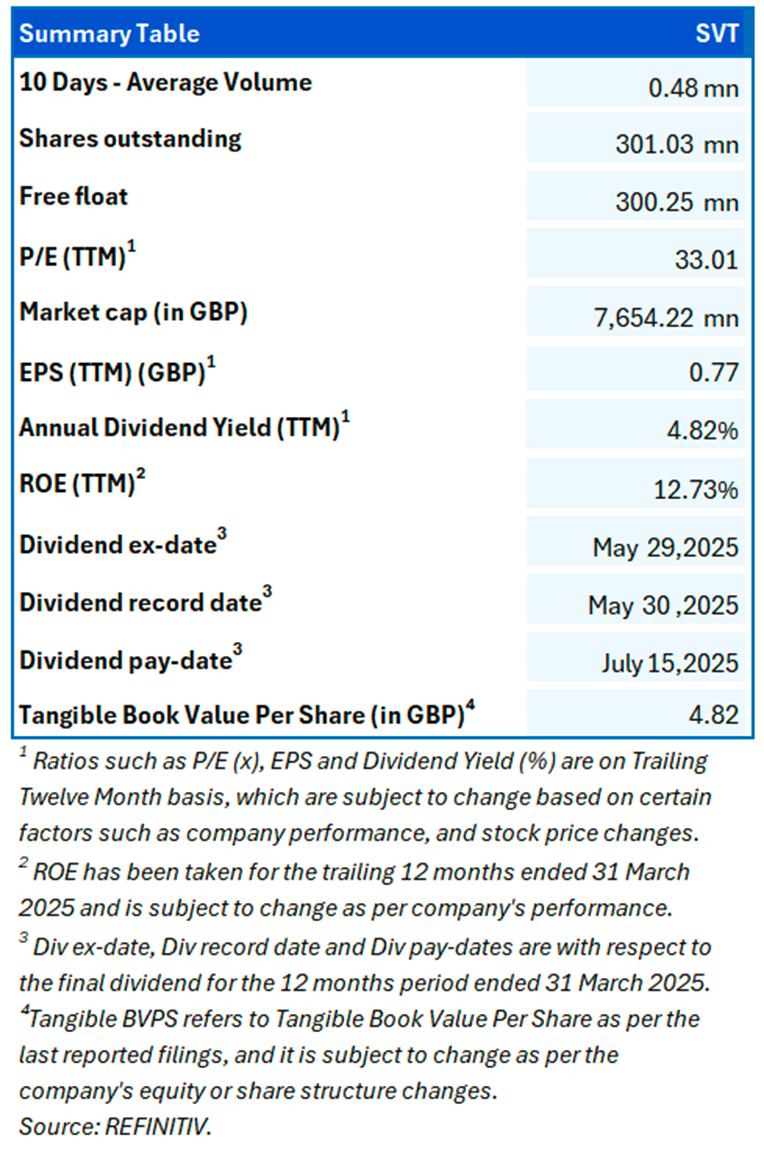

Severn Trent PLC (LSE: SVT)

Severn Trent PLC (LSE: SVT), a FTSE 100 listed company and United Kingdom-based holding company of Severn Trent Water Limited (STWL) and the ultimate holding company of Severn Trent Utilities Finance Plc (STUF). The Company provides water and wastewater services. The Company operates through two divisions: Regulated Water and Wastewater, and Severn Trent Business Services. Regulated Water and Wastewater division includes the wholesale water and wastewater activities of the Company’s regulated businesses, STWL and Hafren Dyfrdwy and its retail services to domestic customers. This Report covers the Investment Highlights, Conclusion, and Recommendation on the stock.

