Key Takeaways for Investors and Businesses

- Fiscal Credibility Over Growth: Chancellor Rachel Reeves' Budget secures £26 billion in new revenue, primarily through long-term freezes and wealth levies, prioritizing fiscal stability over immediate, broad-based economic growth stimulus.

- The Rise of the "Stealth Tax": The extension of the Income Tax and National Insurance threshold freeze until 2030/31 is the largest revenue-raiser (£12.7 billion annually), representing a multi-year, indirect squeeze on middle and high-income household disposable income.

- Targeting High-Earner Wealth: New levies, including a cap on pension salary sacrifice NICs exemption (£2,000 limit) and increased tax rates on unwrapped savings/dividend income, necessitate urgent financial planning and structural changes in high-earning sectors.

- Domestic Focus and Value Chain Winners: The policy rotation favors sectors exposed to the domestic UK economy, specifically Retail/Hospitality (due to permanent Business Rates Relief), UK Domestic Banking (due to fiscal stability and higher nominal GDP), and Construction/Infrastructure (due to targeted capital spending).

- Losers in the Wealth Ecosystem: High-end services, wealth management, and the super-prime residential property market face direct headwinds from the new wealth-focused levies. The Mansion Tax surcharge directly impacts homes valued over £2 million.

Source: Kalkine Group

The Budget That Targeted Wealth, Not Income Rates

Chancellor Rachel Reeves' 2025 Budget marks a seismic and unconventional fiscal shift. It successfully addresses the substantial challenge of stabilizing the UK’s public finances by raising a staggering £26 billion through structural reforms and carefully calibrated "stealth taxes," rather than resorting to the headline Income Tax or VAT hikes that were widely feared across the political spectrum.

The core of this strategy is a deep, multi-year fiscal drag coupled with targeted levies on accumulated wealth and the specific benefits enjoyed by high earners. The goal is two-fold and clear: first, to establish a robust £22 billion fiscal buffer, restoring the UK's fiscal credibility; and second, to fund key social policies—most notably the scrapping of the politically contentious two-child benefit cap—all while steadfastly adhering to the administration's core promise not to raise basic income tax rates.

For investors, this Budget is not a moment for panic, but a critical juncture that necessitates a fundamental portfolio rotation. The strategic playbook must shift away from sectors penalised by the wealth squeeze and the long-term tax burden, and decisively towards those supported by domestic operational relief, sustained public investment, and the stable macroeconomic environment that the Budget aims to secure.

- The Revenue Engine: Fiscal Drag and the Pension Cap

The massive £26 billion revenue boost is overwhelmingly derived from measures that will accelerate over the medium term, demonstrating a politically complex, but undeniably long-sighted, fiscal strategy to rebuild the public finances.

A. The Income Tax Threshold Freeze Extension (The Stealth Tax)

The most potent and substantial revenue generator is the extension of the freeze on Income Tax and National Insurance thresholds. Originally scheduled to conclude in 2027/28, this freeze has been extended until 2030/31. The Office for Budget Responsibility (OBR) projects this single policy to raise the largest amount of revenue, an estimated £12.7 billion annually by the end of the decade.

Economic Impact: As nominal wages continue to rise (forecast to be strong in the near term due to inflation and tight labor markets), more and more workers will be pulled into the tax system and dragged into higher tax brackets. This is a direct, long-term, and significant squeeze on the disposable cash of middle and high-income households—a classic example of fiscal drag acting as a politically obscured, yet powerful, tax hike.

B. The Salary Sacrifice Pension Cap (The High-Earner Hit)

A significant structural reform targets high-earning individuals and their compensation packages. From April 2029, a £2,000 annual limit will be placed on the amount of salary that can be exchanged for an employer pension contribution without the contribution incurring National Insurance Contributions (NICs).

Sector Impact: This measure is a structural blow to compensation models in high-earning sectors such as Financial Services, Law, and Large Technology firms. It removes the substantial employer NICs saving previously enjoyed on large contributions, effectively raising the true cost of employment for these companies and fundamentally reducing the tax efficiency of pensions for high-earning employees. Financial planners and HR departments must urgently model its effect on net retirement savings and total reward packages.

C. Targeted Wealth Levies and Property Surcharges

The Budget directly targets the accumulation of passive wealth outside of tax-free wrappers.

