The London Stock Exchange opened its 2026 doors with a bang for Oxford Biomedica (LSE: OXB). On January 2, the stock climbed approximately 6%, hitting new 12-month highs and leaving retail investors asking: Is this the start of the "Great Biotech Recovery" or a calculated valuation correction?

As a leading Cell and Gene Therapy (CGT) Contract Development and Manufacturing Organisation (CDMO), Oxford Biomedica has spent the last 24 months pivoting its business model. Today, that discipline is finally reflecting on the ticker.

The "January Jump": Key Drivers Behind the 6% Surge

Source: Kalkine Group

The market reaction on January 2, 2026, isn't just a random fluctuation. It is the culmination of three specific tailwinds:

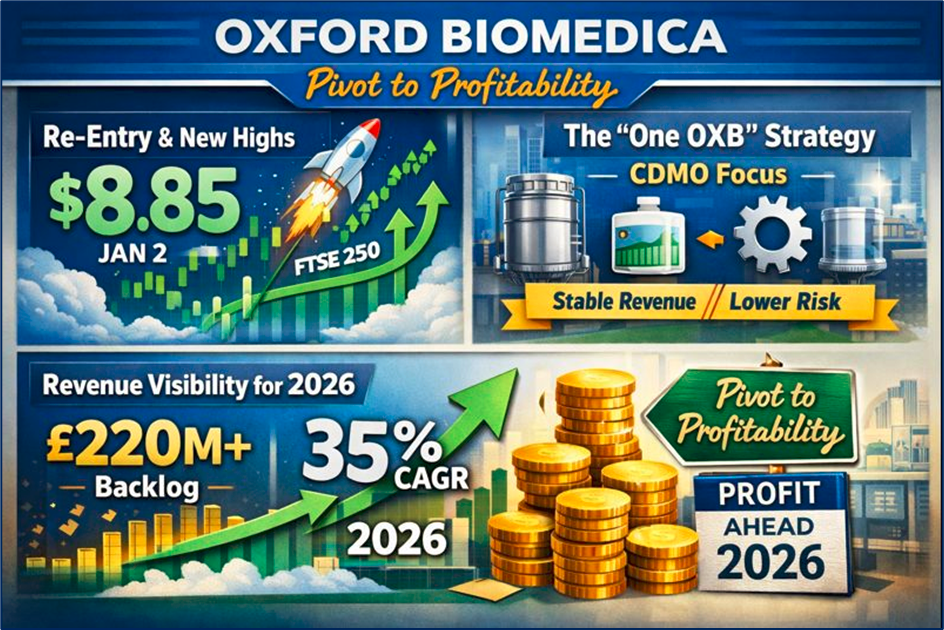

- Re-entry Sentiment & New Highs: Following its re-entry into the FTSE 250 in late 2025, OXB has seen increased institutional "buy-in" from trackers. On Jan 2, the stock breached a psychological resistance level, hitting a 52-week high of approximately $8.85 (OTCMKTS: OXBDF) and corresponding highs on the LSE.

- The "One OXB" Strategy Gains Velocity: Investors are responding to the company's shift from a hybrid (drug developer + manufacturer) to a pure-play CDMO. This move has removed the high-risk "binary" R&D failure risk, replacing it with a predictable, fee-for-service revenue stream.

- Revenue Visibility for 2026: With a revenue backlog exceeding £220 million reported late last year and a 35% CAGR target for 2023–2026, the market is pricing in the "Pivot to Profitability" expected this fiscal year.

The 2026 Business Model: From "Hybrid" to "Heavyweight"

Oxford Biomedica has successfully shed its skin. Its latest business model is built on three pillars:

- Multi-Vector Excellence: No longer just the "Lentiviral company," OXB now commands a significant share in AAV (Adeno-Associated Virus) and Adenovirus sectors.

- Global Footprint: With the full integration of sites in France (OXB France) and the recently acquired North Carolina facility in the US, OXB provides a "bridge" for biotechs to move from European clinical trials to US commercial launches.

- Asset-Light Innovation: Instead of spending hundreds of millions on their own drugs, they license their TetraVecta™ system and Process C technology to others, earning royalties and milestones without the clinical trial risk.

Financial & Operational Update: The Road to Black Ink

- Revenue & Profitability

- 2026 Revenue Guidance: Management has reiterated a target of £220M – £240M for the 2026 fiscal year.

- The Profit Pivot: After years of EBITDA losses, OXB is forecast to be EBITDA positive in 2025/2026, with medium-term margins targeted at >20%.

- Order Book Momentum: New client orders signed in the last half-year totaled £149 million, a 166% increase year-on-year.

- Operational Expansion

- US Scale-Up: The Durham, NC site is expected to be fully GMP-operational for AAV manufacturing by Q1 2026, capturing the lucrative US market.

- France Integration: The AAV platform transfer to French sites is on track for completion in the first half of this year.

2026 SWOT Analysis: A Strategic Deep Dive

Source: Kalkine Group

Critical Risks to Watch

Despite the 6% rally, the biotech sector remains a "high-conviction" play with inherent risks:

- Utilization Rates: The company has invested heavily in capacity (Capex of ~£60M for 2026-27). If the global biotech funding winter returns, these suites may sit idle.

- Execution Risk: Transitioning the newly acquired US sites to OXB’s proprietary "Process C" technology must be seamless to maintain client trust.

- Regulatory Changes: Any shifts in FDA or EMA requirements for viral vector purity could necessitate expensive retrofitting.

Conclusion

Oxford Biomedica’s 6% jump on January 2, 2026, reflects a market that is finally beginning to value operational stability over R&D hype. By transforming into a global, multi-vector CDMO with a clear path to profitability, OXB has positioned itself as a "picks and shovels" play for the gene therapy revolution.

Please wait processing your request...

Please wait processing your request...