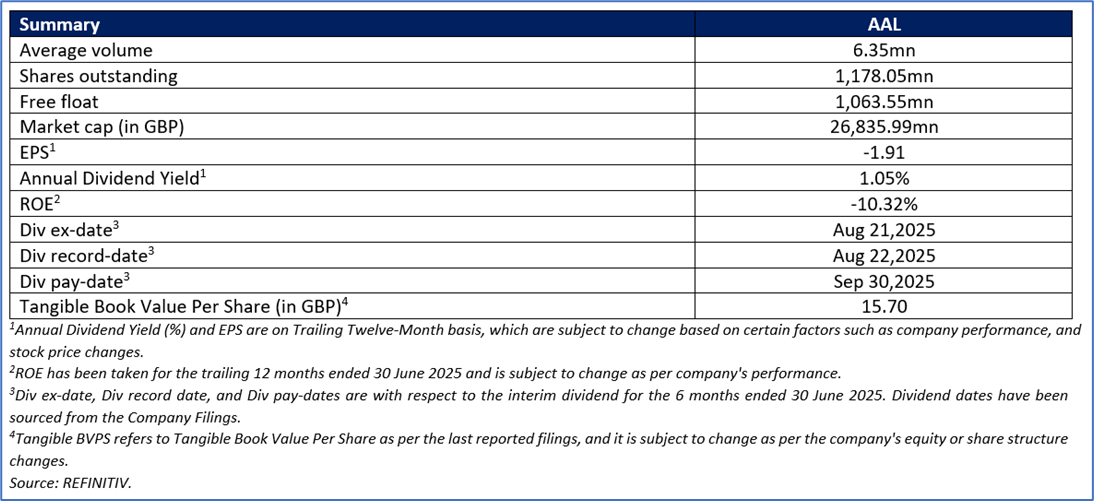

Anglo American PLC

Anglo American PLC (LSE: AAL) is a mining company which is listed under the FTSE 100 index with a portfolio of undeveloped resources, mining, and processing operations. The company’s operations are segmented into Platinum Group Metals, Iron Ore, Manganese, Copper, DeBeers, and Crop Nutrients. This Report covers the Investment Highlights, Conclusion, and Recommendation on the stock.

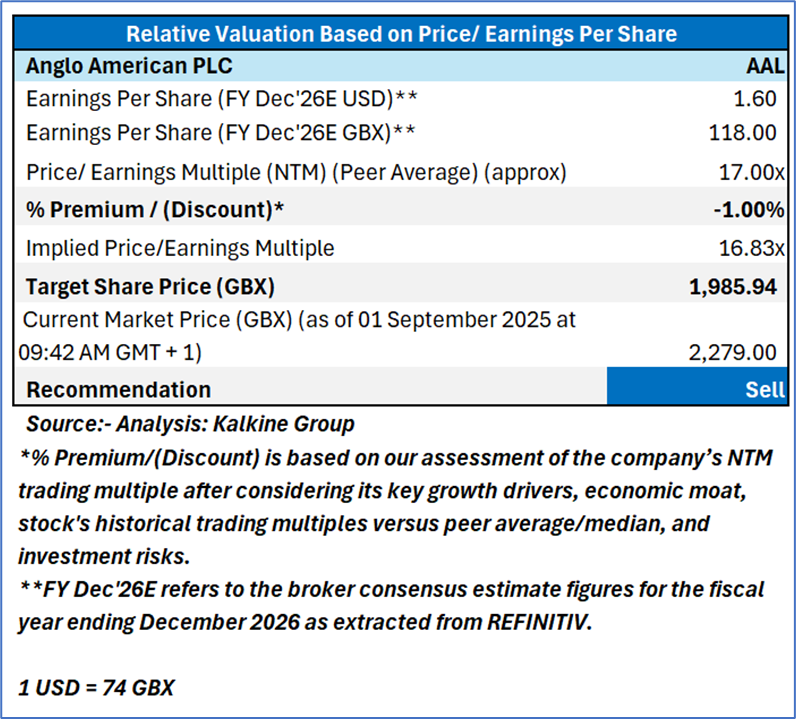

Key Recommendation Rationale – Sell at GBX 2,279.00

- Resistance near Current levels: AAL’s stock price breached the Resistance (R2) which was stated in the previous report on 09 April 2025 therefore, there could be a possibility that the stock might consolidate or decline from the current levels, considering overstretched valuation. Considering the market conditions and the price action, it is prudent to exit from the stock.

