK & Ireland banners (B&Q, Screwfix) showed 4%+ growth in late 2025, providing a solid foundation for the new year.

2. The 2026 Business Model: "Powered by Kingfisher"

Kingfisher has moved away from being a loose collection of retail brands to a centralized, tech-driven powerhouse.

- The 50/50 Split: The business is now balanced between DIY (Do-it-Yourself) and DIFM (Do-it-For-Me/Trade). Trade sales (Screwfix, TradePoint) now represent nearly 30% of group sales.

- E-commerce Marketplace: B&Q’s marketplace now hosts over 2.1 million SKUs, contributing to an e-commerce penetration rate of roughly 20%.

- Own Exclusive Brands (OEB): Kingfisher generates £5.5bn (approx. 44% of sales) from its own brands (e.g., Magnusson, Erbauer). These carry higher margins than third-party brands and are a key profit driver.

3. Latest Financial & Operational Updates

- Profit Guidance: Management recently upgraded its adjusted profit before tax (PBT) guidance to between £540m and £570m for the 2025/26 fiscal year.

- Dividend Yield: The stock offers an attractive expected dividend yield of ~3.9%, making it a favorite for income-seekers in a volatile market.

- Expansion: Screwfix continues its aggressive push into France (targeting 600 stores) and Poland, diversifying the revenue stream away from the UK housing market.

4. SWOT Analysis (2026 Perspective)

Source: Kalkine Group

5. Key Risks to Watch

- Macro-Economic Sensitivity: Home improvement is highly cyclical. If interest rates do not fall as expected, consumers may continue to delay major kitchen or bathroom renovations.

- Geopolitical Friction: With a large footprint in France, national strikes and political uncertainty remain a "wildcard" for operational costs and consumer footfall.

- Cost Headwinds: The business is fighting a £145m headwind from higher wages and taxes (including UK National Insurance increases), which it hopes to offset via its "lean" productivity program.

Conclusion

Kingfisher's 1.2% rise on the first trading Friday of 2026 reflects a company that has successfully navigated the post-pandemic slump by pivoting toward trade professionals and digital marketplaces. While the high debt levels and sluggish European markets demand caution, the aggressive share buybacks and upgraded profit guidance suggest that the "B&Q owner" is building a much more durable house than it had two years ago.

Please wait processing your request...

Please wait processing your request...