On January 6, 2026, Ocado Group (LSE: OCDO) emerged as the top performer on the FTSE 250, closing up approximately 11.6%.

This surge reflects a pivot in investor sentiment as the company transitions from a high-burn growth story to a focused technology licensor nearing financial maturity.

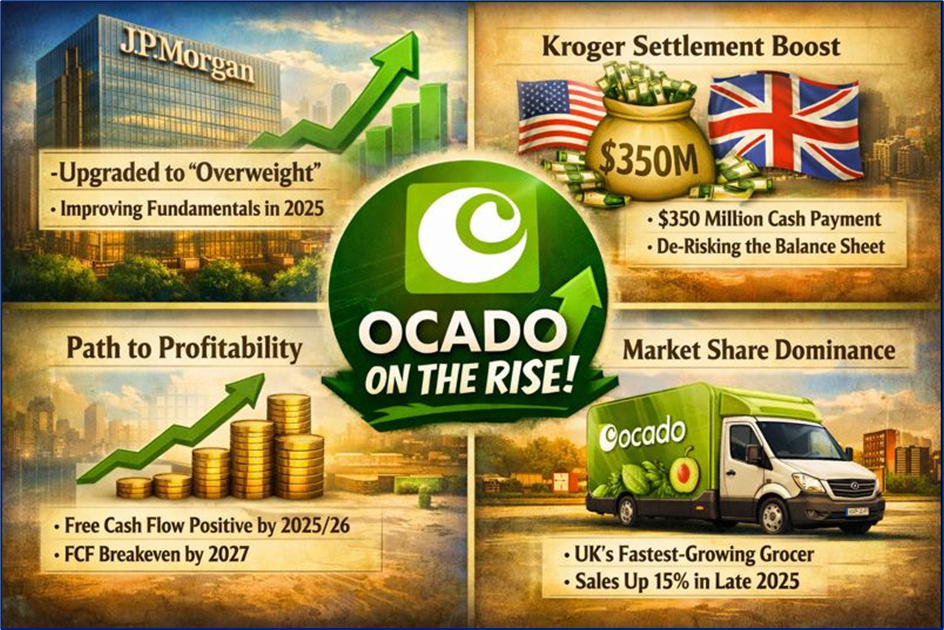

Key Reasons for the Jan 6 Surge

Source: Kalkine Group

The double-digit rally was driven by a "perfect storm" of broker upgrades and operational clarity:

- JPMorgan 'Positive Catalyst Watch': The bank placed Ocado on a "positive catalyst watch," upgrading the outlook to 'Overweight.' JPM highlighted that the stock’s volatility in 2025 had masked improving fundamentals.

- Kroger Settlement Liquidity: Investors cheered the confirmation of a $350 million (£260m) one-off cash payment from US giant Kroger, expected this month (Jan 2026). This compensates for the closure of three fulfillment centers and significantly de-risks the balance sheet.

- Path to Profitability: Management reiterated that the group is on track to be Free Cash Flow (FCF) positive by the 2025/26 financial year, with full-year FCF breakeven targeted for 2027.

- Market Share Dominance: Fresh data from Worldpanel by Numerator showed Ocado remains the UK’s fastest-growing grocer, with sales up 15% in the 12 weeks to late December 2025—outpacing rivals like Tesco and Sainsbury’s.

Latest Business Model & Strategy

Ocado has evolved from a British online grocer into a global Technology Solutions provider.

- Ocado Smart Platform (OSP): The "crown jewel." Ocado licenses its end-to-end robotic and AI software to 13 global partners (e.g., AEON in Japan, Coles in Australia, Kroger in the US).

- End of Exclusivity: As of late 2025/early 2026, Ocado has ended mutual exclusivity with most partners. This allows them to sell their tech to multiple retailers in the same country, vastly increasing their Total Addressable Market (TAM).

- Hardware-as-a-Service: Moving toward more modular, flexible automation (like the "600 Series" bot) that can be fitted into existing warehouses, not just massive new builds.

Financial & Operational Updates

- Cash Position: The $350m Kroger payment provides a vital buffer after a year of heavy CAPEX.

- Operational Scale: There are now 26 automated Customer Fulfillment Centers (CFCs) live globally, with over 1,000 stores using Ocado’s in-store fulfillment (ISF) software.

- Efficiency Gains: New "Re:imagined" robotics have increased picking speeds to over 2,500 items per hour, roughly 5x faster than manual picking.

SWOT Analysis (2026)

Source: Kalkine Group

Risks to Consider

While the Jan 6 rally is significant, several hurdles remain:

- Execution Risk: Transitioning to FCF positive requires flawless execution of the 80+ CFCs currently in the pipeline.

- US Saturation: While exclusivity has ended, the US market is becoming crowded with local automation startups.

- Valuation Sensitivity: Ocado remains a "growth" stock; any hint of a slowdown in new partner signings often leads to sharp sell-offs.

Conclusion

The 12% jump on January 6, 2026, marks a transition for Ocado. It is no longer just a "promising" tech firm but one that is finally collecting the "rent" on its global infrastructure. With the Kroger settlement providing a cash bridge and retail sales booming, the market is beginning to price in a future where Ocado is a self-sustaining tech powerhouse rather than a cash-burning experiment.

Please wait processing your request...

Please wait processing your request...