Executive Summary: From Stagnation to Strategic Growth

As the UK economy exits the "permacrisis" era of the early 2020s, 2026 is projected to be a year of divergence and stabilization. Major institutional forecasters (UBS, Morgan Stanley, JP Morgan) align on a narrative where the FTSE 100 potentially breaches the psychological 10,000 barrier, driven not by explosive GDP growth, but by a "catch-up" trade in valuations, infrastructure spending, and the "Great Grid Upgrade."

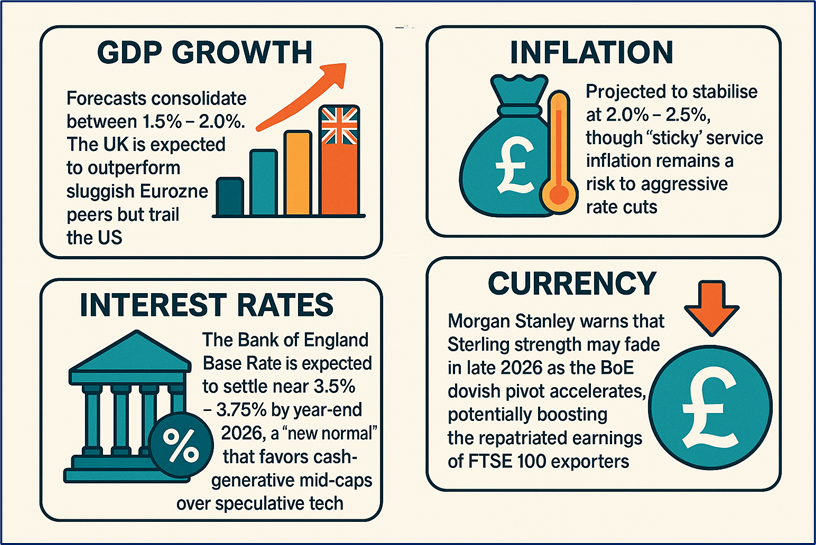

- 2026 Macro Dashboard: The Data Landscape

- GDP Growth: Forecasts consolidate between 1.5% – 2.0%. The UK is expected to outperform sluggish Eurozone peers but trail the US.

- Inflation: Projected to stabilize at 2.0% – 2.5%, though "sticky" service inflation remains a risk to aggressive rate cuts.

- Interest Rates: The Bank of England Base Rate is expected to settle near 3.5% – 3.75% by year-end 2026, a "new normal" that favours cash-generative mid-caps over speculative tech.

- Currency: Morgan Stanley warns that Sterling strength may fade in late 2026 as the BoE dovish pivot accelerates, potentially boosting the repatriated earnings of FTSE 100 exporters.

