The FTSE 100’s pest control giant, Rentokil Initial (LSE: RTO), saw its share price jump approximately 3.6% on January 6, 2026, outperforming the broader market.

After a period of "digestion" following its massive Terminix acquisition, the company is finally showing the operational "teeth" investors have been waiting for.

The Catalyst: Why RTO is Up Today

The primary driver for today’s movement is a combination of positive analyst sentiment and quantifiable progress in the North American integration.

Investment banks, including BofA Securities and J.P. Morgan, have recently entered 2026 with "Buy" ratings, citing improved visibility on the company’s margin expansion. The stock’s climb reflects a "catch-up" trade as the market realizes that the $100 million cost-saving target for the Terminix merger is not just a projection, but a nearing reality.

Key Drivers for 2026

Source: Kalkine Group

- Terminix Integration Milestones: The "RIGHT WAY 2" strategy is hitting its stride. Over 250 branches have now unified their back-office systems, reducing administrative friction.

- The "Satellite" Strategy: Rentokil has successfully rolled out nearly 150 satellite branches in the US. This "local-first" approach has improved customer proximity, directly boosting organic lead generation by over 6% in recent months.

- Retention Resilience: Colleague retention has hit a record 81.8%, marking 11 consecutive quarters of improvement. In a service-heavy industry, keeping experienced "ratcatchers" is the single biggest factor in maintaining route density and profitability.

2026 Business Model: Leaner and More Focused

Rentokil has undergone a significant structural shift. In late 2025, the company completed the sale of its France Workwear business for approximately €410 million.

The New Focus:

- Pure-Play Pest Control: Now making up nearly 80% of revenue, focusing on high-margin residential and commercial contracts.

- Hygiene & Wellbeing: A simplified portfolio focusing on washroom services and "Ambius" (plant care), which provides a stable, recurring revenue stream.

- Digital-First Servicing: Using "PestConnect" (smart traps) to move from reactive to predictive maintenance, which significantly lowers the cost-to-serve per customer.

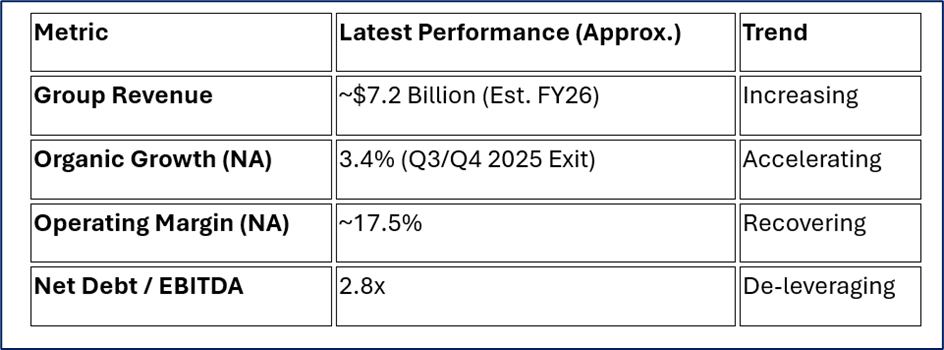

Latest Financial & Operational Updates

The company enters 2026 with a bolstered balance sheet and tightening margins.

Source: Company Data

Operational Highlights:

- M&A: Successfully integrated 21 bolt-on acquisitions in the past year, adding $39 million in annual revenue.

- Pricing Power: Rentokil has successfully pushed through price increases slightly above inflation, a testament to the non-discretionary nature of pest control.

SWOT Analysis 2026

Source: Kalkine Group

Strengths

- Global Scale: Operates in 90 countries with 90% coverage of global GDP.

- High Recurring Revenue: Over 80% of revenue is contract-based.

- Centenary Brand: Celebrating 100 years in 2025/2026, the brand carries immense trust in the B2B sector.

Weaknesses

- Integration Complexity: The Terminix merger was slower than expected, leading to historical cost overruns.

- North American Dependency: Nearly 60% of revenue is tied to the US market, making it sensitive to US labor costs.

Opportunities

- Margin Expansion: Management targets a 20%+ North American margin post-2026 once the integration is 100% complete.

- Under-served Markets: Over 80% of the North American residential termite segment remains unserved by professional providers.

Threats

- Macro-Volatility: While "pests don't care about a recession," labor and fuel costs remain highly sensitive to inflation.

- Legal Scrutiny: Historical class-action lawsuits regarding the Terminix integration have caused reputational drag.

Risks to Watch

- Seasonal Nuances: Q1 is historically a quieter quarter for pest control. Any "miss" in spring termite activity could dampen sentiment.

- Labor Inflation: Wage pressure in the US remains the biggest threat to the 20% margin target.

- Execution Risk: The final phase of the Terminix branch mergers is the most delicate; any disruption in customer service could lead to churn.

Conclusion

Rentokil Initial’s 3% pop today is a signal that the market is finally rewarding the "heavy lifting" done in 2025. By shedding the Workwear business and focusing on its core pest control dominance, RTO has transitioned from a messy integration story into a streamlined growth engine. The "Drive to 85" (customer retention goal) and the $100 million synergy targets are now the primary barometers for the stock's 2026 performance.

Please wait processing your request...

Please wait processing your request...