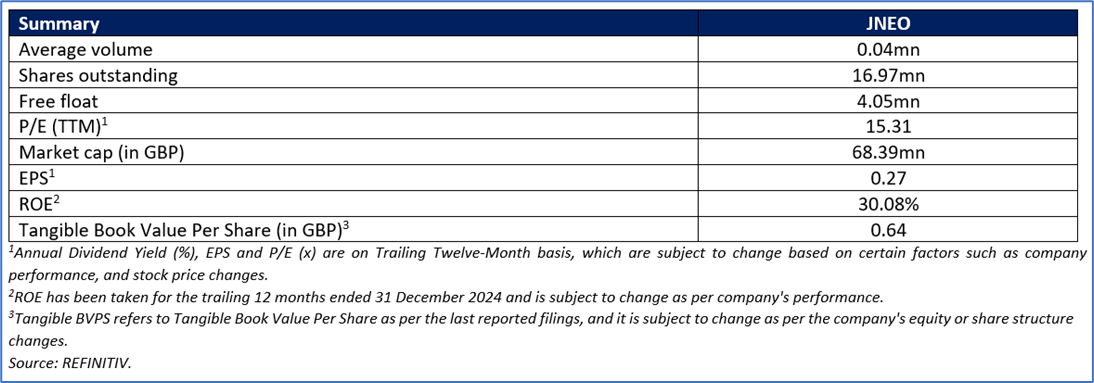

Journeo PLC

Journeo PLC (LSE: JNEO) is a company listed on the FTSE AIM All-Share Index, specializing in information systems and technical services for the transport sector. As a leading provider of intelligent transport systems (ITS), the company delivers innovative solutions for urban environments, airports, and public transport networks. Its core focus is on developing advanced infrastructure and operational technologies to enhance public transportation efficiency and connectivity.

Key Recommendation Rationale – Sell at GBX 430.00

- Resistance near Current levels: JNEO’s stock price breached the Resistance (R2) which was stated in the previous report on 19 August 2025 therefore, there could be a possibility that the stock might consolidate or decline from the current levels, considering overstretched valuation. Considering the market conditions and the price action, it is prudent to exit from the stock.

- Profit Stagnation Despite Operational Changes: Adjusted profit before tax remained flat at £2.8m compared to H1 2024. This stagnation occurs despite a notable shift in revenue composition, with higher growth in the Fleet division and a decline in Infotec. This could indicate that the newer or growing business segments are operating at lower margins than the legacy projects that have concluded, potentially pressuring overall profitability even as sales volumes increase in other areas.

- Decline in a Key Acquisition's Performance: The Infotec division, which was likely acquired to drive growth and geographic diversification, experienced a sharp 58% decrease in revenue (£8.5m to £3.6m). While this is explained by a specific contract ending, it raises questions about the division's ability to consistently secure new business of a similar scale to replace expired contracts and justify its acquisition cost, creating a lumpy revenue profile.

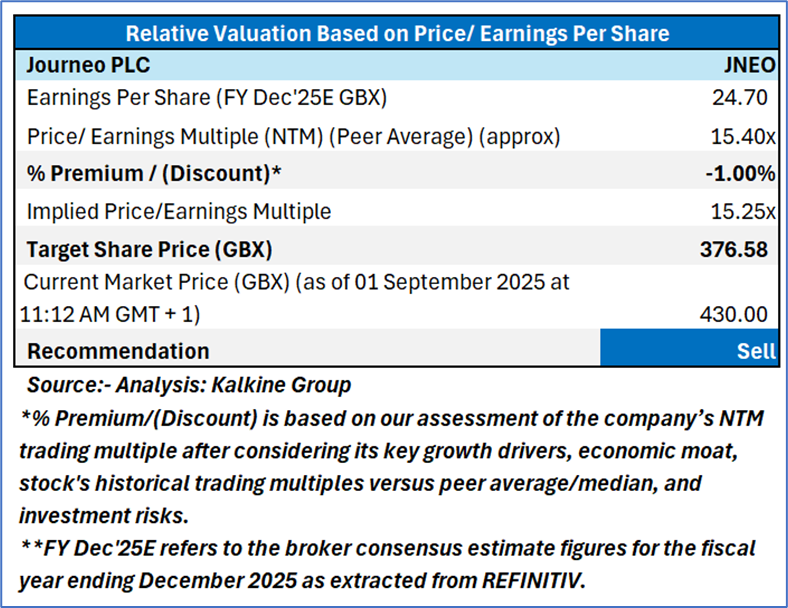

Valuation Methodology: Price/ Earnings Approach

Share Price Chart

One-Year Technical Price Chart (as of September 01, 2025). Source: REFINITIV, Analysis: Kalkine Group

Conclusion

The observed profit stagnation, occurring alongside a notable shift in revenue streams, suggests that growth within the Fleet division may be occurring at a lower margin profile than the legacy projects it is effectively replacing. This dynamic exerts pressure on overall profitability, as increased sales volume does not currently translate into enhanced bottom-line results. Concurrently, the significant revenue contraction within the Infotec division highlights a dependency on large-scale, non-recurring contracts. This reliance introduces volatility to the revenue base and presents a challenge for maintaining consistent period-on-period performance, which is relevant for evaluating the strategic return on the acquisition investment.

For conducting the valuation, the following peers have been considered: Dowlais Group PLC (LSE: DWL), Transense Technologies PLC (LSE: TRT), etc

Given its current trading levels, the recent strategic investments and partnerships, relative valuation, and associated risks, it is prudent to exit the stock at the current levels.

Hence, a ‘Sell’ recommendation is given on the stock at the Current Market Price of GBX 430.00 as of 01 September 2025 at 11:12 AM GMT +1.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is 01 September 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Please wait processing your request...

Please wait processing your request...