Source: Kalkine Group

- Mega-Trends Driving 2026

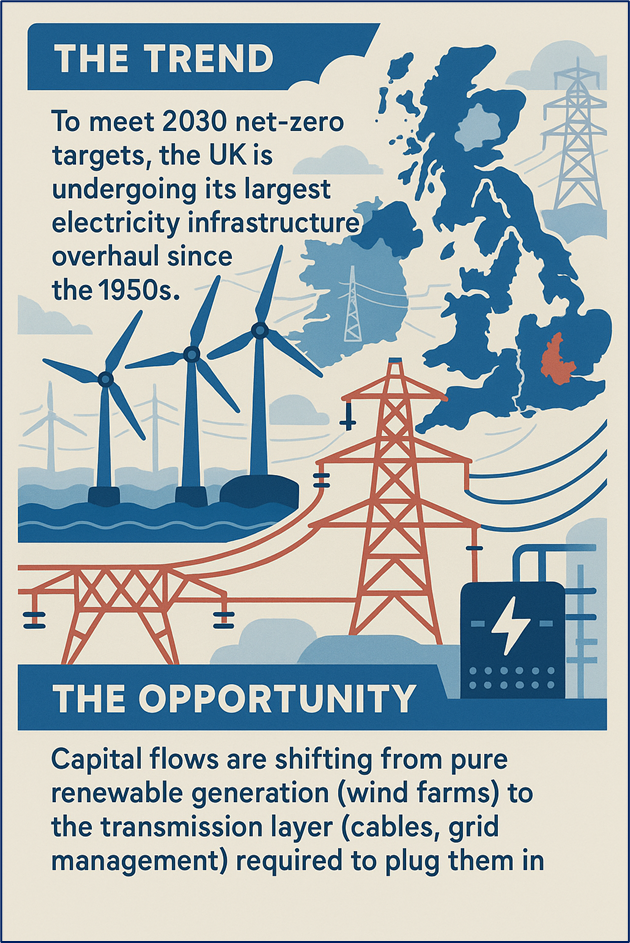

Theme A: The "Great Grid Upgrade" & Energy Security

Source: Kalkine Group

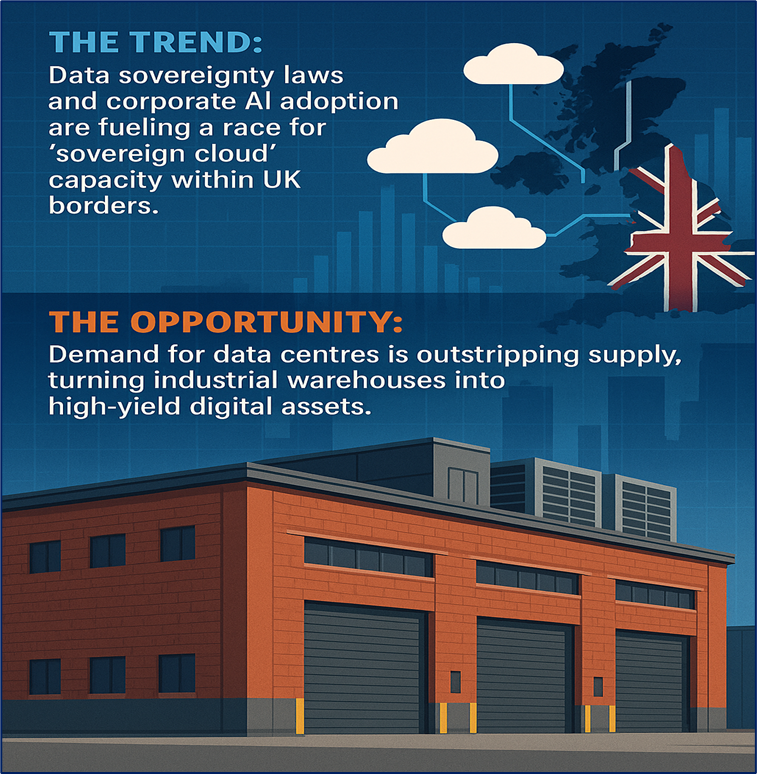

Theme B: AI Sovereignty & Digital Real Estate

Source: Kalkine Group

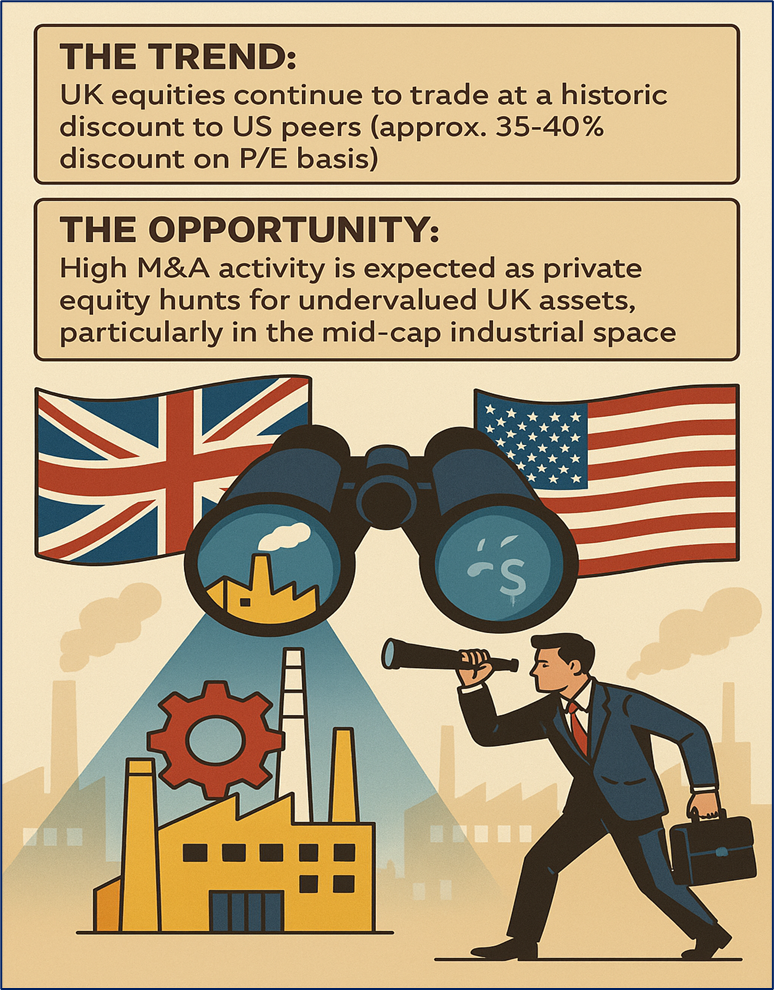

Theme C: The "Unloved" Valuation Gap

Source: Kalkine Group

- Sectors & Stocks to Watch in 2026

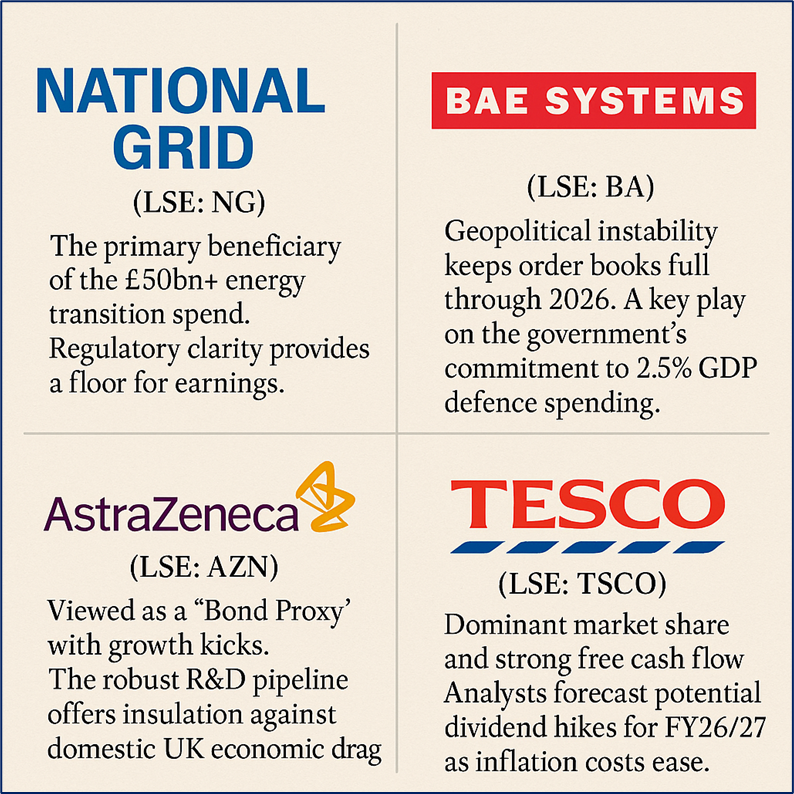

CORE DEFENSIVE: The "Income Fortresses"

- National Grid (LSE: NG): The primary beneficiary of the £50bn+ energy transition spend. Regulatory clarity provides a floor for earnings.

- BAE Systems (LSE: BA): Geopolitical instability keeps order books full through 2026. A key play on the government's commitment to 2.5% GDP defense spending.

- AstraZeneca (LSE: AZN): Viewed as a "Bond Proxy" with growth kicks. The robust R&D pipeline offers insulation against domestic UK economic drag.

- Tesco (LSE: TSCO): Dominant market share and strong free cash flow. Analysts forecast potential dividend hikes for FY26/27 as inflation costs ease.

