The UK economy staged a notable comeback in November, with Gross Domestic Product (GDP) growing by 0.3%. This figure outperformed the consensus estimate of 0.1% and follows a slight 0.1% contraction in October.

The rebound offers a glimmer of hope for the Treasury following a period of fiscal uncertainty surrounding the Autumn Budget. However, economists caution that beneath the headline growth, the recovery remains uneven and heavily influenced by temporary industrial corrections.

Sector Performance: A Tale of Two Industries

Source: Kalkine Group

The November growth was largely a story of manufacturing resurgence and professional service resilience, offset by a deepening slump in construction.

- Production & Manufacturing (+1.1%): This sector was the primary engine of growth. Within it, motor vehicle manufacturing surged 25.5%. This was a "catch-up" effect as the industry, specifically Jaguar Land Rover, recovered from a severe cyberattack in September that had paralyzed production for weeks.

- Services (+0.3%): Growth was led by "professional, scientific, and technical activities" (up 1.7%). Analysts noted that high demand for accounting and auditing services—likely fueled by businesses navigating the complexities of the new Autumn Budget—contributed significantly.

- Construction (-1.3%): The major laggard. Despite government promises of a building boom, output fell for another month. High interest rates continue to suppress new housing and commercial projects, with the sector now down nearly 3% since July.

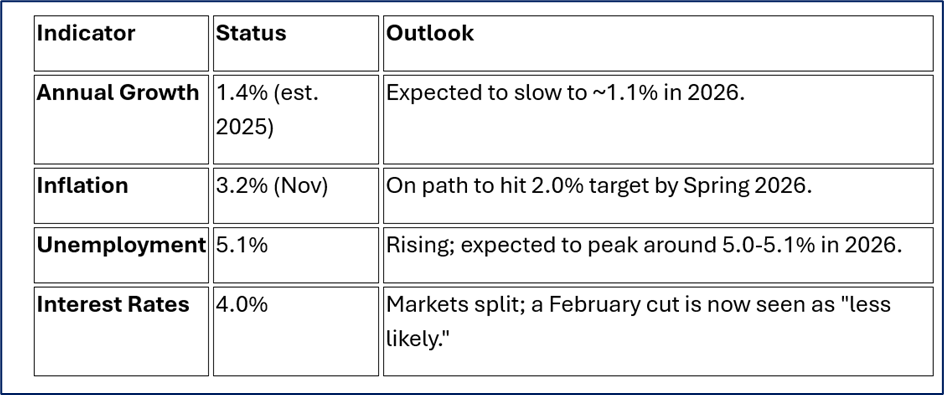

Macro Outlook & Risks

While the November bounce-back is positive, the broader macroeconomic picture for 2026 remains cautious.

Source: Market Data

Key Risks to the Recovery:

- Fiscal Tightening: The full impact of increased National Insurance contributions and tax threshold freezes may stifle private sector hiring and consumer spending in early 2026.

- Labor Market Rigidity: Firms are shedding jobs to manage rising wage costs (the National Minimum Wage increase), which could trigger a sharper rise in unemployment than currently forecasted.

- Global Trade: Potential shifts in international trade tariffs (particularly from the U.S.) pose a risk to the UK’s export-led manufacturing recovery.

Download Free Report – Explore 3 Stock Ideas & Industry Insights

Unlock 3 stock ideas and key industry insights in our free report. This information is general in nature and does not consider your personal objectives, financial situation, or needs. It is not financial advice.

All investments involve risk—consider independent advice before making any investment decisions.

View 3 Research Reports

Disclaimer:

References to ‘Kalkine’, ‘we’, ‘our’ and ‘us’ refer to Kalkine Limited.

This website is a service of Kalkine Limited. Kalkine Limited is a private limited company, incorporated in England and Wales with registration number 07903332. Kalkine Limited is authorised and regulated by the Financial Conduct Authority under reference number 579414.

The article has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. No advice or information, whether oral or written, obtained by you from Kalkine or through or from the service shall create any warranty not expressly stated. Kalkine does not intend to exclude any liability which it is not permitted to exclude under applicable law or regulation.

Kalkine does not offer financial advice based upon your personal financial situation or goals, and we shall NOT be held liable for any investment or trading losses you may incur by using the opinions expressed in our publications, market updates, news alerts and corporate profiles. Kalkine does not intend to exclude any liability which it is not permitted to exclude under applicable law or regulation. Kalkine’s non-personalised advice does not in any way endorse or recommend individuals, investment products or services for your personal financial situation. You should discuss your portfolios and the risk tolerance level appropriate for your personal financial situation, with a professional authorised financial planner and adviser. You should be aware that the value of any investment and the income from it can go down as well as up and you may not get back the amount invested.

Kalkine Media Limited, an affiliate of Kalkine Limited, may have received, or be entitled to receive, financial consideration in connection with providing information about certain entity(s) covered on its website.

Please wait processing your request...

Please wait processing your request...