Global Markets 2026 Outlook Snapshot

- AI is the new macro engine: Corporate AI capex is set to exceed $500B+ in 2026, driving more US GDP growth than households — a historic shift.

- Global fragmentation - new spending boom in defense, energy grids, robotics, and industrial reshoring.

- Inflation is becoming structural, not cyclical — powered by AI energy demand, commodity scarcity, and supply chain reconstruction.

- Asia is the global tech powerhouse (Taiwan, Korea, Japan, China) while Europe benefits from massive fiscal industrial support.

- UK sectors poised for structural tailwinds: Utilities, defense, energy services, data-centre real estate, industrial automation, and selective high-quality financials.

- Risks: Policy misalignment (too many Fed cuts priced in), valuation stretch, global government debt >$100T, bond-market volatility.

- Portfolio theme for 2026: AI infrastructure + quality credit + Asia tech + commodities + alternatives + selective EM.

1. The New Policy Nexus: Rate Cuts Meet Fiscal Firepower

A Post-Cyclical Cocktail Supercharging Asset Prices

2026 opens with an economic anomaly: large deficits + moderating inflation + rate cuts — outside recession.

- US: Tax rebates from the “One Big Beautiful Bill” add fuel to an already booming wealth effect from stocks & housing.

- Europe: Germany’s sweeping fiscal push (defence, industrial subsidies, infrastructure) aligns EU policy with global industrial nationalism.

- UK: Faces a fiscal squeeze (≈1% of GDP) but this stability opens space for the BoE to cut rates toward ~3%.

Source: Kalkine Group

This mix shifts markets away from “macro fear trades” toward AI-led earnings, data-center capex, and regional divergences.

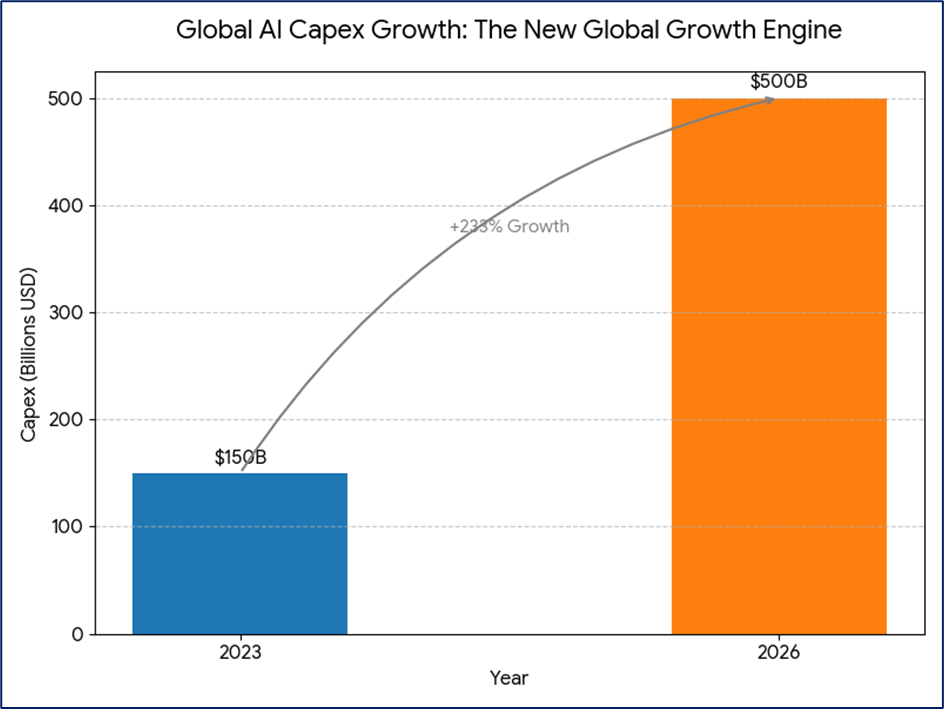

II. AI Super-Cycle: The Biggest Productivity Shock Since the Internet

AI Capex Has Become the New Global Growth Engine

Mega-cap US tech firms are entering a hyper-investment cycle:

- 2023: ~$150B

- 2026: $500B+ global AI capex

- This is now a GDP driver on par with past consumer booms.