Source: Kalkine Group

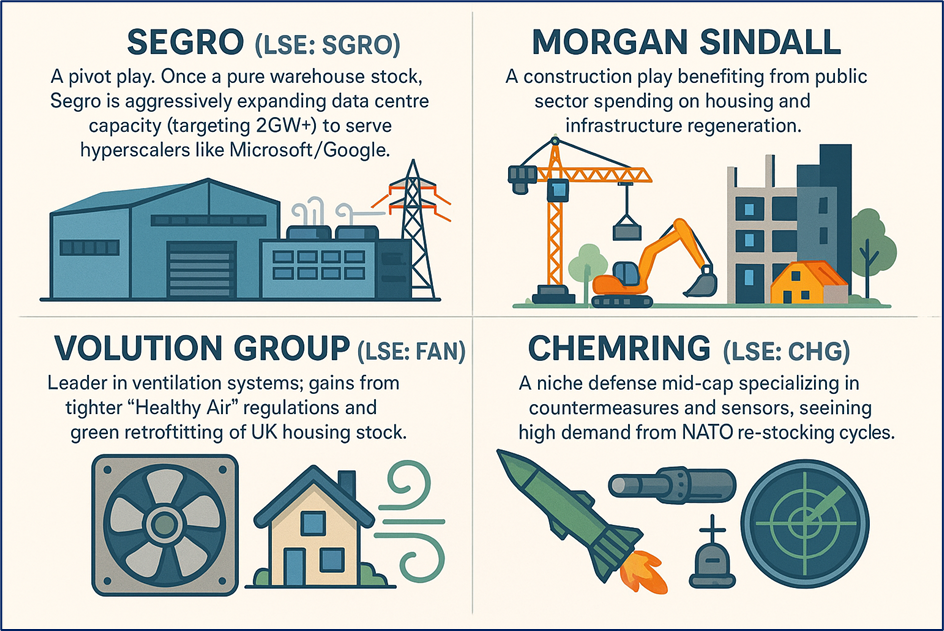

GROWTH & RECOVERY: The "Alpha" Hunters

- Segro (LSE: SGRO): A pivot play. Once a pure warehouse stock, Segro is aggressively expanding data centre capacity (targeting 2GW+) to serve hyperscalers like Microsoft/Google.

- Morgan Sindall (LSE: MGNS): A construction play benefiting from public sector spending on housing and infrastructure regeneration.

- Volution Group (LSE: FAN): Leader in ventilation systems; gains from tighter "Healthy Air" regulations and green retrofitting of UK housing stock.

- Chemring (LSE: CHG): A niche defense mid-cap specializing in countermeasures and sensors, seeing high demand from NATO re-stocking cycles.

Source: Kalkine Group

SPECIAL SITUATIONS: IPOs & Disruptors

- Revolut (Pre-IPO): The "White Whale" of UK Fintech. Rumoured for a 2026 IPO, potentially valuing it over $40bn. A litmus test for London's ability to retain tech giants.

- Tritax Big Box (LSE: BBOX): Leveraging its massive land bank to develop power-heavy data centres, pivoting from simple logistics boxes to high-value digital infrastructure.

Source: Kalkine Group

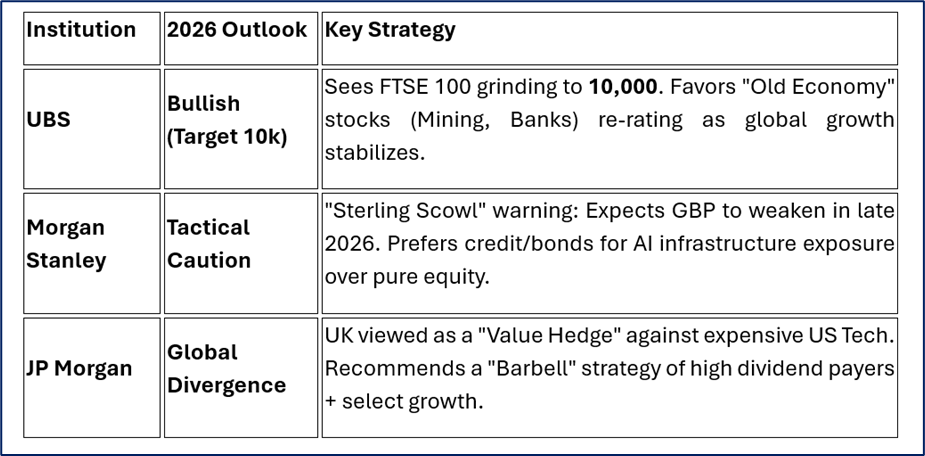

- Institutional Positioning: The Broker Consensus

Source: Global Reports

- Risks & Headwinds

- The "Sticky" Service Inflation: If wage growth keeps service inflation above 3%, the Bank of England may halt rate cuts, punishing housing and retail stocks.

- Trade Fragmentation: A protectionist stance from the US (tariffs) could hurt UK exporters like auto (JLR) and pharma.

- The "De-Equitization" Trend: Continued take-private deals by PE firms shrink the public market, reducing liquidity and options for retail investors.

- Strategy for Investors: The "Barbell" Approach

Analysts suggest a balanced "Barbell Strategy" for 2026 to navigate the "Grind-Up":

- Left Side (Safety): 60% allocation to High-Yield Defensive stocks (Utilities, Defense, Banks). Goal: Harvest 4-6% dividends to beat inflation.

- Right Side (Growth): 40% allocation to Thematic Recovery plays (Data Centres, Mid-Cap Industrials). Goal: Capture capital appreciation from valuation re-rating.

Conclusion

2026 is shaping up to be a "Show Me" year. The easy gains from bouncing back after inflation are gone. The market will likely reward specific execution—companies actually building the grid, supplying the data centres, or delivering defense contracts—rather than broad index trackers. For the astute investor, the UK's "unloved" status is its greatest asset, offering entry points into world-class infrastructure at discounted valuations.

Please wait processing your request...

Please wait processing your request...