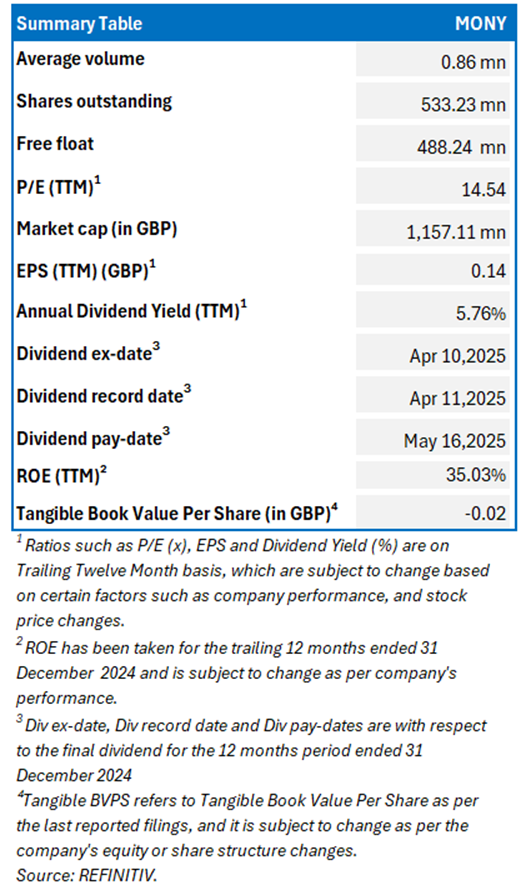

Mony Group PLC

Mony Group PLC (LSE: MONY) is a UK-based company listed at the FTSE 250. It runs a technology-driven platform designed to help households save money. The company provides various consumer finance brands through its innovative, tech-focused platform. This Report covers the Investment Highlights, Conclusion, and Recommendation on the stock.

Key Recommendation Rationale – Sell at GBX 217.00

- Resistance near Current levels: MONY’s stock price crossed the Resistance (R2) which was stated in the previous report on 14 April 2025 therefore, there can be a possibility of a decline in resistance levels. Considering the market conditions and the price action, it is prudent to exit the stock.

- Declining Segment Revenues in Money, Home Services, and Travel: The Money segment declined by 2% to £97.8mn, Home Services dropped 7% to £36.1mn, and Travel fell 5% to £19.6mn in FY24. These declines suggest reduced demand across key categories and a challenging competitive environment, particularly in broadband, mobile, and travel verticals.

- Drop in Active Users Raises Engagement Concerns: Active users across MSM and Quidco decreased from 14.2 million in FY23 to 13.8 million in FY24. This decline, despite increased investment in member-based propositions and app features, indicates pressure in maintaining user growth and engagement levels.

- Rising Pay-Per-Click (PPC) Costs Add to Margin Pressure: PPC costs rose by 19% in H2 compared to H1 2024, highlighting increasing reliance on paid channels for customer acquisition. Although offset by growth in SuperSaveClub membership, this trend poses a risk to future marketing efficiency and profitability if not controlled.

- Macroeconomic Risk: The market sentiments can remain weak in the short term due to the subdued consumer disposable income, geopolitical tensions, and political risks.

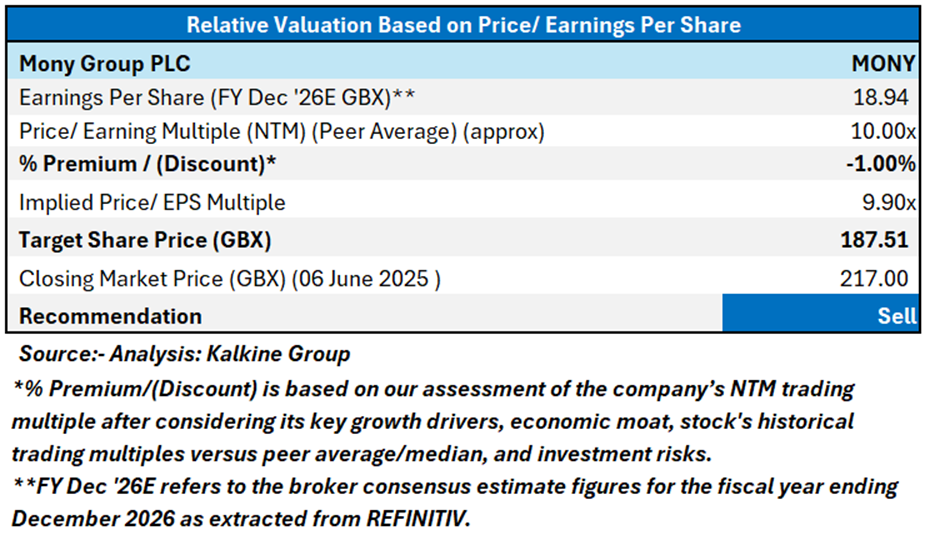

Valuation Methodology: Price/ Earnings Approach

Share Price Chart

Conclusion

MONY may remain under pressure and trade at a discount, reflecting multiple headwinds in FY24: flat Q4 revenue signals a weak close to the year, with segment declines in Money, Home Services, and Travel. A reduction in active users raises concerns around engagement, while a 19% increase in H2 Pay-Per-Click (PPC) costs versus H1 further strained margins. Additionally, tariff disputes, escalating geopolitical tensions, renewed conflict from the Russia-Ukraine war, elevated interest rates, and persistent inflation are expected to weigh on profitability. For conducting the valuation, the following peers have been considered: Future PLC (LSE: FUTR), Reach PLC (LSE: RCH), etc.

Given its current trading levels, the recent financial performance, strategic investments and partnerships, market expansion and cost optimization strategies, relative valuation, and associated risks, it is prudent to exit the stock at the current levels. Hence, a ‘Sell’ recommendation is given on the stock at the Closing Market Price of GBX 217.00 as of 06 June 2025.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is 06 June 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Note 6: Dividend Yield may vary as per the stock price movement.

Please wait processing your request...

Please wait processing your request...