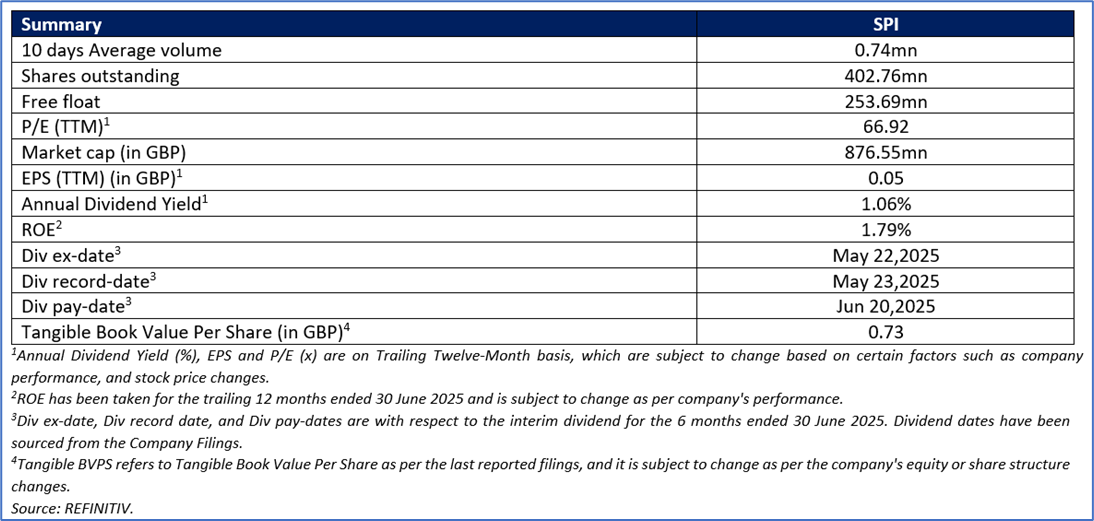

Spire Healthcare Group PLC

Spire Healthcare Group PLC (LSE: SPI) is a UK-based company listed at FTSE 250, managing private hospitals and clinics. The organization offers diverse healthcare services, including treatment for allergies, infectious diseases, cancer diagnostics, and cosmetic and general surgeries. It also specializes in areas like cardiology, neurology, pediatrics, and dental care. Additionally, Spire provides diagnostic services such as CT scans, MRI scans, ultrasounds, and X-rays to enhance patient care.

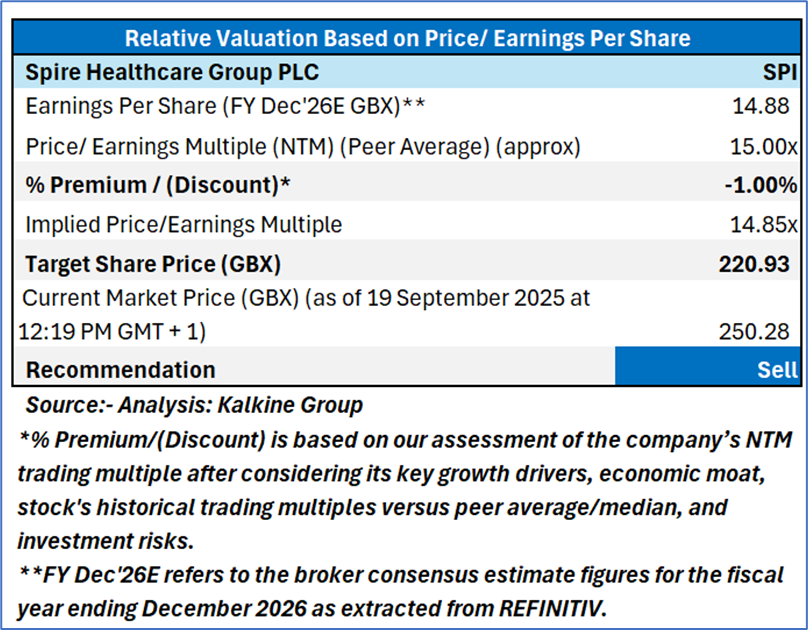

Key Recommendation Rationale – Sell at GBX 250.28

- Resistance near Current levels: SPI’s stock price crossed the Resistance (R2) which was stated in the previous report on 11 September 2025 therefore, there could be a possibility that the stock might consolidate or decline from the current levels, considering overstretched valuation. Considering the market conditions and the price action, it is prudent to exit from the stock.

- Declining Profitability Metrics: The company's statutory profit before tax decreased significantly by 52.4% to £10.8 million. This sharp decline was primarily driven by £13.0 million in adjusting items, largely from costs associated with restructuring and headcount reductions. While these are presented as one-off costs, their magnitude materially impacts the bottom line and raises questions about the near-term financial cost of the business transformation.

- Weak Performance in Core Private Payor Segments: Revenue from private patients, a core market, showed minimal growth of just 0.8%. Within this, self-pay revenue declined by 2.6%, and while Private Medical Insurance (PMI) revenue saw some growth, it was attributed to price increases that offset a decline in volumes. The report notes "softer" PMI volumes due to insurers tightening claims access, indicating potential headwinds and competitive pressures in the group's primary revenue streams.

Valuation Methodology: Price/ Earnings Approach

Share Price Chart

One-Year Technical Price Chart (as of September 19, 2025). Source: REFINITIV, Analysis: Kalkine Group

Conclusion

The decline in statutory profit, driven largely by substantial restructuring costs, raises concerns regarding the execution and financial burden of the group's transformation strategy. While positioned as a one-off investment, the magnitude of these charges materially impacts reported earnings, and shareholder returns in the near term. This presents a risk that the promised future benefits and cost savings may be delayed, may not fully materialize as expected, or could be offset by further unforeseen expenses associated with such a large-scale operational overhaul. The strategy carries a notable degree of execution risk.

For conducting the valuation, the following peers have been considered: Kooth PLC (LSE: KOO), CVS Group PLC (LSE: CVSG), etc

Given its current trading levels, the recent strategic investments and partnerships, relative valuation, and associated risks, it is prudent to exit the stock at the current levels.

Hence, a ‘Sell’ recommendation is given on the stock at the Current Market Price of GBX 250.28 as of 19 September 2025 at 12:19 PM GMT + 1.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is 19 September 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Please wait processing your request...

Please wait processing your request...