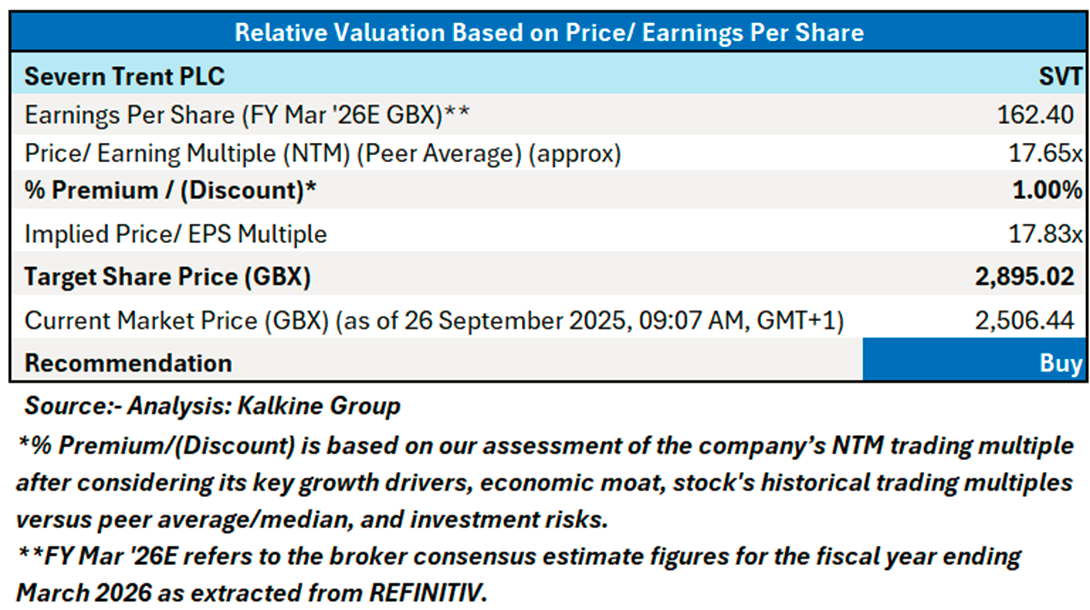

Key Investment Rationale – Buy at GBX 2,506.44

- Financial delivery and earnings momentum – Revenue increased 3.8% to £2,426.7m, while PBIT rose 15.3% to £590.2m as costs were managed and energy input prices eased. Net finance costs reduced 13.4% to £243.9m, supporting a 59% uplift in profit before tax to £320.1m. Adjusted basic EPS advanced 41.2% to 112.1p, and the total dividend moved up 4.2% to 121.71p, indicating room to keep capital investment elevated and still reward shareholders.

- Investment-led growth platform – Capital investment reached a record £1,673.5m (up 39.5%), including >£450m of AMP8 spend brought forward, taking the RCV to £13.7bn. This earlier deployment should help bring benefits forward (e.g., storm overflow upgrades) and, by increasing the asset base now, may support future allowed returns and earnings trajectory into AMP8.

- Balance sheet and cash cost discipline – Regulated gearing sits at 62.7% with credit ratings reaffirmed, and the effective interest cost eased to 4.3% (cash cost 3.4%). The combination of a stable funding profile, a higher capitalisation of interest from the enlarged programme, and energy hedging helped keep finance charges contained, which in turn supported EPS growth and a 4.2% dividend uplift.

- Multiyear outlook signals – Management guides to adjusted EPS doubling between 2025 and 2028, aided by regulated revenue growth (including ODIs), continued cost management and financing strategy. They also indicate £300m of net operational outperformance over five years (2027/28 prices) and target £1.7–£1.9bn capex next year, while environmental delivery remains visible (e.g., 912 GWh self-generation, frontier spills trajectory and interventions on 1,800 overflows), which may support both service metrics and future incentives.

SVT Daily Chart & Valuation

For conducting the valuation, the following peers have been considered: Telecom Plus PLC (LSE: TEP), National Grid PLC (LSE: NG.), etc.

As per the above-mentioned price action and technical indicators analysis, a ‘Buy’ rating has been given on Severn Trent PLC (LSE: SVT) at the Current Market Price of GBX 2,506.44, as of 26 September 2025, 09:07 AM, GMT+1.

Markets are trading in a highly volatile zone currently due to certain Macro & Micro-economic data and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is 26 September 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Note 6: Dividend Yield may vary as per the stock price movement.

Please wait processing your request...

Please wait processing your request...