- Earnings Contraction and Profitability Decline: The company reported a substantial decline in its financial performance. Underlying EBITDA from continuing operations fell by 20% to USD 3.0 billion, down from USD 3.7 billion in the same period last year. Basic underlying earnings per share from total operations experienced a severe 86% decrease to USD 0.15. This contraction is attributed to challenging market conditions, particularly in diamonds, and lower production volumes in key divisions like copper, indicating underlying operational and market headwinds that are pressuring profitability.

- Deteriorating Debt Position and Elevated Leverage: Anglo American's net debt increased to USD 10.8 billion, prior to receiving proceeds from planned asset sales. This has resulted in a net debt to EBITDA ratio rising to 1.8x, up from 1.3x at the end of 2024. The ratio is described as "temporarily elevated," but it reflects a period where debt levels are growing while earnings are shrinking. The company's reliance on the successful completion and receipt of proceeds from its portfolio simplification strategy to deleverage introduces a element of execution risk to its balance sheet health.

Valuation Methodology: Price/ Earnings Approach

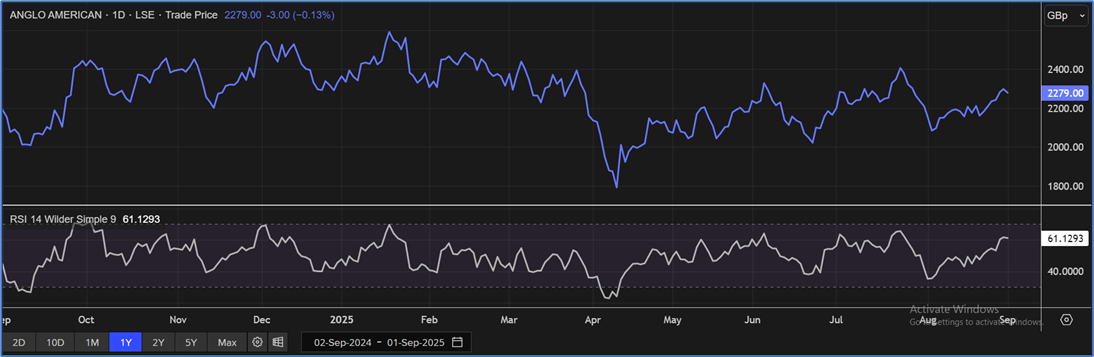

Share Price Chart

One-Year Technical Price Chart (as of September 01, 2025). Source: REFINITIV, Analysis: Kalkine Group

Conclusion

The company is experiencing a period of financial strain, characterized by a contraction in earnings and a decline in profitability. This is evidenced by a reduction in underlying EBITDA and a pronounced decrease in earnings per share, primarily driven by adverse market conditions and lower operational output. Concurrently, the company's financial leverage has increased, as reflected in a higher net debt to EBITDA ratio. This elevation in leverage coincides with a reduction in earnings, indicating a narrowing capacity to service its debt obligations. The organization's strategy to address its balance sheet is contingent upon the execution of its asset disposal plans, introducing a degree of uncertainty regarding the timeline and successful completion of these financial deleveraging actions.

For conducting the valuation, the following peers have been considered: South32 Ltd (LSE: S32), BHP Group Ltd (LSE: BHP), etc

Given its current trading levels, the recent strategic investments and partnerships, relative valuation, and associated risks, it is prudent to exit the stock at the current levels.

Hence, a ‘Sell’ recommendation is given on the stock at the Current Market Price of GBX 2,279.00 as of 01 September 2025 at 09:42 AM GMT +1.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is 01 September 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Please wait processing your request...

Please wait processing your request...