The first trading session of 2026 saw Prudential PLC (LSE: PRU) continue its relentless northward march. Rising approximately 1% on January 2nd to touch a new 52-week high of roughly 1,172p, the stock is currently riding a wave of institutional confidence.

With a staggering 103% gain over the last 12 months, the insurer has officially shed its "underperformer" tag, becoming a focal point for retail and institutional investors alike.

The Jan 2 Catalyst: Why the Stock is Climbing

Source: Kalkine Group

The ~1% nudge on the first Friday of the year wasn't just "January effect" noise. It was the culmination of three specific drivers:

- Completion of the $2 Billion Buyback: Prudential confirmed it successfully closed its massive capital return program as 2025 ended. By shrinking its share count by roughly 4.5%, the company has fundamentally increased the "slice of the pie" for remaining shareholders.

- The "Sanaenomics" Tailwind: With new Japanese economic policies (Sanaenomics) taking hold, investors are rotating into Asia-focused financials. Prudential, with its massive footprint in Japan and Southeast Asia, is viewed as a primary proxy for this regional recovery.

- Technical Momentum: Breaking the previous 52-week high triggered algorithmic buying. Trading at a P/E of approximately 12.05x, the stock is still perceived as "cheap" relative to its double-digit growth in New Business Profit (NBP).

Latest Business Model: The "Pivot to Growth"

Prudential has completed its transformation into a pure-play Asia and Africa life insurance and asset management powerhouse.

- Geographic Focus: 100% focused on high-growth, under-penetrated markets.

- Dual-Engine Distribution: A hybrid model using a 1-million-strong agency force and exclusive Bancassurance partnerships (e.g., Bank Syariah Indonesia).

- Health & Protection Focus: Shifting away from low-margin savings products toward high-margin health and "protection" (life/critical illness) cover.

- Eastspring Investments: Its asset management arm now manages over $286 billion, providing a steady stream of fee-based income that balances the insurance underwriting risk.

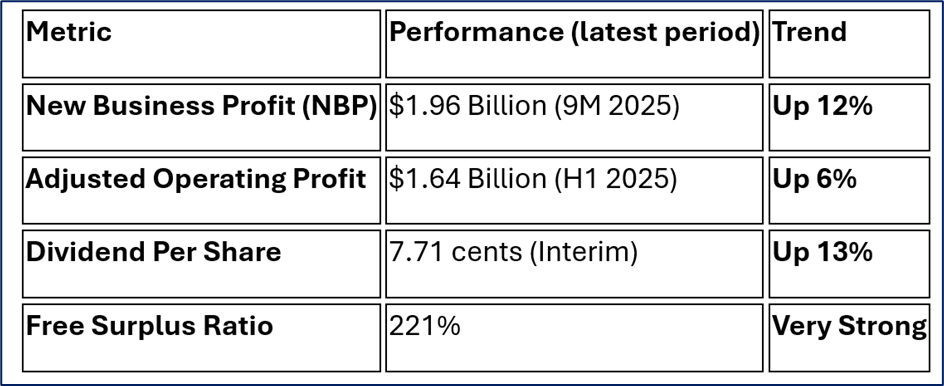

Financial & Operational Performance (Latest Update)

The most recent data highlights a company hitting its "inflection point":

Source: Company Data

Operational Milestone: In late 2025, Prudential’s Hong Kong entity was designated a Domestic Systemically Important Insurer (D-SII), a badge of stability that, while bringing more regulation, has boosted sovereign-level trust in its solvency.

SWOT Analysis (2026 Outlook)

Source: Kalkine Group

Strengths

- Capital Health: A perfect Piotroski Score of 9 and a "Great" financial health rating.

- Scale: Managing $1.6 trillion in Assets Under Management (AUM) gives it massive "moat" protection.

- Dividend History: 34 consecutive years of payments.

Weaknesses

- Complexity: A multi-jurisdictional regulatory environment (UK, HK, Singapore) adds high compliance costs.

- Legacy Tech: Despite a $400M investment, older systems still hinder total operational agility compared to "Insurtech" rivals.

Opportunities

- IPAMC IPO: The upcoming IPO of its Indian JV (ICICI Prudential AMC) is expected to unlock billions in "hidden" value.

- Retirement Gap: The aging population in China and Southeast Asia represents a multi-decade growth runway for its pension products.

Threats

- Geopolitical Friction: Trade tensions between the West and China can impact investor sentiment toward HK-heavy stocks.

- Monetary Volatility: Sudden currency swings in emerging markets can eat into reported USD earnings.

Risks to Watch

While the momentum is strong, the "bull run" faces two primary hurdles in 2026:

- Executive Transition: The upcoming transition to a new Chief Investment Officer (CIO) in March 2026 creates a short-term "execution risk" in how the company manages its vast bond portfolio.

- Margin Compression: If competition in the "Bancassurance" space intensifies, Prudential may have to pay higher commissions to banks, squeezing its New Business Margins.

Conclusion

Prudential’s 1% gain on January 2nd reflects a market that finally believes in the "Asia Pivot." With a combination of disciplined capital returns (buybacks), a clean balance sheet, and double-digit growth in its core insurance metrics, the stock is currently acting as a "quality growth" play within the FTSE 100. The upcoming IPO of its Indian asset management arm remains the next major "hard" catalyst for the share price.

Please wait processing your request...

Please wait processing your request...