Snowflake Inc

Snowflake Inc. (NYSE: SNOW) is a cloud-native data platform that enables enterprises to securely store, manage, and analyze large-scale data across multiple clouds, supporting advanced analytics, data sharing, and AI-driven workloads. The Company operates a usage-based, subscription model and serves a broad global customer base across industries, positioning itself as a core infrastructure layer for enterprise data and artificial intelligence strategies.

Key Business and Financial Updates:

- Robust Top-Line Expansion and Customer Momentum: Snowflake delivered a strong third quarter of fiscal 2026, reporting total revenue of USD 1.21 billion, up 29% year over year, with product revenue of USD 1.16 billion growing at the same pace. Customer engagement remained solid, reflected in a net revenue retention rate of 125%, alongside continued expansion among large enterprises, with 688 customers generating over USD 1 million in trailing 12-month product revenue and 766 Forbes Global 2000 customers.

- Strengthening Contract Visibility and Demand Backlog: Forward revenue visibility improved materially during the quarter, with remaining performance obligations (RPO) reaching USD 7.88 billion, representing 37% year-over-year growth. This increase highlights strong multi-year customer commitments and sustained demand for Snowflake’s AI Data Cloud platform across analytics, data sharing, and AI-driven workloads.

- Profitability Profile and Cash Flow Generation: On a GAAP basis, Snowflake recorded a product gross margin of 72% and an operating loss, reflecting continued investment in growth. However, non-GAAP results are underscored by improving operating leverage, with product gross margin expanding to 76% and non-GAAP operating income of USD 131.3 million, equivalent to an 11% margin. Cash generation remained healthy, with operating cash flow of USD 137.5 million and adjusted free cash flow of USD 136.4 million, demonstrating disciplined cost management alongside growth investments.

- AI-Led Platform Expansion and Strategic Positioning: Management emphasized accelerating adoption of Snowflake Intelligence, the Company’s enterprise AI agent, which achieved the fastest uptake in Snowflake’s history. Strategic partnerships with leading AI model providers, cloud platforms, and application ecosystems continue to enhance Snowflake’s position as a foundational layer for enterprise data and AI strategies, supporting deeper customer integration and long-term platform relevance.

- Outlook and Full-Year Trajectory: Looking ahead, Snowflake guided for fourth-quarter fiscal 2026 product revenue of USD 1.20 billion at the midpoint, implying 27% year-over-year growth, alongside positive non-GAAP operating margins. For the full fiscal year, management reaffirmed expectations for product revenue of approximately USD 4.45 billion, representing 28% growth, with product gross margin of around 75% and adjusted free cash flow margin near 25%, indicating continued confidence in durable growth, expanding profitability, and sustained cash generation.

Key Risks for Snowflake Inc. (NYSE: SNOW):

- Customer Consumption Sensitivity and Spend Optimization Risk: Snowflake’s usage-based revenue model exposes it to fluctuations in customer data-consumption patterns, where optimization efforts, cloud cost discipline, or macro-driven spending pullbacks by large enterprise customers could materially slow revenue growth and pressure net revenue retention.

- Intensifying Competitive and Platform Dependency Risk: The Company operates in a highly competitive cloud data and AI ecosystem against hyperscalers and well-capitalized peers offering vertically integrated or bundled analytics solutions; increased price competition or tighter integration by cloud providers could constrain Snowflake’s differentiation, pricing power, and long-term margin expansion.

- Execution Risk in AI Monetization and Product Innovation: Snowflake’s growth narrative increasingly depends on successful commercialization of AI-driven products and services; delays in customer adoption, slower-than-expected monetization, or higher R&D and infrastructure costs could dilute returns and weaken the expected payoff from elevated investment levels.

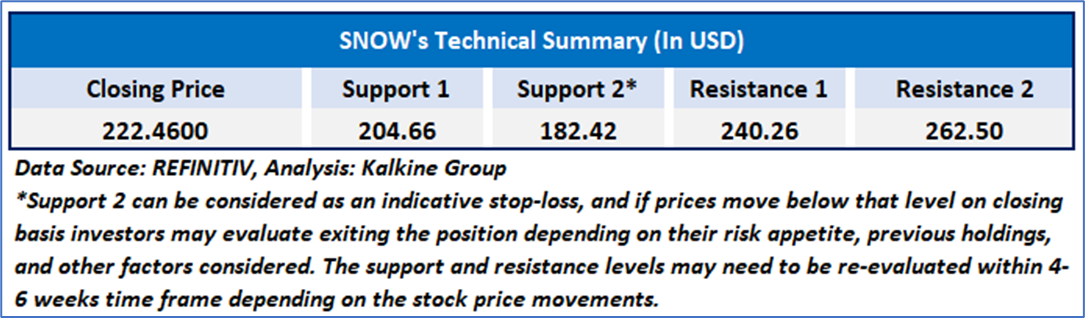

Technical Observation (on the daily chart):

- Trend Structure and Moving Averages: SNOW has shifted from a prior uptrend into a corrective phase, now trading below its 20-day and 50-day moving averages, which signals weakening short-term trend strength and rising overhead resistance.

- Momentum and Volume Signals: RSI near 39 indicates subdued momentum without extreme oversold conditions, while moderate volumes suggest controlled profit-taking rather than panic selling, but with limited evidence of strong dip-buying interest.

- Key Levels and Technical Bias: Support is seen around USD 215–220, with stronger support near USD 200, while resistance lies at USD 233–235 and USD 247–250; until these levels are reclaimed, the near-term outlook remains cautious and range-bound.

Snowflake Inc. (NYSE: SNOW) remains a strategically important cloud-native data and AI platform, delivering strong top-line growth, improving forward revenue visibility, and expanding enterprise adoption, as reflected in 29% year-over-year revenue growth in Q3 FY26, a net revenue retention rate of 125%, and remaining performance obligations of USD 7.88 billion (+37% YoY). While GAAP profitability remains constrained by continued investment in growth and innovation, non-GAAP margins and free cash flow generation highlight improving operating leverage and financial discipline. The Company’s accelerating AI-led product adoption and deepening ecosystem partnerships reinforce its long-term platform relevance; however, near-term performance remains sensitive to customer consumption patterns, competitive intensity within the cloud data ecosystem, and successful monetization of AI initiatives. Overall, Snowflake presents a balanced profile of durable growth opportunities underpinned by strong customer engagement, alongside execution and cyclicality considerations inherent in its usage-based model.

As per the above-mentioned price action, important support near USD 200- USD 220, momentum in the stock over the last month, and technical indicators analysis, a ‘WATCH’ rating has been given for Snowflake Inc. (NYSE: SNOW), at the closing price of USD 222.46 , as of December 19, 2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective, and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is December 19, 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Please wait processing your request...

Please wait processing your request...