Paragon Banking Group (LSE: PAG) started the 2026 trading year with a notable 2% climb on January 6th, defying the broader market's cautious tone. As mid-cap lenders face a tug-of-war between high interest rates and regulatory headwinds, Paragon appears to be carving out a "specialist's edge.

Here is a deep dive into the drivers, the latest operational data, and the risk-reward profile of this specialist banking powerhouse.

The 2% Catalyst: Why the Move Today?

Source: Kalkine Group

While no single "blockbuster" RNS was released this morning, the 2% uptick is widely attributed to a "catch-up" trade following several key updates:

- Ongoing Share Buybacks: The group has been aggressively active in its £50 million share repurchase program for FY26. Frequent "Transaction in Own Shares" notifications in early January have provided a steady floor for the stock price.

- Broker Upgrades: Analysts from RBC Capital Markets and Shore Capital recently reiterated "Outperform" and "Buy" ratings, with price targets ranging between 1,000p and 1,050p, suggesting significant upside from current levels.

- Sector Rotation: As the market prepares for potential BoE rate cuts later in 2026, investors are rotating into mid-sized lenders with high Return on Tangible Equity (RoTE), where Paragon currently leads with a robust 17.5%.

Latest Business Model: The "Specialist" Pivot

Paragon has evolved from a traditional mortgage lender into a tech-enabled specialist bank. Its 2026 model focuses on two high-margin pillars:

- Mortgage Lending: Deep focus on professional landlords (Buy-to-Let) and complex residential property development.

- Commercial Lending: SME-focused asset finance, equipment leasing, and motor finance.

- Digital-First Funding: Unlike the "Big Four," Paragon funds its lending almost entirely through its digital savings brand "Spring", which surpassed £600 million in balances by late 2025.

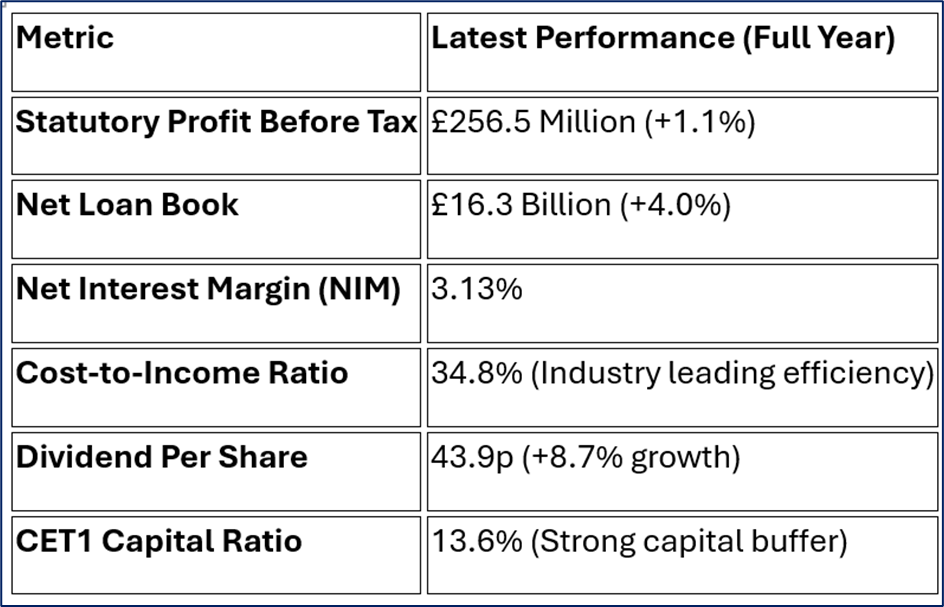

Financial & Operational Performance (FY 2025/2026)

The most recent audited figures reveal a bank that is lean, profitable, and highly capitalized.

Source: Company Data

SWOT Analysis: The Analytical Lens

Source: Kalkine Group

Strengths

- Efficiency: A cost-to-income ratio below 35% makes Paragon one of the most efficient banks in the FTSE 250.

- High RoTE: Delivering a 17.5% Return on Tangible Equity, significantly outperforming larger retail banks.

- Specialist Expertise: Their focus on professional landlords provides a "moat" against more generalized lenders.

Weaknesses

- Concentration Risk: Over 90% of revenue is tied to the UK economy and property market.

- NIM Pressure: Management has guided that Net Interest Margins may narrow to 2.90%–3.00% in 2026 as competition for deposits intensifies.

Opportunities

- Digital Expansion: The success of the "Spring" savings app provides a cheaper route to funding.

- SME Growth: As larger banks tighten credit, Paragon is capturing market share in the underserved SME asset finance sector.

Threats

- Motor Finance Redress: Paragon has set aside £25.5 million for potential motor commission payouts following the FCA's industry-wide investigation.

- Macro Volatility: Any sudden spike in UK unemployment could impact the development finance and BTL portfolios.

Key Risks to Monitor

- The "Motor Scandal" Hangover: While the £25.5m provision is managed, any expansion of the FCA's redress scope could require further capital hits.

- Regulatory Drag: New Basel 3.1 capital rules (effective Jan 2026) may increase the "cost of capital" for SME lending, potentially squeezing margins.

- Property Market Sensitivity: If UK house prices stagnate or drop in 2026, the loan-to-value (LTV) ratios on their £16bn book could come under scrutiny.

Conclusion

Paragon Banking’s 2% rise today reflects a market that is beginning to value efficiency and capital return over pure scale. With a massive dividend hike and an active buyback program, the bank is signaling extreme confidence to the retail market. However, the guided "margin squeeze" for 2026 and the looming cloud of motor finance litigation mean that while the engine is running hot, the road ahead has a few visible potholes.

Please wait processing your request...

Please wait processing your request...