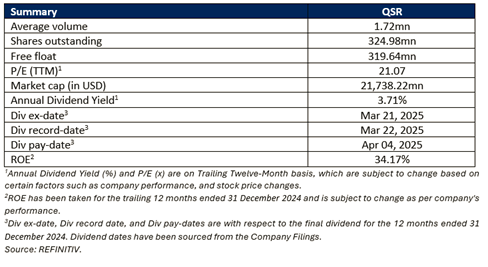

Restaurant Brands International Inc

Restaurant Brands International Inc (NYSE: QSR) is a fast-food restaurant company that owns and franchises quick-service dining establishments. It specializes in serving coffee, beverages, and a variety of food items. The company operates through several segments, including Tim Hortons (TH), Burger King (BK), Popeyes Louisiana Kitchen (PLK), Firehouse Subs (FHS), International (INTL), and Restaurant Holdings.

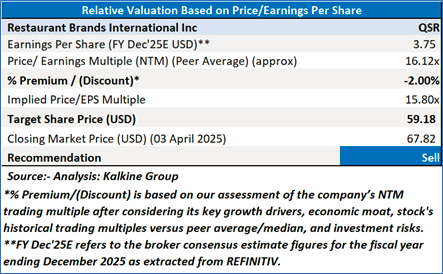

Recommendation Rationale – SELL at USD 67.82

- Challenges in System-wide Sales Growth: QSR 's system-wide sales growth was relatively modest across multiple segments in the fourth quarter and full year of 2024. Although some brands, such as Tim Hortons and Popeyes, saw slight improvements, others like Burger King and Firehouse Subs struggled. Burger King reported significantly lower growth compared to previous years, especially in the U.S., where comparable sales growth was sluggish. Additionally, the overall system-wide sales growth for Burger King, Popeyes, and Firehouse Subs were below expectations, signaling that these brands may face difficulty in maintaining momentum in the near future.

- Negative Impact of FX Movements: Throughout 2024, QSR faced unfavorable foreign exchange (FX) movements that impacted its financial results. Total Revenues and Adjusted Operating Income for the full year and fourth quarter were adversely affected, despite growth in local currencies. When excluding the FX impact, QSR 's total revenues and operating income showed only marginal improvements, indicating that the company’s performance was heavily influenced by currency fluctuations. This suggests that the company's international business might continue facing volatility due to exchange rate risks.

- Increased Operating Expenses in Certain Segments: The company experienced higher operating costs in several segments, especially in Burger King and Popeyes. The increase in Segment F&P (Franchise and Property) Expenses and higher advertising costs placed pressure on profit margins, particularly for Burger King. Additionally, the International segment saw a rise in Segment G&A (General & Administrative) expenses, mainly due to higher compensation-related costs. While some of these increases were attributed to business investments and acquisitions, the rising costs could limit profitability in the future if revenue growth does not outpace these expenses.

- Disappointing Performance in the RH Segment: The Restaurant Holdings (RH) segment, which includes the recently acquired Carrols Burger King and Popeyes China restaurants, posted weak results. For the full year and fourth quarter, RH experienced negative system-wide sales growth, reflecting operational challenges and ongoing restaurant remodels. The underperformance was compounded by temporary restaurant closures, which further impacted overall revenue. Although QSR has been optimistic about its plans to refranchise and find a new partner for PLK China, the segment's lackluster financial results may raise concerns about the integration of newly acquired entities.

- Slowing Growth Amid Strategic Changes: Despite QSR 's long-term goals of system-wide sales growth and net restaurant expansion, some brands are experiencing slower growth and operational hurdles. The Burger King U.S. segment is attempting to rejuvenate its performance with the "Reclaim the Flame" initiative, but these investments may take time to yield results. The slowdown in restaurant count growth, particularly for Burger King and Firehouse Subs, raises questions about the company’s ability to sustain its growth targets. Additionally, the shift toward refranchising and potential restructuring in markets like China may lead to further uncertainty in future growth projections.

QSR’s Daily Price Chart

Valuation Methodology: Price/Earnings Approach

QSR faced multiple challenges in 2024, with sluggish system-wide sales growth across key brands, particularly Burger King and Firehouse Subs. Adverse foreign exchange movements further weakened financial results, while rising operating expenses, especially in advertising and G&A costs, pressured profitability. The Restaurant Holdings segment underperformed, with Carrols Burger King and Popeyes China struggling due to operational disruptions. Strategic initiatives, like Burger King’s "Reclaim the Flame," have yet to show meaningful impact, and slowing restaurant growth raises concerns about QSR’s long-term expansion strategy. Persistent headwinds suggest ongoing difficulties in maintaining momentum and profitability.

Given its current trading levels, downside indicated by valuation, and risks associated, it is prudent to book profit at the current levels. Hence, a ‘Sell’ recommendation is given on the stock at the closing price of USD 67.82, as of April 03,2025.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical issues prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is neither an indicator nor a guarantee of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is April 03,2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Please wait processing your request...

Please wait processing your request...