Associated British Foods PLC (LSE: ABF)

Associated British Foods PLC (LSE: ABF) a constituent of the FTSE 100 index, operates as a diversified conglomerate with a portfolio spanning food production and retail. The company is structured into five key divisions: Grocery, Ingredients, Agriculture, Sugar, and Retail. Its Grocery division specializes in manufacturing a broad range of food products, including hot beverages, sweeteners, vegetable oils, balsamic vinegars, baked goods, cereals, ethnic foods, and meat products. These products are distributed through retail, wholesale, and foodservice channels, serving diverse consumer and commercial markets. This Report covers the Key Recommendation Rationale, Conclusion, and Recommendation on the stock.

Key Recommendation Rationale – Sell at GBX 2,221.00

- Resistance near Current levels: ABF’s stock price has approached Resistance (R1) which was stated in the previous report on 03 October 2025 therefore, there can be a possibility of a decline from resistance levels. Considering the market conditions and the price action, it is prudent to exit the stock.

- Underperformance and Uncertainty in the Sugar Division Remain a Drag - Despite restructuring efforts and the closure of the Vivergo bioethanol plant, ABF's Sugar segment continues to underperform, with full-year sales expected to decline by around 10% and adjusted operating profit only expected to break even. The UK and Spanish markets are still challenged by persistently low European sugar prices and high input costs, notably for beet. The group is also absorbing £200 million in restructuring and impairment charges linked to the closure of Vivergo and the overhaul of its Spanish sugar operations. These developments suggest that the turnaround in this division will be slower and more expensive than previously anticipated, with profitability not expected to fully recover in the near term.

- Primark Growth Stagnation Highlights Exposure to Consumer Caution - While Primark remains a major contributor to group performance, sales growth in H2 is expected to be only 1%, with like-for-like sales falling 2%. The retailer is relying heavily on new store openings to support overall sales growth, masking weakness in organic performance. Even in its largest market, the UK and Ireland, like-for-like sales are expected to be flat, despite a trading period. Performance in key continental markets like France and Italy is particularly weak, with sales projected to decline by 4%. This highlights Primark's exposure to the weaker European retail environment and raises questions about the sustainability of its low-cost operating model amid ongoing inflationary pressures and rising costs tied to brand and digital investment.

Valuation Methodology: Price/ Earnings Approach

Share Price Chart

ABF Daily Technical Chart, Source - Refinitiv

Conclusion

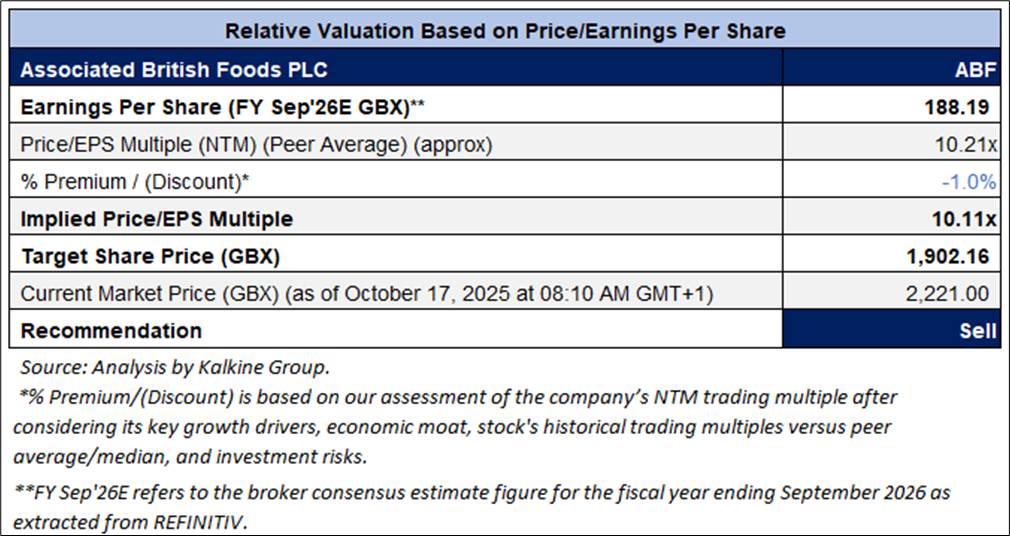

ABF is expected to trade at a discount, considering Primark Growth Stagnation and fears of global slowdown. For conducting the valuation, the following peers have been considered - Next PLC (LSE: NXT), Marks and Spencer Group PLC (LSE: MKS) and others.

Given its current trading levels, Underperformance and Uncertainty in the Sugar Division, recent rally in the share price, relative valuation, and associated risks, it is prudent to exit the stock at the current levels. Hence, a ‘Sell’ recommendation is given on the stock at the Current Market Price of GBX 2,221.00 as of 17 October 2025 at 08:10 AM GMT+1.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is 17 October 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and/or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Note 6: Dividend Yield may vary as per the stock price movement.

Please wait processing your request...

Please wait processing your request...