The Great AIM Rebound: Why Junior Stocks are Set to Outperform in 2026

The FTSE AIM All-Share index is entering 2026 at a critical valuation pivot. After years of being overshadowed by large-cap "Magnificent Seven" momentum, the UK’s junior market is witnessing a renaissance driven by a stabilization in interest rates and a renewed appetite for domestic growth stories.

Analysts from major houses like Peel Hunt and Panmure Liberum are increasingly vocal about the "valuation gap" between AIM-listed innovators and their global peers. As the UK economy shifts toward a recovery cycle, small-cap companies with lean balance sheets and scalable tech or consumer models are the primary candidates for double-digit re-ratings.

Source: Kalkine Group

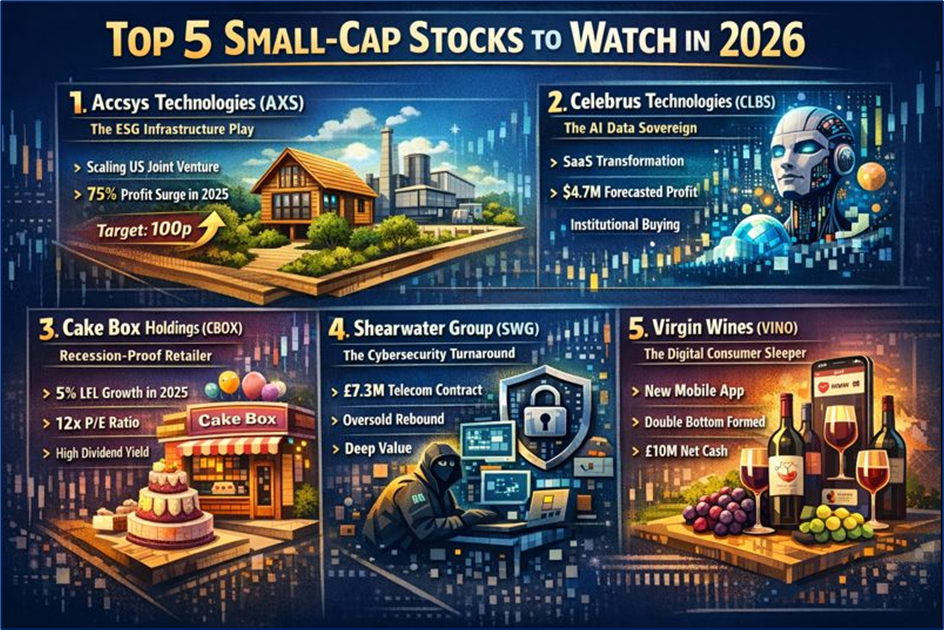

1. Accsys Technologies (LSE: AXS) – The ESG Infrastructure Play

Accsys is transforming the global timber industry through its proprietary acetylation process, creating "Accoya" wood—a high-performance, sustainable alternative to tropical hardwoods and carbon-heavy materials.

- Key Drivers & Business Model: The core driver for 2026 is the scaling of the Arnhem facility and the operational ramp-up of the US joint venture with Eastman. Their model is shifting toward higher-margin licensing and royalty streams alongside direct manufacturing.

- Latest Updates & Technicals: In late 2025, operating profits surged by nearly 75% as capacity utilization improved. Technically, the stock is emerging from a long-term rounding bottom base, with a key resistance level at 70p. A breakout here could signal a fast move toward 100p.

- Analysts & Risks: Recent upgrades from mid-cap specialists highlight the "breakeven pivot." However, the primary risk remains the sensitivity to global construction volumes and raw material costs.

2. Celebrus Technologies (LSE: CLBS) – The AI Data Sovereign

Celebrus specializes in first-party data capture and behavioral biometrics, helping blue-chip enterprises navigate the "death of the third-party cookie" while enhancing fraud prevention.

- Key Drivers & Business Model: The company has successfully transitioned to a high-visibility SaaS (Software as a Service) subscription model. Its "Instant Personalization" tool is being integrated into major banking and retail platforms as a first-line defense against AI-generated fraud.

- Latest Updates & Technicals: While interim results showed a temporary dip due to the subscription transition, 2026 forecasts predict a swing back to significant profitability (estimated $4.7M profit for 2027). The stock is currently consolidating in a tight range; volume spikes suggest institutional accumulation.

- Analysts & Risks: Panmure Liberum maintains a "Buy," citing a massive cash pile that covers roughly 50% of its market cap. The risk lies in the lengthy sales cycles of enterprise-level software contracts.

3. Cake Box Holdings (LSE: CBOX) – The Recession-Proof Retailer

A franchised retailer of egg-free, fresh cream celebration cakes, Cake Box has defied the UK retail gloom through a low-overhead, high-growth model.

- Key Drivers & Business Model: The primary catalyst is the successful integration of Ambala, an Indian sweets supplier, which has diversified their product range and footfall. Their "lite" franchise model allows for rapid expansion without heavy capital expenditure.

- Latest Updates & Technicals: Like-for-like sales grew by 5% in late 2025 despite a tough consumer backdrop. Technically, the stock is trending above its 200-day moving average, showing "sugary resilience" with a prospective P/E ratio that remains historically low at 12x for 2027.

- Analysts & Risks: Rated as a "Buy for Income and Growth," with a forecasted dividend yield exceeding 5%. The main risk is the potential for input cost inflation (dairy and sugar) to squeeze franchisee margins.

4. Shearwater Group (LSE: SWG) – The Cybersecurity Turnaround

Shearwater provides advanced cybersecurity services and software to government and corporate entities, a sector seeing unprecedented demand in the age of state-sponsored cyber threats.

- Key Drivers & Business Model: A new management focus on "contracted recurring revenue" rather than one-off consultancy is stabilizing the bottom line. A significant £7.3 million contract extension with a UK telecom giant serves as a blueprint for 2026 growth.

- Latest Updates & Technicals: After an accounting-led sell-off in 2025, the stock is currently trading at a "deep value" level. Technical indicators like the RSI suggest it is oversold, making it a classic "mean reversion" candidate for 2026.

- Analysts & Risks: Cavendish forecasts a return to pre-tax profit of £1.1 million for the 2025-26 period. The risk is the company's inconsistent historical execution and the competitive nature of the cyber-services market.

5. Virgin Wines (LSE: VINO) – The Digital Consumer Sleeper

One of the UK's largest direct-to-consumer online wine retailers, Virgin Wines is finally shaking off its post-IPO hangover.

- Key Drivers & Business Model: The launch of a high-tech mobile app in early 2026 and strategic partnerships with Ocado and Moonpig are driving down customer acquisition costs (CAC). Their "WineBank" subscription model provides a steady, predictable cash flow.

- Latest Updates & Technicals: Pre-tax profits are currently running ahead of analyst expectations. The stock has formed a "double bottom" on the weekly charts, a bullish signal for a long-term trend reversal.

- Analysts & Risks: With a market cap of roughly £27 million and nearly £10 million in net cash, the downside appears limited. The risk is a potential further decline in UK discretionary spending if inflation proves "stickier" than expected.

The Analytical Verdict: Is 2026 the Year for AIM?

The "risk-on" sentiment returning to the London Stock Exchange suggests that the highest alpha in 2026 will not be found in the FTSE 100 giants, but in the nimble, specialized players of the AIM. While liquidity remains lower in these stocks—meaning price swings can be more volatile—the fundamental recovery of these five businesses suggests they are significantly undervalued relative to their 12-month earnings potential.

Please wait processing your request...

Please wait processing your request...