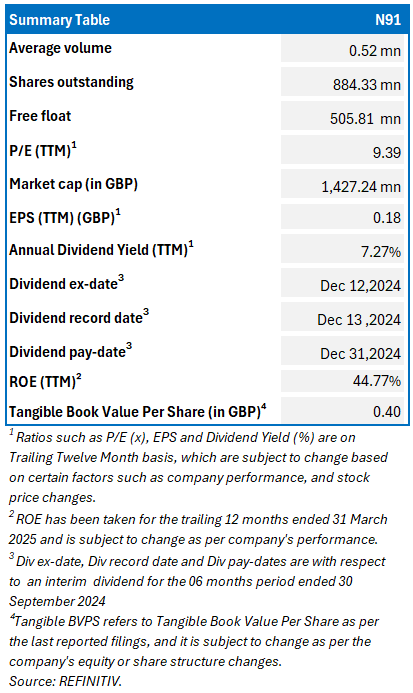

Ninety One PLC

Ninety One PLC (LSE: N91) is an FTSE 250 index-listed, headquartered in the United Kingdom, functions as an investment management firm. It provides a variety of active investment strategies spanning equities, fixed income, multi-asset, and alternative assets. The company serves its clients through five regional divisions: the United Kingdom, Africa, Europe, the Americas, and the Asia Pacific). This Report covers the Investment Highlights, Conclusion, and Recommendation on the stock.

Key Recommendation Rationale – Sell at GBX 162.20

- Resistance near Current levels: N91’s stock price crossed the Resistance (R1) which was stated in the previous report on 01 April 2025 therefore, there can be a possibility of a decline in resistance levels. Considering the market conditions and the price action, it is prudent to exit the stock.

- Net Outflows Remained Despite H2 Recovery: The firm experienced full-year net outflows of £ (4.9) billion (FY25), following £(9.4) billion in FY2024. Although H2 saw modest inflows of £0.4 billion, the persistence of outflows—particularly in equities and fixed income—indicates continued investor caution or rotation away from certain strategies.

- Decline in Profitability Metrics: Adjusted operating profit fell by 1% YoY to £187.9 million (FY25), and the adjusted operating profit margin contracted from 32.0% to 31.2%, reflecting a slightly higher cost base and subdued topline leverage. This decline suggests pressures on operational efficiency during the year.

- Continued Outflows from Key Regions and Channels: The UK market saw net outflows of £ (3.9) billion, and the advisor channel experienced £ (3.1) billion in net redemptions during the reported period (FY25). These figures indicate persistent challenges in key client segments and regions, particularly in relation to portfolio reallocations and subdued investor sentiment

- Macroeconomic Risk: The market sentiments can remain weak in the short term due to the subdued consumer disposable income, geopolitical tensions, and political risks.

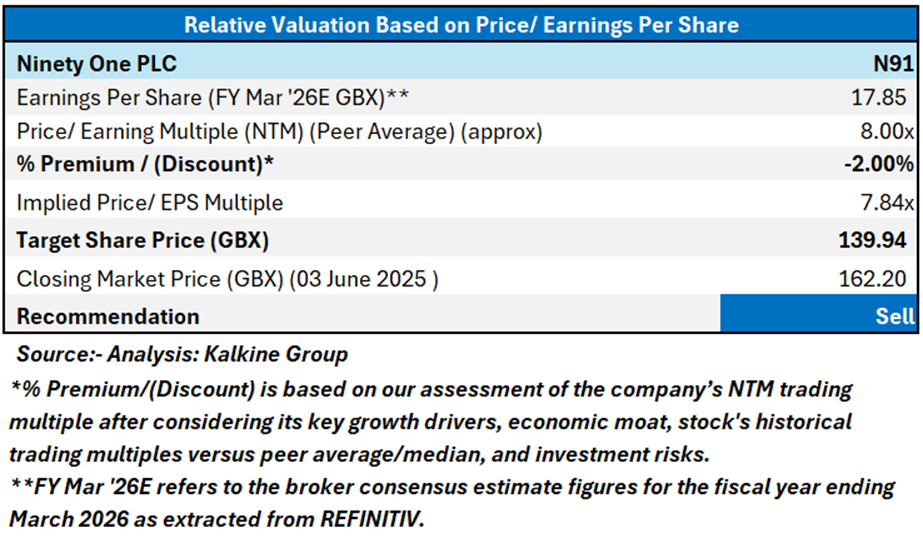

Valuation Methodology: Price/ Earnings Approach

Share Price Chart

Conclusion

Ninety One (N91) may continue to trade at a discount, weighed down by several challenges across FY25 including persistent net outflows—£ (4.9) billion for the year despite a recovery in H2, following £ (9.4) billion in FY2024. Profitability metrics also weakened, with adjusted EPS down 3% YoY to 15.5p and basic EPS falling 7% to 17.2p. Additionally, the firm faced ongoing outflows across key regions and distribution channels. Additionally, tariff disputes, escalating geopolitical tensions, renewed conflict from the Russia-Ukraine war, elevated interest rates, and persistent inflation are expected to weigh on profitability. For conducting the valuation, the following peers have been considered: Man Group PLC (LSE: EMG), Investec PLC (LSE: INVP), etc.

Given its current trading levels, the recent financial performance, strategic investments and partnerships, market expansion and cost optimization strategies, relative valuation, and associated risks, it is prudent to exit the stock at the current levels. Hence, a ‘Sell’ recommendation is given on the stock at the Closing Market Price of GBX 162.20 as of 03 June 2025.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is 03 June 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Note 6: Dividend Yield may vary as per the stock price movement.

Please wait processing your request...

Please wait processing your request...