In a dominant display of market confidence, GSK PLC (LSE: GSK) emerged as the star performer of the FTSE 100 today, with shares climbing ~4% following a flurry of regulatory victories and a strategic pivot that has analysts recalculating the company’s 2026 terminal value.

The surge, which added billions to GSK's market capitalization, marks a "de-risking" milestone for CEO Emma Walmsley’s biopharma-focused strategy.

The Catalyst: Why GSK is Trending Today

The primary driver behind today's rally is the triple-crown regulatory approval of Exdensur (depemokimab). On January 6, 2026, Japan’s Ministry of Health, Labour and Welfare (MHLW) gave the green light to the ultra-long-acting biologic for severe asthma and nasal polyps.

Key Performance Drivers:

Source: Kalkine Group

- Pipeline Perfection: Exdensur is the first biologic in its class to offer twice-yearly dosing, a massive competitive advantage over monthly rivals.

- Market Expansion: With approvals now secured in the US, UK, and Japan, GSK has unlocked the world’s three largest pharmaceutical markets for its new respiratory flagship in less than 30 days.

- Operational Beat: Strong Q4 2025 performance data (released early Jan) showed Specialty Medicines growing at 16% YoY, far outstripping the industry average.

- Zantac Resolution: Investor sentiment remains buoyed by the successful implementation of the $2.2 billion settlement (concluded in late 2025), which resolved 93% of US state court cases, effectively removing the "litigation overhang" that plagued the stock for years.

The 2026 Business Model: Specialized & Streamlined

Following the 2022 demerger of its consumer health wing (Haleon), GSK’s latest business model is built on Pure-Play Biopharma. The company has moved away from "general" medicines toward high-margin, patent-protected Specialty Medicines and Vaccines.

Core Revenue Pillars:

- Infectious Diseases & HIV: Through ViiV Healthcare, GSK dominates long-acting HIV treatments.

- Respiratory & Immunology: Transitioning from traditional inhalers to advanced biologics (like Nucala and Exdensur).

- Oncology: Rapidly scaling its B7-H3-targeted antibody-drug conjugates (ADCs).

- Vaccines: Utilizing mRNA and adjuvant technologies to maintain a world-leading position in Shingles (Shingrix) and RSV (Arexvy).

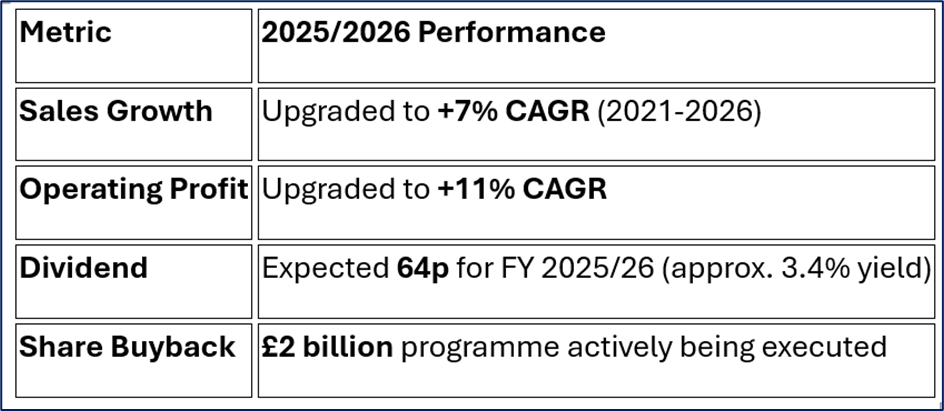

Latest Financial & Operational Snapshot

Source: Company Data

Operational Update: GSK has officially integrated AI-driven drug discovery into its R&D labs, allocating £45m to AMR (Anti-Microbial Resistance) research, aiming to cut drug development timelines by 20% by 2027.

SWOT Analysis (2026 Update)

Source: Kalkine Group

Strengths

- Dominant RSV/Shingles Franchise: High barriers to entry and strong brand loyalty.

- R&D Efficiency: One of the industry’s highest "success-to-approval" ratios in Phase III trials.

- Long-Acting Tech: Leadership in injectable medicines that reduce patient dosing frequency.

Weaknesses

- Patent Cliffs: Looming loss of exclusivity for key HIV assets (Dolutegravir) toward 2028-2030.

- Vaccine Volatility: Short-term fluctuations in US uptake for adult vaccines.

Opportunities

- mRNA Pipeline: Expansion into combination Flu/COVID-19 vaccines.

- Emerging Markets: High demand for Shingrix in China and India.

- MASH (Liver Disease): Potential blockbuster data expected later in 2026 for efimosfermin.

Threats

- US Drug Pricing: The Inflation Reduction Act (IRA) continues to put pressure on Medicare pricing.

- Competition: Intense rivalry from Pfizer and Moderna in the respiratory vaccine space.

Risks to Watch

While the January 6 rally is significant, investors are monitoring "The 7% Gap"—the risk that new product launches may not fully offset the revenue loss when core HIV patents expire. Furthermore, while Zantac is 93% settled, the remaining 7% of "orphan" cases and potential class-action appeals in Delaware represent a lingering, albeit minor, tail risk.

Conclusion

GSK’s 4% jump on January 6, 2026, is a "validation trade." It signals that the market finally believes in the company’s ability to grow without its consumer health safety net. By securing global approvals for ultra-long-acting biologics and resolving its legal headaches, GSK has transformed from a "value trap" into a high-performance growth story.

Please wait processing your request...

Please wait processing your request...