_01_29_2026_04_52_29_356102.jpg)

Is Bunzl stock undervalued in 2026? We analyse BNZL’s dividend, margins, acquisitions, and long-term outlook for UK investors

As the FTSE 100 enters uncharted territory in 2026, breaching the historic 10,000-point milestone, savvy retail investors are frantically scouring the UK stock market for undervalued blue-chip stocks that can offer both dividend growth and capital appreciation. One name dominating the investment news and financial social media is Bunzl PLC (BNZL). Known as a powerhouse in the support services sector, Bunzl has long been a staple for income investors due to its status as a Dividend Aristocrat. However, with the UK economy facing "anaemic" growth and global market dynamics shifting due to US trade tariffs and inflationary pressures, many are asking: is Bunzl’s 30% decline in 2025 a massive buying opportunity or a warning of a structural margin downcycle?

In this deep-dive equity analysis, we peel back the layers of the Bunzl business model to determine if this multinational distributor can navigate the macroeconomic volatility of 2026. With the British Pound (GBP) trading defensively and the Bank of England weighing further interest rate cuts, the stakes for UK equities have never been higher. We explore the latest financial results, acquisition strategy, and operational updates to see if Bunzl’s aggressive move into Slovakia and its recovery in North America can flip the script. From SWOT analysis to forward-looking strategies, this is the ultimate guide for anyone looking to optimize their ISA portfolio or SIPP with high-yield FTSE stocks in a "Goldilocks" or "Gloom" scenario.

The Support Services industry is currently at a crossroads. While heavyweights like Rolls-Royce and BAE Systems have led the FTSE 100 rally, the more defensive, "boring" companies like Bunzl have lagged behind. But as global investors look to diversify away from US mega-cap concentration, high-quality mid-cap and large-cap UK stocks are seeing a massive valuation re-rating. Is Bunzl’s current P/E ratio of 14.1 too cheap to ignore, or does the 2026 margin warning justify the sell-off? Let’s break down the short-term, medium-term, and long-term outlook for one of the London Stock Exchange’s most resilient players.

Source: Kalkine Group

What Is the Current State of the Global Market and the UK Economy?

The global landscape in January 2026 is defined by a paradoxical "high-altitude" stock market and "low-altitude" economic growth. While the FTSE 100 has hit record highs above 10,000, the underlying UK economy remains fragile.

- UK Macro Dynamics: GDP growth for 2026 is forecast to be sluggish at best, hampered by a high tax burden and a loosening labor market. The Bank of England is expected to cut rates only twice this year, reaching a "neutral" rate of around 3.25% by Autumn.

- FTSE 100 vs. FTSE 250: The blue-chip index has been carried by mining and defense, while the FTSE 250 is widely considered the "cheapest in 23 years" relative to its history, trading at a significant discount.

- GBP Analysis: Sterling is trading defensively. Any internal political challenges to the UK leadership or further economic softening could trigger a sell-off in the GBP/USD pair, which ironically helps Bunzl since 80% of its revenue is generated outside the UK.

How is Bunzl Performing and What is Its Business Model?

Bunzl is a "silent giant" of the global supply chain. It doesn't manufacture; it sources, consolidates, and delivers essential items—everything from food packaging and cleaning supplies to PPE and surgical gloves.

- Current Performance: The stock is currently trading around 2,052p, significantly down from its 52-week high of 3,488p.

- Latest Financials: According to the December 2025 Pre-Close Statement, Bunzl expects 2025 revenues to be broadly flat. The operating profit margin is pegged at 7.6%, but the company issued a "disappointing" warning that the 2026 margin might be slightly down due to cost inflation and lack of product price inflation (Source: Bunzl Investor Relations/RNS).

- Dividend & Buybacks: Bunzl paid an interim dividend of 20.2p on January 5, 2026. While the £200 million share buyback for 2025 is complete, management has been cautious about starting a new one, keeping leverage at roughly 2.0x (Source: Bunzl Annual Report/Interim Updates).

What is the Short, Medium, and Long-Term Sector Outlook?

- Short Term (3-6 Months): Neutral to Bearish. The market is still digesting the margin warning. Until the full-year results on March 2, 2026, provide more clarity on North American recovery, the stock may remain range-bound.

- Medium Term (1-2 Years): Bullish. The "Support Services" sector is expected to benefit from a "margin recovery cycle" as inflation cools and acquisitions like Nisbets and the new Slovakian firm Damito begin to contribute synergies.

- Long Term (3+ Years): Strongly Bullish. Bunzl's compounding model is world-class. Having completed over 220 acquisitions since 2004, their ability to consolidate fragmented markets remains an unmatched competitive advantage.

What Forward-Looking Strategies Should Investors Consider?

Investors must think logically about the drivers of "boring but beautiful" stocks like Bunzl.

