Can Red-Hot Defense Stocks Run Rampant in 2026?

The unprecedented rally in UK defense and aerospace giants has transitioned from a recovery play into a structural "supercycle." Investors asking if the run is over are now being met with a wall of capital expenditure from Western governments.

The narrative for 2026 has shifted from simple recovery to multi-year growth visibility, driven by a fundamental reset in global security architecture. The "peace dividend" era is officially dead, replaced by a race for modernization, nuclear recapitalization, and sovereign capability. While valuations have expanded, the earnings power of these firms is being structurally re-rated higher.

Key Reasons & Strategic Drivers for 2026

Source: Kalkine Group

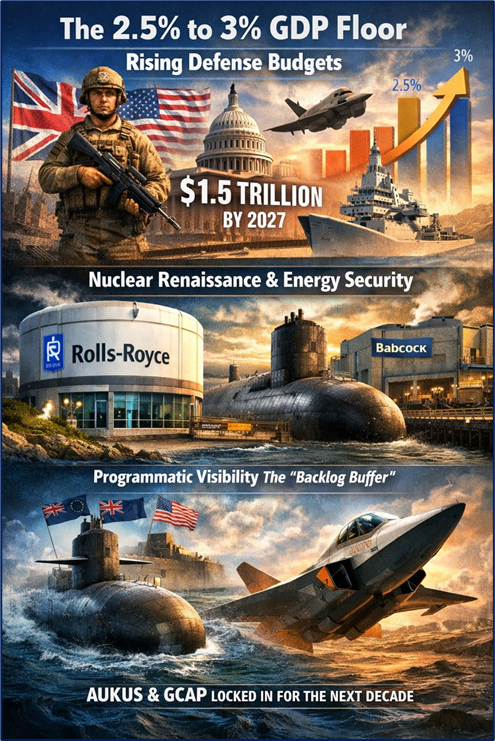

- The "2.5% to 3%" GDP Floor: NATO members are no longer aiming for 2%; they are sprinting past it. The UK government’s commitment to reach 2.5% of GDP on defense, combined with aggressive US budget proposals (potentially targeting $1.5 trillion by 2027), creates a rising tide that lifts all boats. This is not one-off spending; it is recurring, long-term program funding.

- Nuclear Renaissance & Energy Security: Beyond missiles and tanks, energy security has become synonymous with national defense. This specifically benefits Rolls-Royce (SMRs) and Babcock (nuclear submarine infrastructure), positioning them as dual-threat energy/defense plays.

- Programmatic Visibility (The "Backlog Buffer"): Unlike consumer stocks, these companies have locked in revenue for the next decade. Major multi-national programs like AUKUS (submarines) and GCAP (Tempest fighter jet) provide an earnings safety net that insulates them from broader economic recessions.

Company-Specific Analysis: Business Models & Operational Updates

- Business Model Pivot: CEO Tufan Erginbilgic’s "transformation" is largely complete, shifting focus now to high-margin durability. The strategic pivot is twofold: dominating the widebody civil market (cash cow) while aggressively commercializing Small Modular Reactors (SMRs) to own the future of mid-sized nuclear power.

- Operational Update: Civil aerospace engine flying hours have returned to pre-pandemic levels, restoring the high-margin "Power by the Hour" service revenue. Crucially, RR has achieved "Preferred Bidder" status for UK SMR deployment, a potential multi-billion pound revenue stream commencing in the late 2020s but priced in by forward-looking markets now.

- Financial Health: Free cash flow has surged, allowing for a resumption of dividends and a push toward investment-grade credit rating status.

- Business Model Pivot: BAE has evolved from a hardware manufacturer into a full-spectrum integrator. The new frontier is "Multi-Domain Integration"—connecting space, cyber, and physical platforms. The acquisition of Ball Aerospace in the US has cemented their foothold in the high-growth space and sensing sector.

- Operational Update: The order backlog is at record levels (surpassing £60bn+), providing exceptional earnings visibility. Recent operational highlights include the acceleration of the Type 26 Frigate program and confirmed orders for the next batch of Typhoon jets for export markets.

- Financial Health: Guidance for 2025/2026 suggests sales growth of 8-10%, with margins expanding as supply chain inflation eases and fixed-price contracts roll off.

- Business Model Pivot: Babcock has successfully shed its "conglomerate discount" by selling non-core civil businesses to become a pure-play defense support specialist. They are the "mechanics" of the military—they don't just build the ships; they run the dockyards and maintain the nuclear submarines.

- Operational Update: The turnaround story is arguably the most potent here. Operational margins are on track to hit the 8-9% target earlier than expected (potentially FY26). The company is deeply embedded in the AUKUS submarine maintenance structure, a role that guarantees work for decades.

- Financial Health: The balance sheet has been repaired, debt leverage is low, and the reinstatement of dividends signals management confidence. Analysts view Babcock as having the most "catch-up" potential in terms of valuation re-rating compared to RR and BAE.

Latest Analysts Upgrade or Downgrades

- Rolls-Royce: Sentiment remains largely "Overweight" or "Buy," though some caution is emerging regarding valuation multiples. JP Morgan recently raised price targets, citing the SMR potential and civil aerospace pricing power. However, some boutique firms have moved to "Hold," suggesting the easy money has been made and the stock is priced for perfection.

- BAE Systems: Consensus remains a strong "Buy." Analysts highlight BAE as a core portfolio holding for defensive stability. Recent notes emphasize the "Space" division as an underappreciated growth engine that warrants a higher P/E multiple.

- Babcock: Recently saw a significant upgrade from Citi, which hiked its price target aggressively (nearly doubling it in some models) based on the "margin expansion acceleration" thesis. The consensus is shifting from "Turnaround Play" to "Quality Growth."

Current Technical Analysis: Momentum & Levels

The technical structure for the sector remains bullish but overextended on weekly timeframes, suggesting consolidation may occur before the next leg up in 2026.

- Trend: All three stocks are trading above their 200-day and 50-day moving averages, confirming a strong primary uptrend.

- Momentum: RSI (Relative Strength Index) levels have occasionally flirted with "overbought" territory (>70), particularly for Rolls-Royce. This often leads to short-term pullbacks which institutional investors have been using as buying opportunities.

- Breakouts: BAE Systems recently broke out of a multi-month consolidation rectangle, signaling a continuation of the trend. Babcock is forming a "bull flag" pattern on monthly charts, often a precursor to a secondary breakout. Rolls-Royce faces psychological resistance at whole-number round figures, where profit-taking is most active.

Risks to the Bull Thesis

- Valuation Compression: These stocks are no longer cheap value plays. They are priced for growth. Any disappointment in earnings or margin guidance could lead to a sharp multiple contraction.

- Supply Chain Fragility: Ramping up production (e.g., ammunition, engines) is difficult due to shortages in skilled labor and raw materials (titanium, specialty steels). Delays could hurt cash flow.

- Political Volatility: While defense spending is bipartisan, changes in UK tax policy or US foreign policy (e.g., sudden shifts in NATO commitments by a US administration) could introduce volatility.

Conclusion

The "red-hot" run for Babcock, Rolls-Royce, and BAE Systems has legs to continue into 2026, but the nature of the returns will change. The explosive "recovery" gains of 2023-2024 will likely be replaced by steady "compounder" growth driven by margin expansion and buybacks. BAE Systems offers the safest floor due to its backlog; Rolls-Royce offers the highest ceiling via its nuclear optionality; and Babcock offers the best relative value as it completes its turnaround. The sector remains a "Buy on Dips" for investors seeking exposure to the geopolitical supercycle.

Please wait processing your request...

Please wait processing your request...