Data Source: Global Reports

Why This Time AI = Structural (Not a Bubble)

- Record profits across US mega-cap tech

- Rapid diffusion across services, manufacturing, finance, and healthcare

- OECD estimates 1–2.5% productivity gains over the decade

- Asia dominating the semiconductor backbone (Taiwan, Korea, Japan)

The Three Layers of AI Value Creation

- Enablers – chips, power grids, cooling systems, data centers

- Intelligence – proprietary models, cybersecurity, data management

- Applications – robotics, fintech, cloud, healthcare automation

The investment implications are now moving beyond Big Tech.

III. Physical AI: Energy, Metals & Infrastructure Become the New Growth Sectors

AI is hitting a physical bottleneck:

- Data centers need 10–30x more power

- Grid investment is lagging

- Copper, lithium, uranium and rare metals remain in structural deficit

Result:

Utilities, Industrials, Energy Services, and Grid Infrastructure become high-growth sectors, not defensive plodders.

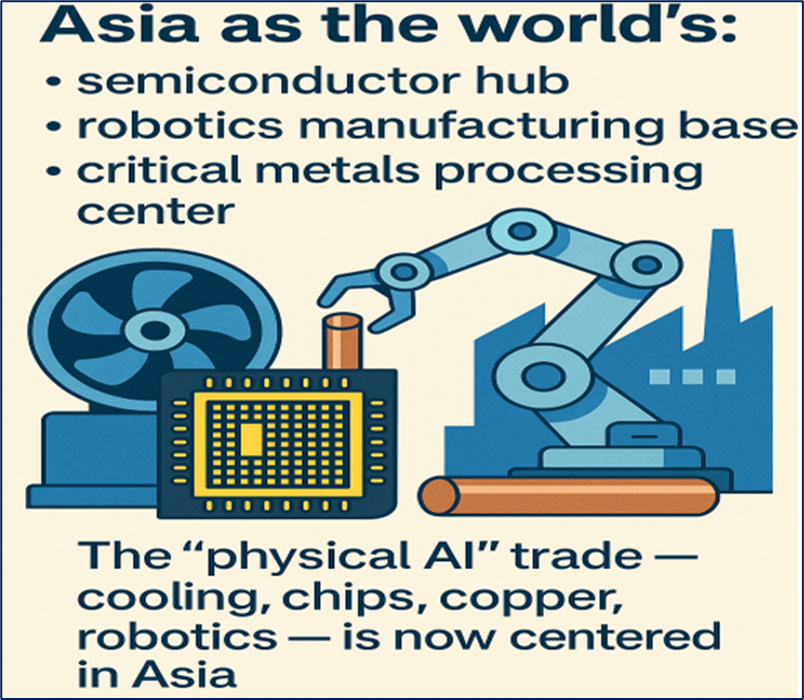

Asia Takes the Lead

BNP Paribas and UBS point to Asia as the world’s:

- semiconductor hub

- robotics manufacturing base

- critical metals processing center

The “physical AI” trade — cooling, chips, copper, robotics — is now centered in Asia.

Source: Kalkine Group

IV. The Fragmentation Dividend: Geopolitics Is Now an Investment Theme

Strategic Rivalry = Big, Durable Spending Cycles

De-globalization is creating multi-year investment booms in:

- defense & military technology

- energy security

- industrial reshoring

- semiconductor independence

- critical minerals

These are not cyclical — they are government-backed and sticky.

The New Inflation Regime: Scarcity Everywhere

The world has entered:

- energy scarcity

- metal scarcity

- labour scarcity

- political scarcity (instability risk premium)

This makes the 2020–2023 inflation spike structural, not a one-off.

Result: commodities remain a core hedge; bonds lose diversification power.

V. Global Equity Architecture: Leadership, Dispersion & Rotations

US: Exceptionalism Still Intact

2026 S&P 500 targets converge at:

7,400 – 7,800, driven by AI-led earnings (13–15% required).

- Morgan Stanley: 7,800

- JPMorgan: 7,500 (up to 8,000 if Fed cuts more)

- Goldman Sachs: 7,400–7,600

- Bank of America: 7,100 (more energy + defence biased)

But the Rally MUST Broaden or It Breaks

Consensus: US mega-cap concentration risk is too high.

