On January 6, 2026, Raspberry Pi Holdings PLC (LSE: RPI) witnessed a significant surge, closing up approximately 11%. This rally stands out against a broader backdrop of FTSE volatility and reflects a renewed investor confidence in the company’s pivot from a hobbyist brand to an industrial powerhouse.

Key Reasons & Drivers for the Surge

Source: Kalkine Group

The 11% jump on January 6 was driven by a combination of strategic updates and positive market sentiment:

- Industrial "Design-In" Wins: Reports emerged regarding a significant increase in direct-to-OEM (Original Equipment Manufacturer) shipments. Over 70% of unit sales are now attributed to the industrial and embedded segment, which offers more stable and recurring revenue than the cyclical consumer market.

- Margin Recovery Sentiment: After a period of "inventory correction" and high memory costs in late 2025, investors are pricing in better unit economics for 2026. The shift toward higher-margin Compute Modules and proprietary silicon (like the RP2350) is seen as a major profitability driver.

- Insider Confidence: Recent filings revealed that founder Eben Upton and other directors have been active in the market. While some minor selling occurred for tax purposes, the broader trend of insider buying at lower price points in late 2025 acted as a "floor" for the stock.

- Strategic Partnerships: Expansion of the Sony partnership for local AI processing capabilities has positioned Raspberry Pi as a "pick-and-shovel" play for the edge-computing and AI revolution.

Latest Business Model & Operational Updates

Raspberry Pi has evolved from a non-profit educational project into a full-stack engineering organization.

- Vertical Integration: Unlike competitors, RPI designs its own silicon IP (ASICs), reducing reliance on third-party chipmakers and allowing for higher customization for industrial clients.

- Two-Stage Growth Model: The business now focuses on a "Land and Expand" strategy:

- Phase 1: Seeding innovators and engineers via affordable Single Board Computers (SBCs).

- Phase 2: Scaling those innovations into mass-market industrial products using Compute Modules that integrated into everything from EV chargers to medical devices.

- Operational Milestones (Jan 2026):

- Semiconductor Dominance: For the first time, semiconductor unit volumes (standalone chips) are rivaling board unit volumes.

- Supply Chain Stability: Close collaboration with Sony’s UK manufacturing site has mitigated the supply shocks seen in previous years.

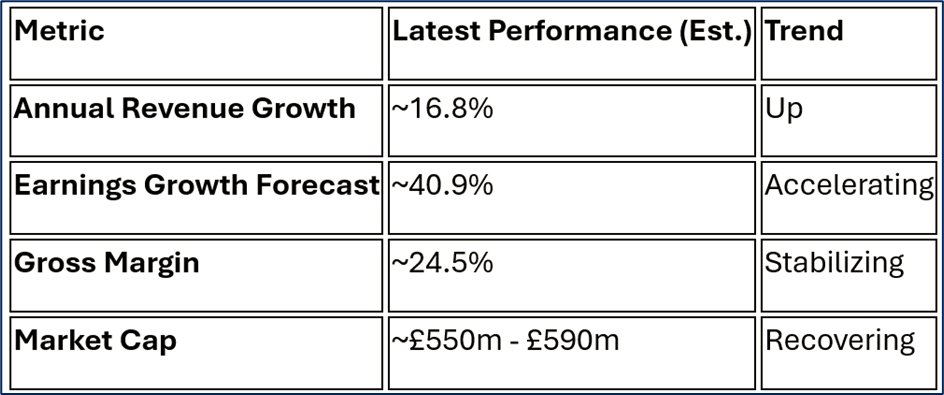

Financial Snapshot

Source: Company Data

SWOT Analysis

Source: Kalkine Group

Strengths

- Brand Loyalty: A massive global community of "evangelist" engineers.

- Low-Cost Leader: Unrivaled price-to-performance ratio in the SBC market.

- Ecosystem: Extensive software library and "HAT" hardware add-on ecosystem.

Weaknesses

- Thin Margins: High dependence on low-margin hardware compared to software-heavy tech firms.

- C-Suite Transition: CFO Richard Boult is slated to step down in 2026, creating short-term leadership uncertainty.

Opportunities

- Edge AI: The need for low-power, local AI processing in IoT devices.

- Market Expansion: Increasing penetration in the US and Asian industrial sectors.

- Software Monetization: Potential to introduce recurring revenue through enterprise management software.

Threats

- Component Costs: Volatility in memory (RAM) prices can eat into razor-thin hardware margins.

- Competition: Rising competition from Chinese manufacturers and "clones" offering similar specs at lower prices.

Risks to Consider

Investors should remain aware of the high Price-to-Earnings (P/E) ratio, which often hovers between 60x and 80x. This makes the stock highly sensitive to even minor earnings misses. Additionally, the transition to a more corporate, OEM-focused model risks alienating the enthusiast base if product availability for "makers" is sacrificed for industrial orders.

Conclusion

The 11% rally on January 6, 2026, marks a potential turning point for Raspberry Pi Holdings. By successfully navigating the post-IPO volatility and proving its utility in the industrial sector, the company is shifting from a "niche tech" story to a foundational "industrial IoT" play. While risks regarding leadership transitions and margin pressure remain, the current momentum suggests that markets are finally buying into the "Pi" as a serious contender in the global semiconductor landscape.

Please wait processing your request...

Please wait processing your request...