While the broader market remains in a quiet "Santa Rally" lull, Entain PLC (LSE: ENT) is bucking the trend. On December 29, 2025, the FTSE 100 gambling giant saw its shares climb approximately 2%, a notable move for a stock that has spent much of the year navigating regulatory storms and boardroom shifts.

But what is driving this late-December rally? From a de-risked UK tax outlook to the "BetMGM Goldmine," we break down the latest updates on this global gaming titan.

Key Reasons & Drivers: Why the Stock is Up Today

The ~2% jump on December 29th is largely attributed to a "relief rally" and positive year-end sentiment:

Source: Kalkine Group

- De-Risking the UK Budget: Following the November 2024/2025 tax hikes, Entain has successfully quantified the impact (est. £200m annual cost). Investors are now buying back in, realizing that the worst-case "tax armageddon" scenarios are already baked into the price.

- JPMorgan’s Overweight Upgrade: Recent bullishness stems from a late-year upgrade by JPMorgan, which highlighted Entain's "resilient momentum" and attractive valuation at roughly 6.3x forward EBITDA.

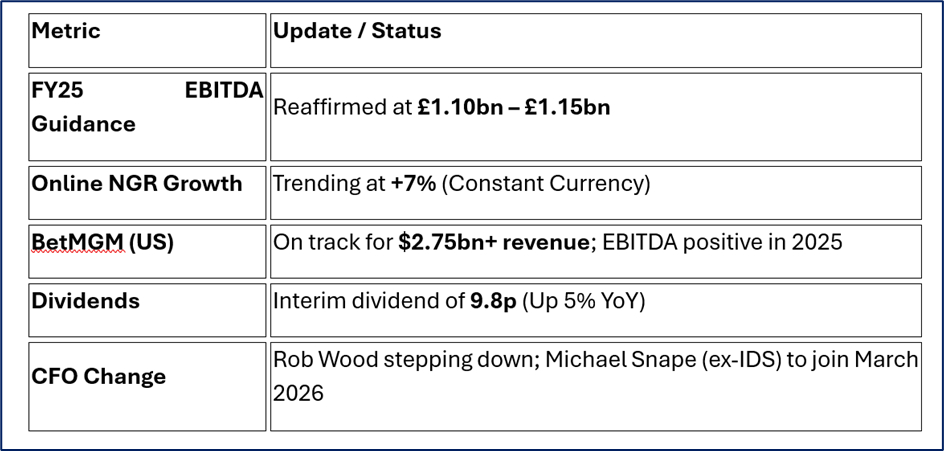

- BetMGM Cash Distribution: For the first time, the US joint venture BetMGM is set to return significant cash—at least $200m—to its parents (Entain and MGM Resorts). This transition from a "money pit" to a "cash cow" is a massive psychological shift for shareholders.

- Operational Stability: Recent trading updates confirmed that performance remains in line with the upgraded FY25 EBITDA guidance of £1.1bn to £1.15bn.

Latest Business Model: The "Podium" Strategy

Entain has pivoted from aggressive, broad-scale M&A to a more disciplined "Quality over Quantity" model.

- Regulated Focus: The group now operates almost exclusively in domestically regulated markets (30+ territories).

- Proprietary Tech: Unlike many peers, Entain owns its entire tech stack. This allows for faster product localization (like the recent Angstrom integration for better US sports pricing).

- The Hybrid Channel: Entain maintains a massive retail footprint (Ladbrokes/Coral) which acts as a low-cost customer acquisition funnel for its high-margin online platforms.

Financial & Operational Updates (Late 2025)

Source: Company Data

SWOT Analysis: A Reality Check

Source: Kalkine Group

Strengths

- Market Dominance: "Podium" positions in the UK, Italy, and Australia.

- BetMGM Partnership: A 50% stake in a top-3 US operator.

- Vertically Integrated: Owning the tech means higher margins and better data control.

Weaknesses

- High Debt Load: Adjusted net debt remains high at over £3.3bn, though leverage is trending down toward 3.5x.

- Management Turnover: Multiple CEO and CFO changes in recent years have caused investor jitters.

Opportunities

- Brazil Regulation: The newly regulated Brazilian market saw Entain grow NGR by 21% recently.

- Project Romer: An efficiency program targeting £100m in annual savings by 2026.

- Cash Flow: Aiming for £0.5bn+ in annual adjusted cash flow by 2028.

Threats

- Regulatory Creep: Potential for further stake limits or affordability checks in the UK and EU.

- Adverse Sports Results: High-payout months (e.g., September 2025) can wipe millions off the bottom line.

- Currency Volatility: Exposure to fluctuations in the Euro and Australian Dollar.

Key Risks to Watch

- Transition Risk: While Michael Snape is a seasoned CFO, the handover in early 2026 must be seamless to maintain market confidence.

- Macro Pressures: If consumer spending in the UK and Italy dips in Q1 2026, the high-frequency gaming spend is usually the first to be cut.

- US Competition: FanDuel and DraftKings continue to spend heavily; BetMGM must maintain its 14% market share without sacrificing profitability.

Conclusion

Entain is finishing 2025 on a stronger footing than many expected. By quantifying the UK tax impact and turning the corner with BetMGM's profitability, the company has cleared several major hurdles. The 2% rise today suggests that the "valuation gap" between Entain and its US-listed peers may finally be starting to close.

Please wait processing your request...

Please wait processing your request...