In the quiet corners of the UK tech market, a sudden explosion of activity has turned heads. 1Spatial (LSE: SPA), a Cambridge-based software company previously known for its steady but niche work in geospatial data, has seen its stock price rocket upwards of 40% in a remarkably short window.

For observers watching the charts, this isn't just a random fluctuation. It is a textbook example of how strategic positioning in a "boring" sector—data management—can suddenly become the hottest ticket in town when the right catalysts align. The surge is driven by a potent combination of a potential takeover bid and significant government contract wins that have validated its long-term strategy.

The "Viral" Catalyst: A Takeover Approach

The primary engine behind the sudden vertical climb in the share price is the revelation of a possible cash offer from VertiGIS, a global provider of spatial asset management solutions backed by major private equity.

Takeover interest is the ultimate "viral" driver in equity markets. It forces a re-evaluation of a company's assets, often revealing that the public market has been undervaluing the business compared to what a strategic trade buyer is willing to pay. For 1Spatial, this potential acquisition highlights the strategic value of its proprietary technology, which cleans and manages complex location data—a commodity becoming increasingly critical for AI, digital twins, and smart infrastructure.

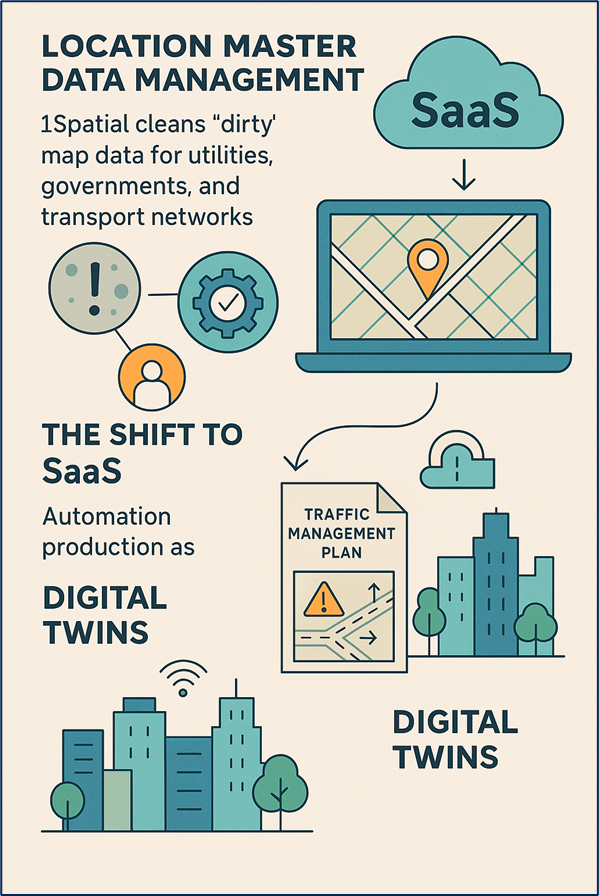

The "Clean Data" Business Model

To understand why a company like VertiGIS would be interested, you have to look under the hood of 1Spatial’s business model.

- Location Master Data Management (LMDM) At its core, 1Spatial solves a massive, unglamorous problem: "dirty" data. Utility companies, governments, and transport networks hold vast amounts of map data that is often inaccurate, duplicated, or disconnected. 1Spatial’s software (like 1Integrate) automates the validation and cleaning of this data. Think of it as a spell-checker, but for complex digital maps.

- The Shift to SaaS (Software as a Service) Historically, 1Spatial relied on one-off licences and consulting services. However, they have been aggressively pivoting to a recurring revenue model.

- Recurring Revenue: Now accounting for over 60% of total revenue, this model provides predictable, stable cash flow that investors (and acquirers) love.

- 1Streetworks: This is their "star" SaaS product. It automates the production of traffic management plans, reducing a process that used to take hours of manual engineering down to just minutes.

- Digital Twins & Smart Cities As cities try to build "digital twins" (virtual replicas of physical infrastructure), they need accurate underlying data. 1Spatial is the gatekeeper ensuring that the foundation of these futuristic projects is solid.

Source: Kalkine Group

Key Drivers of the Recent Rally

Beyond the takeover speculation, the fundamental business has delivered two major updates that have fueled investor confidence.

- The £4.2m NUAR Contract Win Just prior to the takeover news, 1Spatial announced a major win with the National Underground Asset Register (NUAR).

- The Deal: A contract worth £4.2 million to help build a digital map of underground pipes and cables across the UK.

- The Significance: This is not just revenue; it is a "moat." It embeds 1Spatial deeply into critical national infrastructure, making them an essential partner for the UK government for years to come.

- Resilience in Trading Updates Despite a sluggish economic environment where many software companies have issued profit warnings, 1Spatial’s recent trading updates (H1 results) demonstrated resilience. While sales cycles have been slower (meaning customers are taking longer to sign deals), the company successfully grew its recurring revenue base. This proved to the market that their transition to a SaaS model is working, even when the wider economy is dragging.

Risks: What Could Go Wrong?

While the charts look green, the situation is not without its hazards. A 40% rise prices in a lot of optimism, and there are specific risks that must be acknowledged.

- Deal Uncertainty: The approach from VertiGIS is currently a "possible" offer. In the world of M&A (Mergers and Acquisitions), discussions often fall apart over valuation or regulatory concerns. If the deal collapses, the share price could rapidly deflate to its pre-hype levels.

- Government Dependency: A significant portion of 1Spatial’s revenue comes from government contracts (like the NUAR deal). While lucrative, these are subject to political budget cuts, delays, or policy changes.

- The "Lumpy" Nature of Contracts: despite the move to SaaS, 1Spatial is still prone to "lumpy" revenue, where missing a single large deal deadline can skew quarterly results significantly.

- Competition: The geospatial AI market is heating up. Big tech players are increasingly interested in map data, potentially squeezing smaller, niche players if they decide to enter the "data validation" space aggressively.

Conclusion: A Niche Player on the Global Stage

1Spatial has transformed from a quiet UK software firm into a battleground for strategic asset acquisition. The 40% surge is a rational market reaction to two things: a massive validation of their technology via the NUAR contract, and the realization by private equity that the company may be undervalued.

For the market, the story is no longer just about "maps"—it is about the integrity of the data that will power the next generation of infrastructure. Whether 1Spatial remains independent or is absorbed by a larger entity, its technology has undeniably moved to center stage.

Source: Trading View, 12 December 2025, 8:45 AM GMT

Please wait processing your request...

Please wait processing your request...