- Dividend/Savings Income Tax: An additional two percentage point rate increase has been levied on un-wrapped savings, dividend, and property income tax rates. This move is specifically designed to incentivize and drive greater use of tax-free wrappers, such as ISAs (Individual Savings Accounts) and pensions, by making the returns on non-wrapped investments less attractive.

- Mansion Tax Surcharge: A new annual surcharge has been introduced on residential properties valued over £2 million, structured as a high-end, nationally administered Council Tax levy. While politically symbolic and aimed at fairness, its projected revenue is relatively small (£400 million). Crucially, it further chills transaction volume and liquidity in the ultra-prime residential property market.

- Market Impact: Rotation, Not Collapse

The market response was initially volatile—partly due to an OBR leak preceding the official announcement—but quickly settled into a measured reaction. The overall impression amongst analysts is that fiscal credibility has been successfully restored, though this stability has been purchased at the perceived cost of long-term economic growth optimism.

Asset Class Analysis

- Gilts & Rates: The successful announcement of a substantial revenue-raising package and the restored fiscal headroom led to a remarkably muted and stable reaction in the Gilt market. The reduction of perceived UK borrowing risk—the core achievement of the Chancellor—directly supports Gilt prices, leading to a stable or even slightly lower yield environment.

- Sterling (GBP): The pound traded sideways to slightly higher against major currencies. The injection of fiscal stability acts as a strong sterling-supportive factor, offsetting the prevailing concerns over the Budget’s potential long-term economic drag. The currency's direction will now be more heavily influenced by Bank of England (BoE) interest rate policy rather than short-term fiscal shocks.

- Property: The prime London residential market faces a structural headwind from the Mansion Tax surcharge. Conversely, commercial property and volume residential construction are seen as more sensitive to the announced business rates relief and the promise of long-term interest rate stability.

