As UK equities surge to historic highs, GSK has quietly re-emerged as one of the most compelling large-cap pharma stories in the FTSE 100. With strong price momentum, a stabilizing dividend profile, and renewed confidence in its specialty-medicine pipeline, investors are asking the big question: Is GSK stock a buy or sell in 2026?

This fully rephrased, SEO-focused analysis breaks down GSK’s latest catalysts, macro tailwinds, peer comparisons, broker forecasts, and actionable strategies—helping you decide where the stock fits in your portfolio today.

GSK Stock Snapshot: Key Highlights (January 2026)

- Share Price Performance: GSK is trading close to 1,850p, delivering a powerful +32% gain over the past 12 months.

- Recent Catalyst: Japan’s health authority approved Exdensur (depemokimab) for severe asthma and chronic rhinosinusitis with nasal polyps, triggering a 4.3% single-day rally.

- Dividend Outlook: Forecast 2026 dividend of 66p, up from 63.8p in 2025, implying a ~3.6% forward yield.

- Market Backdrop: The FTSE 100 closed at a record 10,122.73 on January 27, 2026, supported by easing inflation and currency stability.

- Earnings Watch: Q4 and full-year 2025 results due February 4, 2026—a potential volatility trigger.

Why Is GSK Stock Rising in January 2026?

GSK’s rally isn’t just riding the index—it’s company-specific. Since spinning off Haleon, GSK has fully refocused on vaccines, HIV, respiratory, and specialty medicines. Management now describes the company as a science-led biopharma, and the market is finally buying into that narrative.

The biggest near-term driver is depemokimab, now branded as Exdensur in Japan. Analysts increasingly view it as a multi-billion-pound blockbuster, reinforcing confidence that GSK’s R&D engine is back online.

Add to that the defensive appeal of large pharma during late-cycle economics, and GSK has become a natural beneficiary of the FTSE 100’s run above 10,000.

UK Economy & Currency: How the Macro Picture Supports GSK

Is the UK Economy Improving in 2026?

The Bank of England is signaling a shift toward a neutral interest rate range of 3.25%–3.50%, while major banks forecast ~1.4% UK GDP growth in 2026—stronger than much of the Eurozone. This steadier outlook is lifting sentiment across UK equities, especially global earners like GSK.

GBP/USD Impact on GSK Earnings

The British pound is holding near 1.25 vs the US dollar. Because GSK earns a substantial portion of revenue in dollars, a stable-to-slightly weaker pound creates a currency translation tailwind, boosting reported earnings in sterling terms.

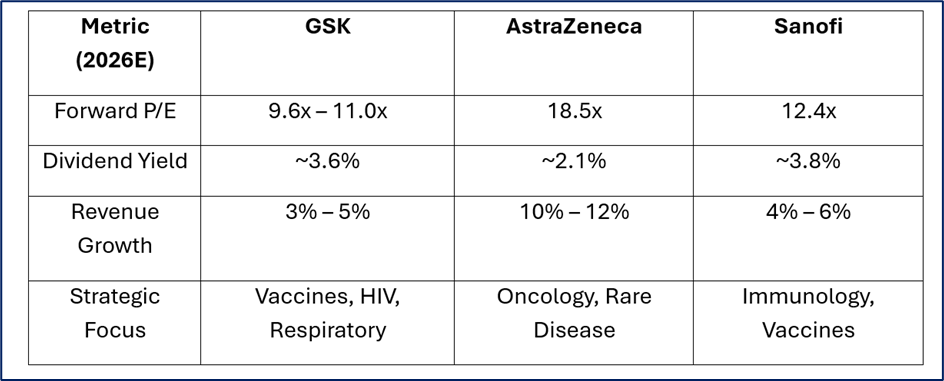

GSK vs Peers: How Does It Compare to AstraZeneca and Sanofi?

Source: Market Data

Compared with AstraZeneca, GSK clearly plays the value card. AstraZeneca commands a premium multiple thanks to oncology dominance, while GSK trades at a discount despite a materially improved pipeline—making it attractive to income and value-oriented investors.

GSK Stock Outlook for 2026: Bullish or Bearish?

Short-Term (3–6 Months): Bullish to Neutral

Momentum remains strong heading into earnings. A positive update on specialty medicines could push shares higher, though conservative guidance may spark short-term profit-taking.

Medium-Term (1–2 Years): Neutral

Investors remain cautious about the HIV patent cliff, particularly around dolutegravir later in the decade. Execution on newer launches like Arexvy (RSV vaccine) and Exdensur is critical to sustaining growth.

Long-Term (5+ Years): Bullish

GSK has upgraded its 2031 revenue target to £40+ billion and continues investing in next-generation platforms such as mRNA and oligonucleotides, positioning it well for long-term innovation-led growth.

Latest Broker Ratings & Price Targets for GSK

Analyst sentiment is balanced, with upside skewed toward valuation support:

- Jefferies – BUY | Target: 2,100p

Pipeline potential in respiratory and oncology still underappreciated. - Citigroup – NEUTRAL | Target: 1,900p

Concerned about mid-term growth as HIV exclusivity fades. - UBS – NEUTRAL | Target: 1,940p

Fair valuation reflects a balanced risk–reward setup. - Deutsche Bank – HOLD | Target: 1,675p

Long-term caution on HIV franchise durability.

Investor Strategy: How to Play GSK Stock in 2026

- Short Term: Buy on Pullbacks — Post-earnings dips could offer attractive entry points with dividend support.

- Medium Term: Track Pipeline Execution — Uptake of Exdensur and Arexvy is the key re-rating catalyst.

- Long Term: Reinvest Dividends — A reliable payout and mid-single-digit EPS growth make GSK ideal for ISA or SIPP compounding.

GSK Stock FAQ

Is GSK a good dividend stock in 2026?

Yes. The forecast yield above 3.5% and a payout ratio near 47% suggest strong dividend sustainability.

What are the main risks?

Pipeline execution risk, regulatory delays, residual litigation exposure, and long-term HIV patent expiries.

Why is the FTSE 100 at record highs?

Lower inflation expectations, easing rates, and strong performance from defensive sectors like pharma, energy, and banking.

Final Verdict: Should You Buy GSK Stock Today?

GSK currently looks like a High-Quality Hold with an Accumulation Bias. The company has shaken off years of underperformance, rebuilt investor trust, and now trades on a ~10x forward P/E, offering a solid margin of safety. While patent risks remain real, the improving pipeline and dependable dividend make GSK one of the most attractive defensive income stocks in the FTSE 100 for 2026.

Please wait processing your request...

Please wait processing your request...