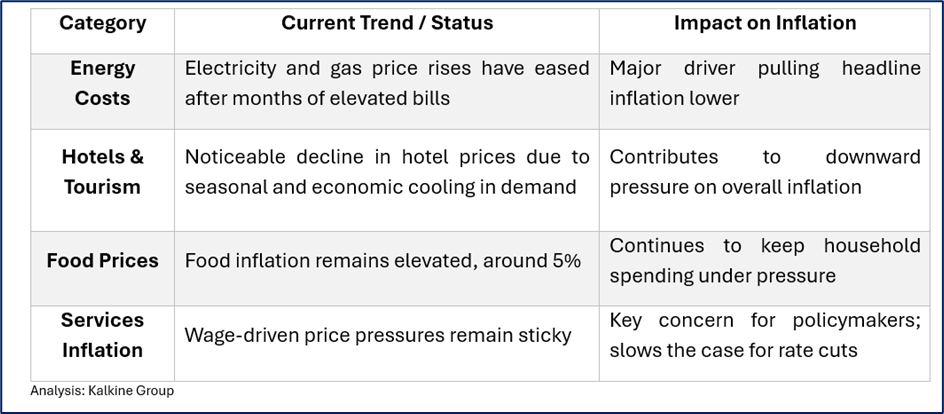

- UK inflation eased to 3.6%, the first fall in five months.

- Energy and hotel prices pulled inflation lower; food prices remain sticky.

- Easing inflation raises hopes for future rate cuts, supporting market sentiment.

- Rate-sensitive sectors such as real estate, utilities, banks, and growth stocks may benefit most if the trend continues.

- Defensive plays like consumer staples remain stable amid lingering cost pressures.

UK inflation eased to 3.6% in October, marking the first decline in five months and offering a cautiously optimistic signal for households, markets, and policymakers. The slowdown was driven by softer increases in energy costs, a pullback in hotel prices, and moderating corporate pricing pressure. Food inflation, however, remains stickier than expected.

This drop comes at a critical time, with businesses and investors watching closely whether the Bank of England could finally gain enough confidence to consider rate cuts in the coming months.

The latest figure lands at a time when:

- Borrowing costs remain at multi-decade highs

- UK consumers are still navigating a real-income squeeze

- Global markets are showing renewed volatility

- Government policy changes are expected post-Budget

A cooling inflation prints offers relief — but also raises deeper questions about which UK sectors may stabilise first, and which could benefit the most if inflation continues to ease.

- Interest Rate Cut Expectations May Strengthen

If inflation continues to trend lower in November–December, speculation may grow for a potential Bank of England rate cut early next year — a significant sentiment booster for rate-sensitive sectors.

- Bond Yields Could Stabilise

Softer inflation typically eases pressure on gilt yields, supporting property, utilities, and infrastructure names.

- Consumer Confidence Could Slowly Recover

Lower inflation doesn’t fix everything overnight, but it reduces the “cost-of-living drag,” helping confidence-sensitive sectors.

- Financials (Banks, Insurance)

Cooling inflation + potential rate cuts can improve loan growth, mortgage activity, and sentiment - though margins may narrow later.

Notable names: Lloyds Banking Group (LSE: LLOY), NatWest Group (LSE: NWG), Barclays (LSE: BARC), HSBC Holdings (LSE: HSBA), Aviva (LSE: AV), Legal & General Group (LSE: LGEN).

- Real Estate & Housebuilding

These sectors react fastest to rate expectations.

Lower inflation = lower gilt yields = improved valuations + demand recovery.

Names to watch: Barratt Developments (LSE: BDEV), Taylor Wimpey (LSE: TW), Berkeley Group Holdings (LSE: BKG), Land Securities Group (LSE: LAND), British Land Company (LSE: BLND).

- Utilities & Infrastructure

Stable inflation and falling rates make their dividend models more attractive, improving capital flows into defensive sectors.

Names: National Grid (LSE: NG), SSE (LSE: SSE), United Utilities Group (LSE: UU).

- Consumer Staples

With food inflation still elevated, this defensive category can stay relatively resilient.

Names: Tesco (LSE: TSCO), J Sainsbury (LSE: SBRY), Unilever (LSE: ULVR), Diageo (LSE: DGE).

- Technology & Growth Stocks

If rate-cut expectations accelerate, growth and tech names may see improved valuations due to lower discount rates.

Names: Darktrace (LSE: DARK), Sage Group (LSE: SGE), Ocado Group (LSE: OCDO).

- Retail & Consumer Discretionary

These recover slower - but easing inflation supports discretionary spending.

Names: Next (LSE: NXT), JD Sports Fashion (LSE: JD), Associated British Foods (LSE: ABF), B&M European Value Retail (LSE: BME).

The cooling of UK inflation to 3.6% is more than just another data point - it’s a potential turning point for the economy. While households continue to feel the squeeze, the latest reading hints that the sharpest pressures may be easing. For markets, the message is clear: If inflation continues to cool, sectors tied to interest rates, stability, and renewed consumer strength could regain momentum. The next few months especially inflation prints and Bank of England signals - will determine whether this is the start of a sustained downtrend or just a brief pause in a long inflation battle.

Please wait processing your request...

Please wait processing your request...