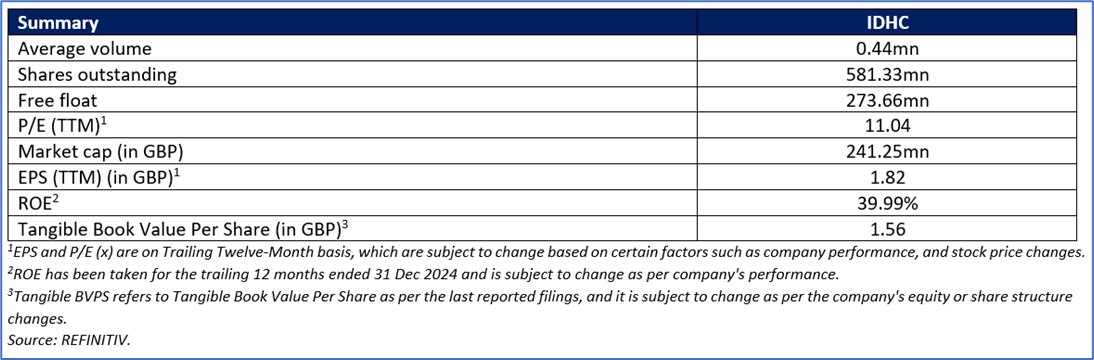

Integrated Diagnostics Holdings PLC

Integrated Diagnostics Holdings PLC (LSE: IDHC) is an integrated diagnostics services provider in Egypt. The Company operates in three geographic areas: Egypt, Sudan, and Jordan. The Company provides over 1,000 diagnostic services ranging from basic tests to molecular tests for hepatitis and specialized deoxyribonucleic acid (DNA) tests to patients and operates approximately 310 branches.

Key Recommendation Rationale – Sell at USD 0.42

- Resistance near Current levels: IDHC’s stock price breached the Resistance (R2) which was stated in the previous report on 15 May 2025 therefore, there could be a possibility that the stock might consolidate or decline from the current levels, considering overstretched valuation. Considering the market conditions and the price action, it is prudent to exit from the stock.

- Decline in Net Profit Due to Reduced FX Gains: IDHC’s net profit contracted 39.0% year-on-year in Q1 2025, primarily due to a normalization of foreign exchange gains compared to the previous year. While the company highlights an improvement in "normalized" net profit, the reported bottom-line decline may raise concerns among investors about the sustainability of earnings without currency fluctuations. The sharp drop in net profit margin (from 34.3% to 15.5%) could indicate vulnerability to external macroeconomic factors beyond operational control.

- Volume Decline in Key Markets Despite Revenue Growth: Revenue growth was driven by higher pricing rather than volume expansion, with patient numbers declining by 8.0% and test volumes dropping by 1.0% year-on-year. The company attributes this to Ramadan timing, but persistent volume declines in Egypt (the largest market) and Nigeria (where test volumes fell 6.0%) suggest underlying demand pressures. If pricing adjustments cannot continue at the same pace, future revenue growth may face constraints.

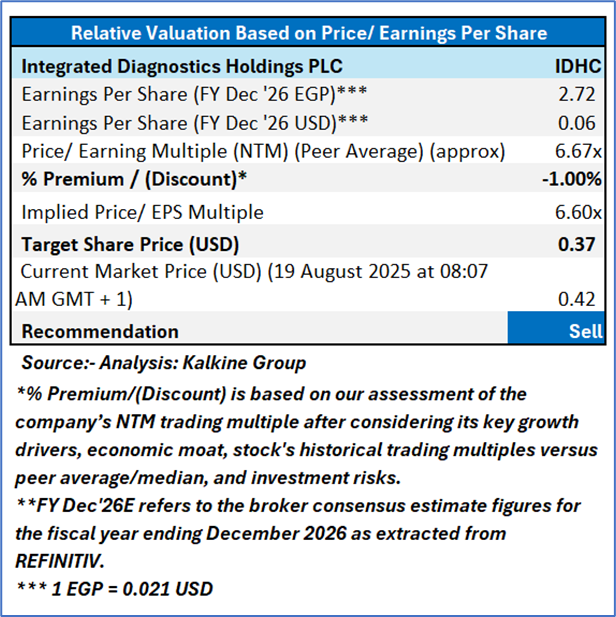

Valuation Methodology: Price/ Earnings Approach

Share Price Chart

One-Year Technical Price Chart (as of August 19, 2025). Source: REFINITIV, Analysis: Kalkine Group

Conclusion

IDHC’s Q1 2025 results reflect a mixed performance, with revenue growth driven by pricing adjustments rather than volume expansion. The decent decline in net profit, largely due to reduced foreign exchange gains, raises questions about earnings sustainability in the absence of favourable currency movements. While operational efficiencies supported margin improvements, the contraction in test and patient volumes—particularly in core markets like Egypt and Nigeria—suggests potential demand-side challenges that could limit future growth if pricing power weakens. IDHC appears overvalued. For conducting the valuation, the following peers have been considered: Kooth PLC (LSE: KOO), Uniphar PLC (LSE: UPR), etc

Given its current trading levels, the recent strategic investments and partnerships, relative valuation, and associated risks, it is prudent to exit the stock at the current levels.

Hence, a ‘Sell’ recommendation is given on the stock at the Current Market Price of USD 0.42 as of 19 August 2025 at 08:07 AM GMT + 1.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is 19 August 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided have been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5:‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Please wait processing your request...

Please wait processing your request...