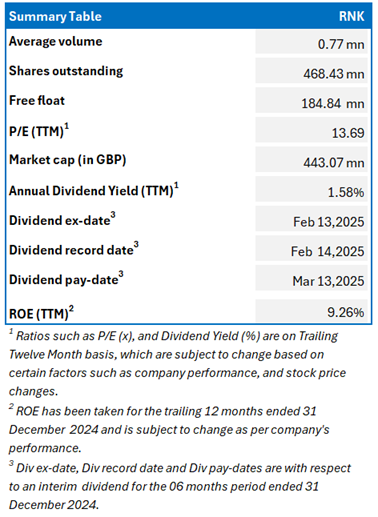

Rank Group PLC

Rank Group PLC (LSE: RNK) is an FTSE All-Share listed international gaming company based in the United Kingdom, offering its services both in physical venues and through online platforms. It operates across several regions, including Great Britain (with the Channel Islands), Spain, and India. The company’s operations are divided into five segments: Digital, Grosvenor venues, Mecca venues, Enracha venues, and Central costs. This Report covers the Key Recommendation Rationale, Conclusion, and Recommendation on the stock.

Key Recommendation Rationale – Sell at GBX 95.00

- Resistance near Current levels: RNK’s stock price crossed the Resistance (R1) which was stated in the previous report on 11 April 2025 therefore, there can be a possibility of a decline in resistance levels. Considering the market conditions and the price action, it is prudent to exit the stock.

- Operational Update Q3 FY25: Mecca venues continued to struggle with footfall, as customer visits declined by 1.8% year-over-year in Q3 FY25, partially offset by a 3.8% rise in spend per visit, reflecting pressure on volume-driven recovery. Spanish digital operations underperformed, with NGR declining 2.9% year-over-year, indicating weakness in international digital engagement despite strong growth in the UK.

- Decline in Net Free Cash Flow: Net free cash flow dropped by 82%, falling from £23.5mn in H1 2023/24 to just £4.3mn in H1 2024/25. This sharp decline was driven by higher capital expenditure of £27.3mn (up 41% YoY) and increased working capital outflows, despite stronger underlying profits.

- Surge in Employment Costs Amid Regulatory Headwinds: Like-for-like employment costs rose significantly from £118.9mn (H1 FY24) to £133.6mn in H1 FY25, reflecting the impact of inflation and tighter labour markets. These pressures are expected to intensify in FY25 due to upcoming increases in the National Living Wage and employer national insurance contributions.

- Macroeconomic Risk: The market sentiments can remain weak in the short term due to the subdued consumer disposable income, geopolitical tensions, and political risks.

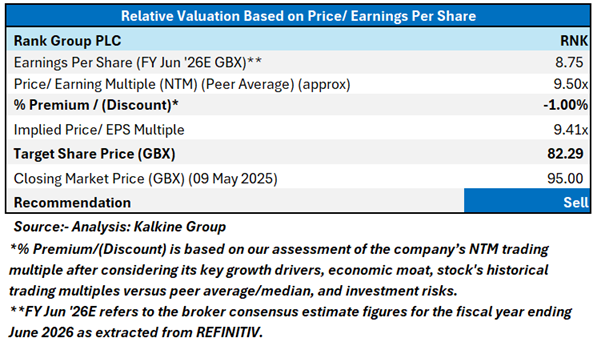

Valuation Methodology: Price/ Earnings Approach

Share Price Chart

Conclusion

RNK is expected to trade at a discount, weighed down by continued footfall challenges at Mecca venues, a 2.9% YoY decline in Spanish digital NGR during Q3 FY25, a significant drop in net free cash flow, and rising employment costs, which increased from £118.9mn to £133.6mn in H1 FY25. Additionally, higher tax expenses and ongoing structural cost burdens—including policy-related disadvantages and persistent inflation—are likely to constrain profitability. For conducting the valuation, the following peers have been considered: Evoke PLC (LSE: EVOK), Whitebread PLC (LSE: WTB), etc.

Given its current trading levels, the recent financial performance, strategic investments and partnerships, market expansion and cost optimization strategies, relative valuation, and associated risks, it is prudent to exit the stock at the current levels. Hence, a ‘Sell’ recommendation is given on the stock at the Closing Market Price of GBX 95.00 as of 09 May 2025.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is 09 May 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Note 6: Dividend Yield may vary as per the stock price movement.

Please wait processing your request...

Please wait processing your request...