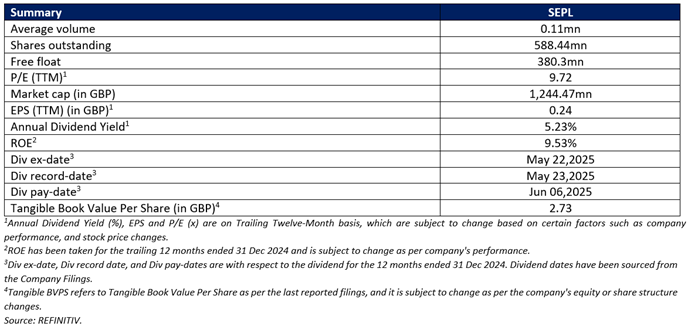

Seplat Energy PLC

Seplat Energy PLC (LSE: SEPL) is an FTSE index listed company specializing in oil and gas exploration and production and gas processing activities. The Company's segments include Oil and Gas. The Oil segment deals with the exploration, development and production of crude oil. The Gas segment deals with the production and processing of gas. It has equity in approximately 11 blocks in onshore and shallow water Nigeria, 48 producing oil and gas fields, five gas processing facilities, and three export terminals. Its portfolio consists of interests in seven oil and gas assets in the Niger Delta region of Nigeria.

Key Recommendation Rationale – Sell at GBX 212.30

- Resistance near Current levels: SEPL’s stock price crossed the Resistance (R1) which was stated in the previous report on 02 Apr 2025 therefore, there could be a possibility that the stock might consolidate or decline from the current levels, considering overstretched valuation. Considering the market conditions and the price action, it is prudent to exit from the stock.

- Decline in Realized Prices of Oil & Gas: The average realized oil price declined by ~11.3% to USD 76.42 per barrel in Q1 FY25, and the gas price dropped by ~3.2% to USD 3.01 per Mscf in same period compared to Q1 2024. Although, production and volumes lifted saw growth, the lower pricing limits revenue upside and compresses margins, particularly in a persistently volatile global energy market.

- Rising Production Cost: Seplat reported unit production costs of USD 12.6/boe in Q1 FY25, which marks an approximate ~32.6% increase compared to USD 9.5/boe in Q1 2024. This rise is partly due to the timing of maintenance activities but also indicates increased operational intensity. Continued cost increases, combined with weak pricing, could potentially impact profitability.

- Higher Royalty Burden May Signal Less Favourable Mix: Royalties rose by 156% to USD 130.2 mn Q1 FY25. Although this aligns with the growth in revenue, the increase suggests a greater fiscal load or a shift in production towards assets with higher royalty obligations.

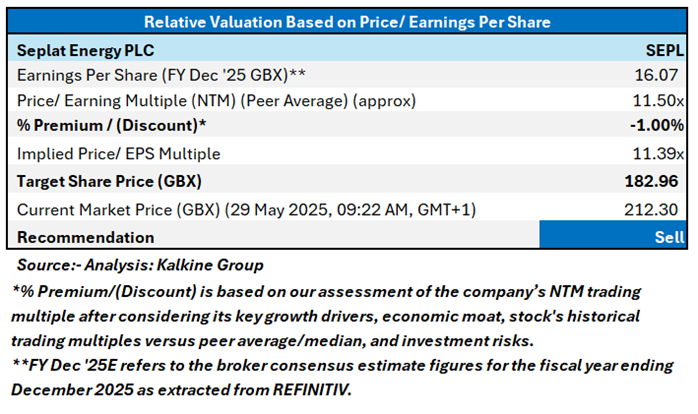

Valuation Methodology: Price/ Earnings Approach

Share Price Chart

One-Year Technical Price Chart (as of May 29, 2025). Source: REFINITIV, Analysis: Kalkine Group

Conclusion

While Q1 2025 results show notable growth in revenue and production volumes, certain underlying metrics raise concerns. There is a decline in realized prices of both oil –11.3% and gas –3.2% compared to Q1 2024, which can affect earnings sustainability if pricing remains under pressure. The increase in unit production cost to USD 12.6/boe, a 32.6% rise from USD 9.5/boe last year, signals higher operational expenditure, even though it remains below current guidance. Additionally, royalty expenses rose by 156%, outpacing revenue growth, which may reflect a shift toward assets or terms with higher fiscal obligations, thereby narrowing the effective margin. Given these trends—lower realizations, rising costs, and increasing royalty obligations—the overall financial efficiency appears to be tightening. These factors may weigh on future profitability if not managed carefully.

SEPL appears overvalued. For conducting the valuation, the following peers have been considered: Zephyr Energy PLC (LSE: ZPHR), Energean PLC (LSE: ENOG), etc

Given its current trading levels, the recent strategic investments and partnerships, relative valuation, and associated risks, it is prudent to exit the stock at the current levels. Hence, a ‘Sell’ recommendation is given on the stock at the Current Market Price of GBX 212.30 as of 29 May 2025, 09:22 AM, GMT+1.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is 29 May 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Please wait processing your request...

Please wait processing your request...