Key Reasons & Drivers for the Surge

The ~5% rise in Princes Group stock today appears driven by a confluence of sector-specific optimism and technical recovery rather than a single regulatory filing.

Source: Kalkine Group

1. "Supermarket Sweep" – Anticipation of Strong Christmas Trading Early January is "trading update season" for major UK retailers like Tesco and Sainsbury’s. As a primary supplier of both branded goods (Napolina, Princes) and private-label essentials, Princes Group is a direct beneficiary of strong grocery volumes. Investors are likely front-running expected positive data from retailers, betting that the "cost-of-living" ease has boosted premium canned and ambient food sales over the holidays.

2. Analyst "Top Picks" for 2026 The first week of the trading year often sees institutional capital rotating into "value" and "defensive" stocks. Analysts have recently highlighted Princes' improved EBITDA margins (up to 7.8% in late 2025) as a key differentiator. The stock is likely benefiting from a "Sector Overweight" upgrade, positioning it as a safe harbor against tech volatility.

3. Technical Rebound & Short Covering After dipping to ~450p in late December (post-IPO lock-up jitters), the stock has crossed key technical moving averages (15-day and 50-day). This 5% move signals a "breakout," forcing short-term bears to cover their positions, further fueling the rally toward the psychological 500p resistance level.

Latest Business Model: The "New Princes" Strategy

Since its IPO in late 2025 and integration with majority shareholder NewPrinces (formerly Newlat Food), the company has pivoted from a "volume-first" to a "margin-first" model.

- Dual-Track Revenue: The business balances Branded giants (Napolina, Princes Tuna, Crisp 'n Dry) with massive Private Label contracts for UK/EU supermarkets. This hedges against consumer down-trading; if shoppers switch from brand to own-label, Princes still captures the sale.

- Vertical Integration: Utilizing the synergies with Newlat, the group now shares procurement networks for wheat (pasta) and tomatoes, significantly lowering raw material costs compared to standalone competitors.

- Portfolio Rationalization: They are actively exiting low-margin "commodity" contracts to focus on value-added products (e.g., ready meals, premium sauces) that command higher shelf prices.

Financial & Operational Updates (Q4/FY 2025 Context)

- Margin Expansion: The most recent data (Q3 2025) showed EBITDA rising 51.5% year-on-year, driven by the delivery of synergy targets earlier than planned.

- Debt Reduction: Proceeds from the IPO (~£400m) were used to deleverage, bringing net debt down significantly. The "Pro Forma Adjusted Net Debt" is now sitting at comfortable levels (~£268m), reducing interest rate sensitivity.

- Operational Efficiency: The "pass-through" pricing mechanisms have stabilized. As inflation cools, Princes has managed to hold pricing power better than expected, widening the gap between input costs and wholesale prices.

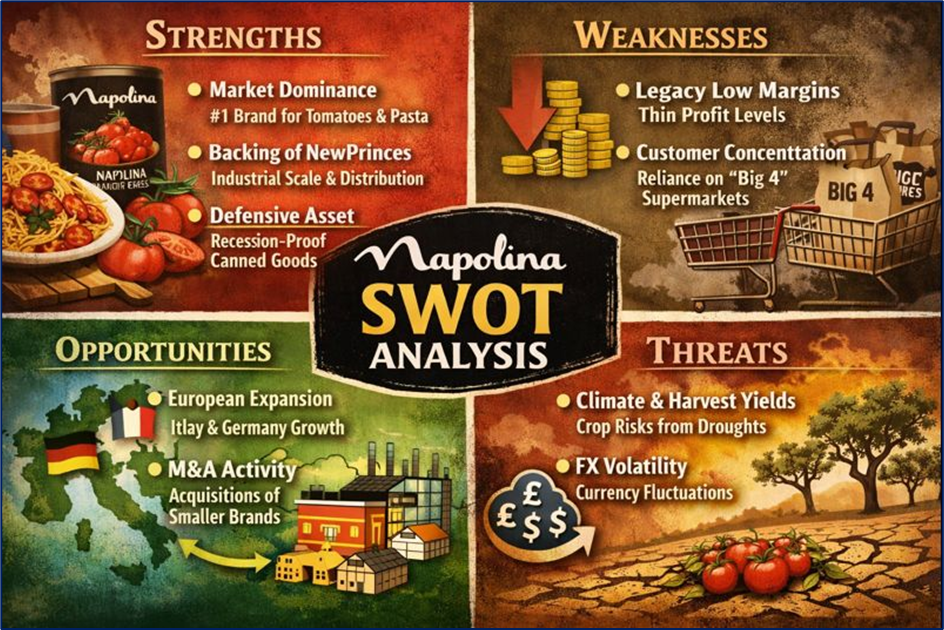

SWOT Analysis

Source: Kalkine Group

Strengths (Internal)

- Market Dominance: Napolina remains the UK’s #1 brand for tomatoes and pasta, a "moat" that is hard to displace.

- Backing of NewPrinces: The majority ownership by NewPrinces S.p.A. provides industrial scale, allowing for cross-border distribution that standalone UK rivals cannot match.

- Defensive Asset: Canned food performs well in both recessions (value) and booms (convenience).

Weaknesses (Internal)

- Legacy Low Margins: Despite improvements, the ambient food sector typically operates on razor-thin margins compared to tech or pharma.

- Customer Concentration: Heavy reliance on the "Big 4" UK supermarkets gives retailers significant bargaining power to squeeze Princes' prices.

Opportunities (External)

- European Expansion: Leveraging Newlat’s distribution channels to push Princes brands into Italy and Germany, reducing UK dependency.

- M&A Activity: Management has explicitly stated a desire for "value-accretive M&A," potentially acquiring smaller, distressed food brands to plug into their efficient supply chain.

Threats (External)

- Climate & Harvest Yields: Olive oil and tomato crops are highly sensitive to climate change (droughts in Southern Europe), which can spike input costs unpredictably.

- FX Volatility: Sourcing raw materials in Euros/Dollars while reporting in GBP leaves earnings exposed to currency fluctuations.

Key Risks to Watch

- Synergy Execution: The market has priced in the success of the Newlat integration. Any operational hiccups or culture clashes between the UK and Italian teams could punish the stock.

- Commodity Deflation: Paradoxically, falling raw material prices can hurt revenue if retailer contracts have strict "deflation clauses" that force Princes to lower prices immediately.

- Governance Structure: With NewPrinces holding a majority stake, minority shareholders have limited voting power. Decisions may favor the parent company over the listed UK entity.

Conclusion

Princes Group's 5% rise on January 7, 2026, marks a confident start to the year, validating the market's belief in its "margin-over-volume" pivot. The stock is transitioning from a "new IPO" to a "staple compounder." While the long-term thesis rests on successful continental expansion and weather-dependent crop yields, the immediate sentiment is buoyed by a robust UK consumer and intelligent cost management.

Please wait processing your request...

Please wait processing your request...