On January 6, 2026, Hikma Pharmaceuticals PLC (LSE: HIK) emerged as a top performer on the FTSE 100, closing up approximately 4% (reaching an intra-day high of GBX 1,585). This surge marks a significant sentiment reversal following a turbulent end to 2025.

Key Drivers for the Jan 6 Surge

Source: Kalkine Group

The ~4% jump was primarily driven by a "relief rally" and specific fundamental triggers:

- Oversold Recovery: After a double-digit plunge in late 2025 due to a lowered medium-term outlook, technical indicators suggested the stock was oversold. Investors moved back in to capture a 4.04% dividend yield.

- Leadership Transition Stability: The market responded positively to the operational continuity under CEO Riad Mishlawi, who has temporarily taken direct control of the Injectables business following the departure of Dr. Bill Larkins.

- Biosimilar Momentum: Recent launches, including Starjemza® (ustekinumab) and the patented Tyzavan™, are beginning to show early market share gains, reassuring investors of the "high-value" pivot.

- US Onshoring Strategy: News of the $1 billion investment in US manufacturing by 2030 is acting as a hedge against potential 2026 trade tariffs, positioning Hikma as a "domestic" US supplier.

Latest Business Model & Operational Updates

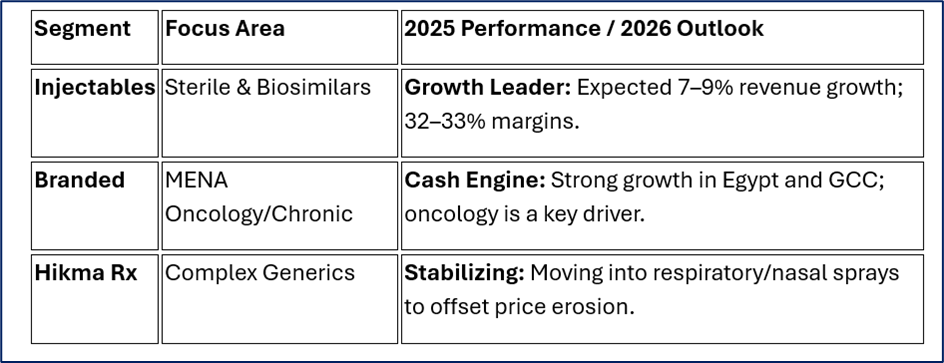

Hikma has transitioned from a pure-play generic provider to a specialty hybrid model focused on high-barrier sterile injectables.

Segment Performance (Current Status)

Source: Company Data

2026 Operational Strategy

- R&D Centralization: Moving from regional hubs to a global structure to accelerate complex product approvals.

- Manufacturing Realignment: Phased operationalization of the Bedford, Ohio facility (expected full capacity by late 2027) to handle the next generation of injectables.

SWOT Analysis

Source: Kalkine Group

Strengths

- Dominant MENA Position: Second largest pharma player in the Middle East.

- High-Barrier Injectables: Specialization in sterile manufacturing creates a wide competitive moat.

- Quality Metrics: High ROCE (~19%) and strong cash conversion.

Weaknesses

- Bedford Facility Delays: Pushing full revenue acceleration for new products to 2028.

- US Price Erosion: Continued deflationary pressure in the standard oral generics market.

- Execution Risk: Recent leadership turnover in the critical Injectables division.

Opportunities

- Biosimilar Explosion: Capturing a share of the $20B+ global biosimilar market.

- AI Integration: Utilizing generative AI in R&D to shorten the drug development cycle for 2026-2027.

- Contract Manufacturing (CMO): Growing the Columbus site to serve as a partner for Big Pharma.

Threats

- Geopolitical Turmoil: Potential supply chain disruptions or currency devaluations in MENA.

- US Tariff Policy: Uncertainty surrounding new tariffs on imported APIs (Active Pharmaceutical Ingredients).

- Regulatory Scrutiny: Increased FDA oversight on sterile manufacturing standards.

Key Risks to Monitor

- Margin Compression: While Injectables are high-margin, the company recently lowered medium-term margin guidance to ~30% due to higher R&D spend.

- Clinical/Regulatory Failure: High-value complex products carry a higher risk of FDA rejection compared to simple generics.

- Currency Volatility: Significant exposure to the Egyptian Pound and other MENA currencies remains a headwind for the Branded business.

Conclusion

The January 6th price action reflects a market that is beginning to look past the "reset" of 2025. While Hikma has adjusted its medium-term growth targets downward, the core fundamentals—driven by a shift toward complex injectables and a robust MENA footprint—remain intact. The recovery suggests that at current valuations (P/E ~12.8), the market perceives the "bad news" as fully priced in, focusing instead on the long-term goal of $5 billion in revenue by 2030.

Please wait processing your request...

Please wait processing your request...