- Short-Term Strategy (The "Wait and See"): Focus on the March earnings call. Key metrics to watch are "New Business Wins in North America." If management confirms that the US decline has bottomed out, the stock could see a sharp "mean reversion" rally.

- Medium-Term Strategy (The "Dividend Reinvestment"): With a 3.6% yield and 30+ years of consecutive increases, using a DRIP (Dividend Reinvestment Plan) during this period of price weakness allows investors to accumulate more shares at a discount.

- Long-Term Strategy (The "Consolidation Play"): View Bunzl as a "private equity fund in public clothes." They buy small businesses at low multiples and fold them into a global giant. This strategy works best over decades, not months.

Is Bunzl Bullish, Bearish, or Neutral?

- Short-Term Reasoning (Bearish/Neutral): The technicals look heavy. The 50-day moving average is below the 200-day, and the MACD is signaling a bearish trend. Retail sentiment is currently low because the stock "missed" the 10,000-point FTSE party.

- Long-Term Reasoning (Bullish): The fundamentals tell a different story. A P/E ratio of 14 for a global leader with an "A" grade credit profile is rare. The logic is simple: the world always needs toilet paper, food containers, and safety vests. Bunzl provides these more efficiently than anyone else.

Latest Drivers of the Stock: Why the Surge or Dip?

- The Dip: Driven by "margin contraction" fears. Analysts expected a 0.1% increase in margin for 2026, but Bunzl guided for a slight decrease. Increased UK staff taxes (National Insurance) also added to the cost base.

- The Potential Surge: The recent acquisition of Damito s.r.o in Slovakia marks an expansion into Central Europe. Furthermore, a "Goldilocks" easing of rates by the Fed and BoE would lower the cost of debt for Bunzl’s future M&A pipeline.

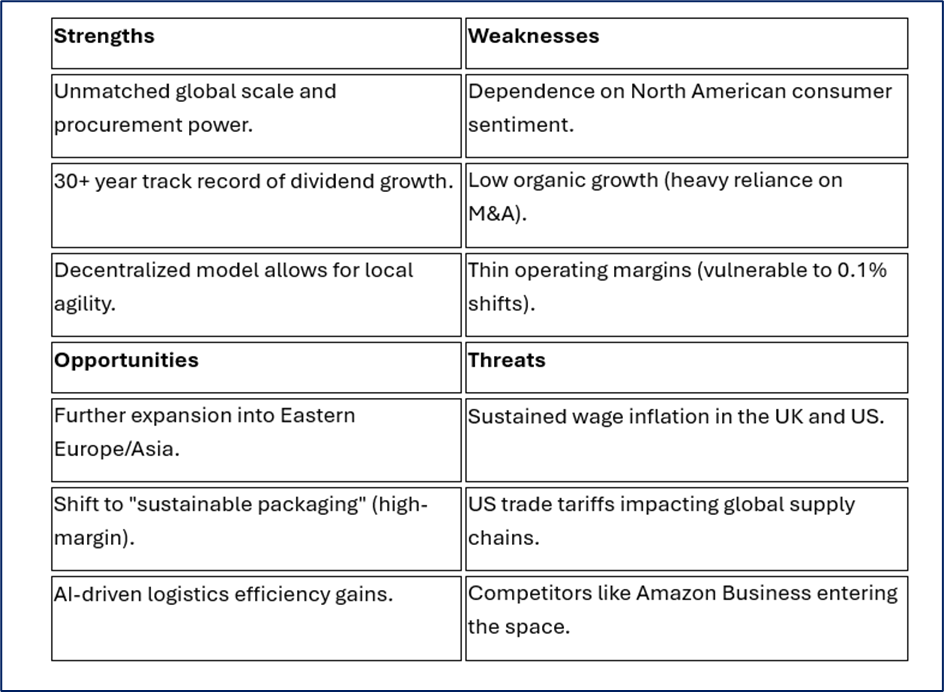

SWOT Analysis: The Brutal Truth About Bunzl

Source: Kalkine Group

Key Risks Every Investor Must Know

- US Labor Market Softening: Since North America is the biggest market, any spike in US unemployment directly hits the foodservice and retail supply divisions.

- Currency Headwinds: A sudden strengthening of the GBP would devalue overseas profits when converted back to Sterling.

- Acquisition Timing: If Bunzl pays too much for "bolt-on" companies in a high-interest-rate environment, it could erode shareholder value.

Analytical Investment Conclusion: Buy, Sell, or Hold?

Conclusion: HOLD / ACCUMULATE ON DIPS

Bunzl isn't a "get rich quick" stock; it’s a "stay rich" stock. While the short-term margin headwinds are real and may lead to further price volatility, the company remains a cash-generating machine. For retail investors, the current valuation represents a "valuation gap" compared to the broader FTSE 100. If you are looking for safety, income, and a proven management team, this is a high-conviction hold. If the price drops below 2,000p, it moves into "Strong Buy" territory for long-term value seekers.

Please wait processing your request...

Please wait processing your request...