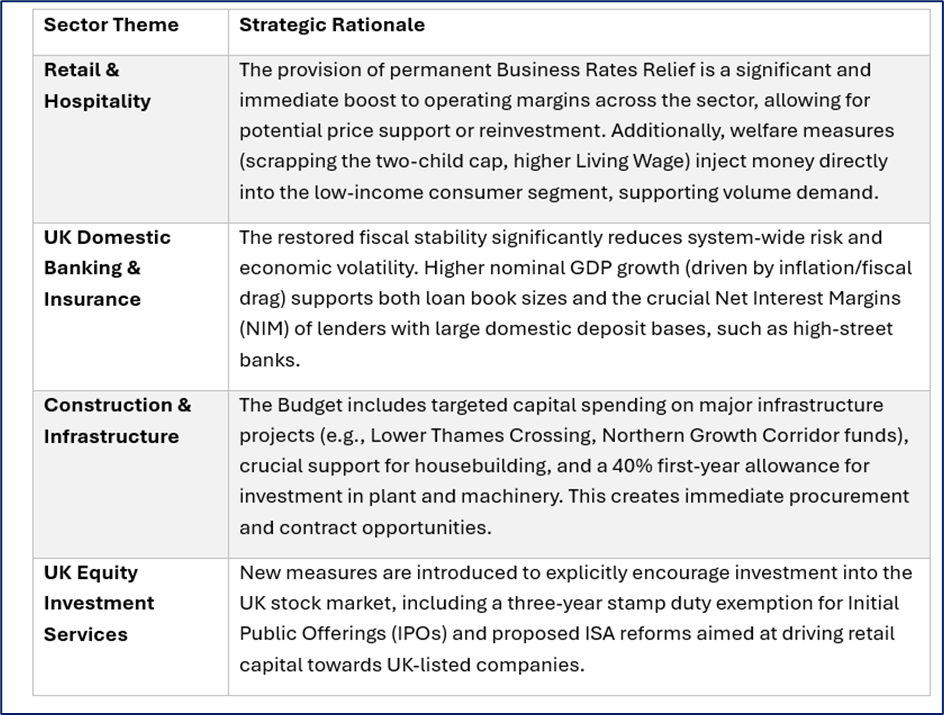

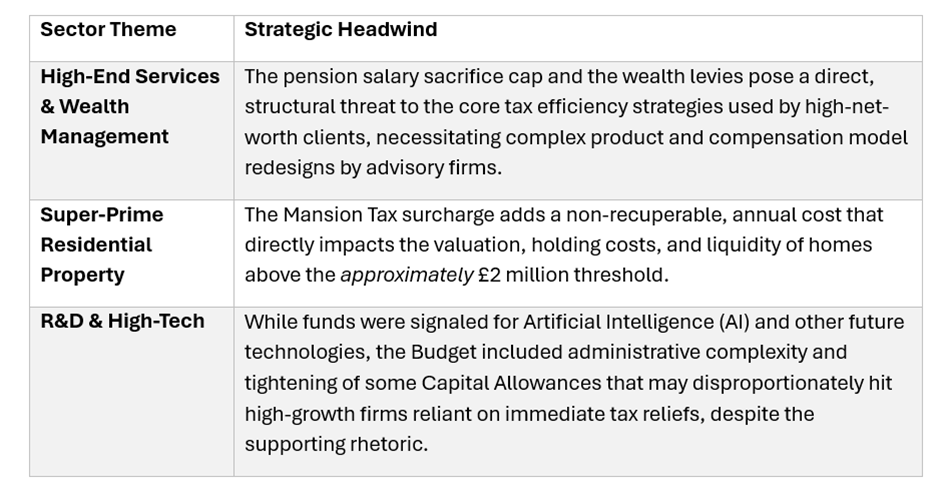

- Sector Deep Dive: Winners and Losers Under the New Playbook

This Budget fundamentally redraws the lines for UK equity sectors, explicitly favouring the domestic value chain and companies with exposure to public contracts and government spending.

The Winning Sectors

Source: Kalkine Group

The Losing Sectors

Source: Kalkine Group

- Stocks to Watch: Tactical Portfolio Adjustments (Illustrative)

Investors must move from broad sector exposure to surgical stock selection, focusing on companies best positioned to leverage the new domestic stability and spending priorities.

- Domestic Banking (WINNER): Lloyds Banking Group (LLOY), NatWest Group (NWG) – These banks have high leverage to both NIM improvement and general UK economy stability, benefiting from higher nominal growth.

- Retail/Consumer Value (WINNER): Next (NXT), Tesco (TSCO) – These giants are perfectly positioned to benefit from the direct impact of business rates relief and the expected demand shift towards the value segment of the market, supported by welfare increases.

- Construction/Housebuilding (MIXED/WINNER): Barratt Developments (BDEV), Taylor Wimpey (TW.) – While sensitive to general interest rates, they gain significant exposure to volume market housebuilding support and the announced infrastructure stimulus.

- Defence/Public Sector Tech (WINNER): BAE Systems (BA.), Qinetiq (QQ.) – Both are set to benefit directly from any increased, ring-fenced public capital spending on defense and essential government technology contracts.

- Wealth Management (LOSER): St. James's Place (STJ), Aviva (AV.) – These firms must urgently address the challenge of pension and wealth tax changes for their lucrative high-net-worth client base, forcing product restructuring.

- Large-Cap Exporters (CAUTIOUS): Diageo (DGE), AstraZeneca (AZN) – These multinational heavyweights must navigate the potential for Sterling appreciation. A stronger pound converts foreign earnings into less GBP, creating a headwind against reported revenue and earnings.

- Conclusion: A New Social Contract and The Next Challenge

Budget 2025 is a definitive statement about the UK’s new fiscal path. It confirms a permanently higher tax burden, specifically and surgically targeted at wealth and high-earner efficiencies, aimed at generating the revenue required to support public services and the lower-income demographic. Chancellor Rachel Reeves has achieved a vital, immediate goal: restoring significant fiscal headroom and injecting a much-needed sense of stability into the volatile bond market.

However, the longer-term threat remains the structural productivity gap. The tax-raising strategy, while fiscally sound and politically astute, could exacerbate the very growth problem that the OBR highlights. The fundamental acid test for this administration will not be the £26 billion in revenue raised, but whether the targeted infrastructure investment and social reforms can collectively generate the supply-side efficiencies and human capital improvements required to outperform the OBR's disappointing 1.0% annual long-term growth forecast.

For investors, the era of broad, market-based UK recovery plays is over; the focus must now transition to surgical precision and identifying those specific companies best positioned to thrive within this new, highly taxed, and domestically focused economic contract.

Please wait processing your request...

Please wait processing your request...