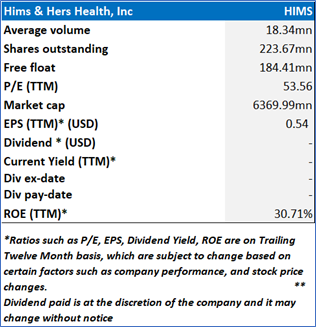

Hims & Hers Health, Inc

Hims & Hers Health, Inc (NYSE: HIMS) offers a customer-centric platform designed to meet a wide range of health and wellness needs. The platform features access to a network of healthcare providers, a clinically oriented electronic medical records system, digital prescription services, cloud-based pharmacy fulfillment, and personalized care solutions.

Rationale – Sell at USD 35.04

- Declining Gross Margins: Despite the company's strong revenue growth, gross margins declined notably in both Q4 and the full year 2024. For Q4, gross margin dropped from 83% in 2023 to 77% in 2024, while for the full year, it declined from 82% to 79%. This margin compression suggests that the cost of delivering services is rising faster than revenue, potentially due to increased costs associated with scaling, customer acquisition, or fulfillment of high-demand offerings such as GLP-1-based weight loss treatments. If this trend continues, it could undermine future profitability despite top-line growth.

- Heavy Dependence on GLP-1 Offering: A significant portion of Hims & Hers’ growth in 2024 was driven by its weight loss product line, including GLP-1 treatments. Revenue excluding this offering only grew 43% year-over-year, compared to the 69% overall increase, suggesting heavy reliance on this single category for acceleration. This raises concerns about the sustainability of revenue growth if market dynamics, regulatory scrutiny, or supply chain issues affect the GLP-1 space. Overreliance on a trend-sensitive segment can pose strategic risks if diversification efforts stall.

- Slowing Efficiency Gains in Subscriber Monetization: While subscriber numbers rose 45% year-over-year to 2.2 million, the increase in monthly online revenue per average subscriber was less pronounced—up 19% year-over-year. This gap suggests a potential plateau in monetization efficiency. The significant rise in AOV (average order value) and net orders may be driven more by higher-priced offerings (e.g., GLP-1s) rather than improved cross-sell or recurring usage patterns across the platform. This could point to challenges in driving long-term value from the expanding user base beyond the core high-demand treatments.

- Reduced Visibility into Net Income Outlook: The company refrained from providing net income guidance for 2025, citing unpredictability in certain reconciliation components, particularly those affected by market assumptions. This lack of visibility limits investor confidence in the company’s ability to consistently convert revenue into bottom-line profitability. Moreover, the 2024 net income of $126 million was heavily influenced by a one-time $68 million tax valuation allowance release, which inflates profitability and complicates year-over-year comparisons.

- Falling Short on Margin Expansion Targets: Despite notable improvements in adjusted EBITDA, the company's EBITDA margin guidance for 2025 (12% to 13%) only reflects a modest increase from 2024’s full-year margin of approximately 12%. This may disappoint investors seeking stronger operational leverage given the scale benefits of a digital platform business. The limited margin expansion implies rising cost pressures or increasing investment needs, particularly in marketing, R&D, or operational infrastructure to support the growing customer base.

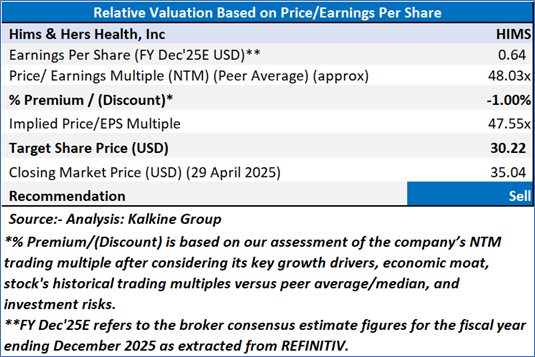

Valuation (Using P/E Methodology)

Share Price Chart

Conclusion

Despite strong revenue and subscriber growth in 2024, Hims & Hers Health faces several challenges. Gross margins declined year-over-year, indicating rising costs. Much of the company’s growth is tied to its GLP-1 weight loss offering, raising concerns about overreliance on a single product category. Monetization per subscriber is improving at a slower pace than subscriber growth, suggesting potential limits to customer lifetime value. Net income in 2024 was boosted by a one-time tax benefit, and the company offered no net income guidance for 2025, reducing financial clarity. Additionally, only modest margin expansion is expected, and the ambitious growth strategy introduces execution risks as the company scales into new healthcare verticals.

Based on the notional gains, valuation downside and price action stance, a "SELL" recommendation on Hims & Hers Health, Inc (NYSE: HIMS) has been given at the closing market price of USD 35.04 as on 29 April 2025.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is 29 April 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Note 6: Dividend Yield may vary as per the stock price movement.

Please wait processing your request...

Please wait processing your request...