Rotation themes for 2026:

- Financials (valuation reset, balance-sheet resilience)

- Industrials & Utilities (AI power demand)

- Small & Mid-Caps (Goldman, BNP)

Asia = The 2026 High-Conviction Region

Drivers:

- Semiconductor dominance

- Governance reforms (Japan/Korea)

- China’s renewed tech stimulus

- EM benefiting from easing and strong real yields

Asia tech is the structural winner across all institutional reports.

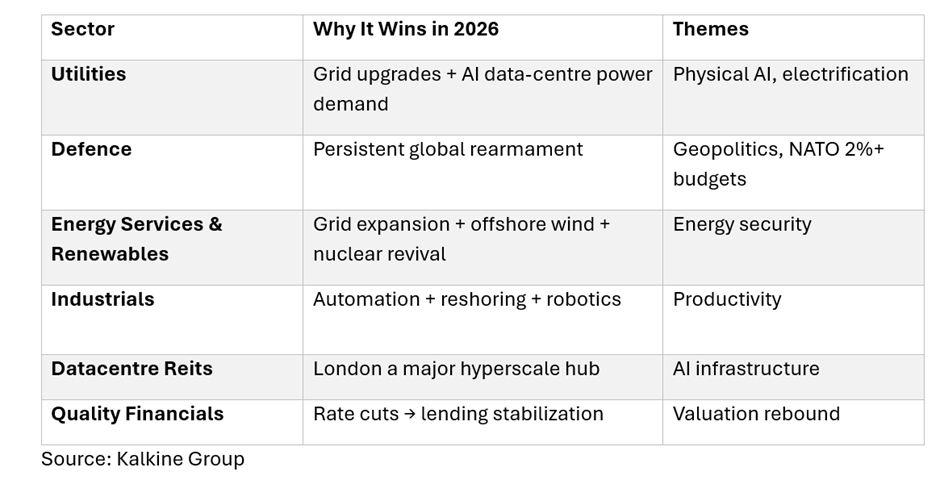

VI. UK 2026: Sectors & Stocks Positioned for Structural Tailwinds

Despite sub-1% growth expectations, the UK market is value-rich and linked to global (not domestic) cycles.

UK Sectors Poised to Benefit

Illustrative UK-Listed Names

- Utilities / Power Infrastructure: National Grid, SSE

- Defense & Security: BAE Systems, QinetiQ

- Energy & Renewables: BP (transition capex), Shell (LNG), Drax (bioenergy/BECCS)

- Industrial Automation: Melrose, IMI, Spirax-Sarco

- Data Infrastructure: Digital 9 Infrastructure (selectively), Greencoat UK Wind

- Banks / Insurers: HSBC, Barclays, Prudential

These align structurally with AI-energy demand, grid reinforcement, global defence capex, and capital-intensive resilience.

VII. Portfolio Resilience & Risk Management

Quality Is King

- Favourable IG credit

- Selective EM local currency (high real yields + USD moderation theme)

- Unfavourable HY due to refinancing risk

Alternatives (The 2026 Safety Net)

- Private credit (M&A recovery → demand)

- Infrastructure (power & digital grids)

- Hedge funds (volatility absorbers)

- Gold (political tail-risk hedge)

Strategic Hedges

- Commodities (inflation hedging)

- USD diversification (EUR/GBP portfolios)

- Tail-risk optionality around policy misalignment

Conclusion: 2026 = The Year of Complex Opportunity

2026 is defined by a triple paradox:

- AI accelerates productivity, but demands massive energy and physical infrastructure.

- Fiscal expansion fuels growth, but embeds inflation and deepens global government debt risks.

- Geopolitical fragmentation creates volatility, but unlocks multi-year spending cycles in defense, energy, robotics, semiconductors and reshoring.

The AI Super-Cycle is powerful enough to lift global equities again — but only if earnings deliver.

The winning strategy for 2026 is not passive exposure. It is:

- Own the AI infrastructure layer, not just the algorithms

- Rotate into Asia tech & UK industrials/defense

- Use quality credit + alternatives for downside protection

- Own commodities to hedge structural scarcity

- Lean into dispersion, not concentration

- The fragmentation paradox is clear: The world is breaking apart — but the investment opportunities are multiplying.

Please wait processing your request...

Please wait processing your request...