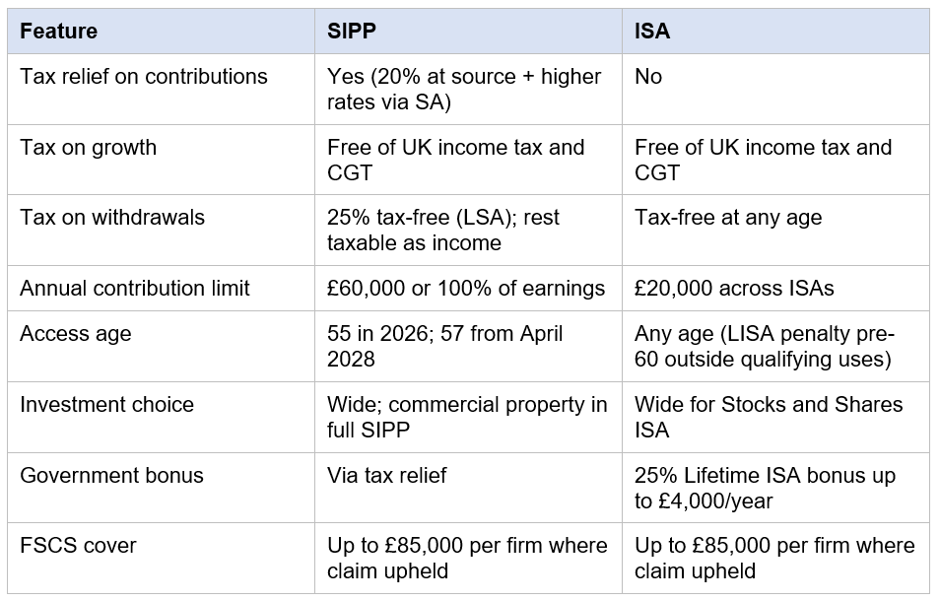

What Readers Need to Know

- SIPPs receive tax relief on contributions; ISAs do not.

- ISA money is accessible at any age; SIPP money is locked until at least the NMPA.

- The SIPP annual allowance is £60,000 in 2026/27; the ISA allowance is £20,000.

- Investment choice in both wrappers is wide for mainstream Assets.

- Most UK savers use both products as complementary parts of a long-term plan.

Introduction

The Self-Invested Personal Pension and the Individual Savings Account are arguably the two most useful long-term wrappers available to UK savers. Each carries its own tax treatment, access rules and investment scope, and each fits different goals.

This article looks specifically at how the two compare on tax relief, access and investment flexibility for the 2026/27 tax year. It is general information for UK readers and not personal advice. A regulated financial adviser can help test these ideas against an individual's circumstances.

Tax Relief Compared

Putting it together

For a higher-rate taxpayer, a SIPP contribution can deliver effective relief of 40% on the gross amount. For an additional-rate taxpayer, 45%. The ISA provides no such relief but pays off later in fully tax-free withdrawals. Which produces a better after-tax outcome depends in part on the tax band the saver expects to be in during retirement.

Access Rules Compared

ISA access

Cash, Stocks and Shares and Innovative Finance ISAs can be accessed at any age, tax-free, without penalty. Lifetime ISAs are an exception — withdrawals before age 60 outside the qualifying first-home or terminal-illness rules incur a 25% government charge, which can be more than the original 25% Bonus.

Investment Flexibility Compared

Both wrappers offer wide investment choice for mainstream assets.

- Funds, shares, ETFs and investment trusts are available in both Stocks and Shares ISAs and SIPPs.

- Cash, gilts and corporate bonds can sit inside both wrappers.

- Full SIPPs add UK commercial property; ISAs do not allow direct property holdings.

- Direct holdings of residential property are prohibited in both wrappers under HMRC rules.

- Investment platforms typically offer the same fund universe across SIPP and ISA accounts, with different charges.

Contribution Limits and Allowances

- SIPP annual allowance: £60,000 or 100% of UK Earnings if lower in 2026/27.

- Tapered annual allowance for high earners with adjusted income above £260,000 and threshold income above £200,000.

- MPAA: £10,000 once a DC pension has been flexibly accessed.

- Non-earner SIPP contribution: up to £3,600 gross.

- ISA allowance: £20,000 across all ISAs.

- Lifetime ISA cap: £4,000 (within the £20,000 total).

- Junior ISA: £9,000 for under-18s.

- Future change: from 6 April 2027, the Cash ISA allowance for under-65s is scheduled to reduce to £12,000.

Taxation in Retirement

SIPP withdrawals are taxed alongside other income — state pension, employment, rental income and so on. Taking too much in a single year can push the saver into a higher band. ISAs do not feature in tax calculations at all; withdrawals are tax-free at any size. That difference can help savers manage their tax position when paired carefully.

Lump sums from a SIPP are capped by the LSA of £268,275 across all pensions. The LSDBA of £1,073,100 sets the wider lifetime tax-free cap, including on death.

Charges and Provider Choice

SIPP and ISA charges vary widely between providers. Some platforms charge a percentage of assets; others apply flat monthly or annual fees. Most allow funds to be traded for free but charge for share, ETF and investment trust trades. Fund OCFs apply on top of the platform fee for any funds held. A pot of similar size in two different providers can incur very different total costs over a decade.

Provider choice should look beyond price. Investment menu, Customer Service, online tools, drawdown support, FCA authorisation and service track record all matter. The cheapest provider is not automatically the best — and the most expensive is not automatically premium quality.

Flexible ISA Withdrawals

Many ISAs are now 'flexible', meaning withdrawals can be replaced within the same tax year without using fresh allowance. This adds a layer of flexibility for short-term cash needs — money taken out can be repaid by the end of the tax year without reducing future ISA capacity. Not every ISA is flexible; savers should check the product terms before relying on this feature. SIPPs do not have an equivalent rule.

Inheritance and Death Benefits

Both wrappers can play a role in estate planning. SIPP death benefits paid before age 75 are normally tax-free up to the LSDBA; benefits paid after 75 are taxed at the beneficiary's marginal rate. ISAs can pass to a surviving spouse or civil partner with an Additional Permitted Subscription (APS), preserving the wrapper's tax-free status for them. The IHT treatment of pension death benefits is the subject of announced future changes; savers should follow current GOV.UK guidance.

Worked Example: Higher-Rate Taxpayer

Consider a higher-rate taxpayer with £1,000 of monthly Disposable Income to allocate. Routed entirely to a SIPP, the £1,000 gross consists of £800 paid in net, £200 added at source and £200 reclaimed via Self Assessment — effectively, the £1,000 'cost' is reduced to £600 after the additional higher-rate relief. Routed entirely to an ISA, the £1,000 is paid from after-tax income, with no further claim. Both wrappers then grow tax-free. At retirement, the SIPP allows 25% tax-free cash (subject to LSA) with the remainder taxed as income; the ISA is fully tax-free.

For a saver who expects to be a basic-rate taxpayer in retirement, the SIPP route typically delivers a better after-tax result for these working-year contributions. For a saver who expects to be a higher or additional-rate taxpayer in retirement — perhaps because of a large pension pot or rental income — the comparison is less clear, and ISAs become more attractive on the income side. This is an illustration only and not a recommendation.

Order of Saving

A common UK saving sequence is: cash reserve for emergencies; workplace pension up to at least the employer match; ISA up to a comfortable level; SIPP for additional tax-relieved long-term saving; and any further savings in GIAs or specialised wrappers. The exact order depends on individual circumstances — a higher-rate taxpayer may prioritise the SIPP over the ISA for working years, while a younger saver targeting a home may prioritise the Lifetime ISA. A regulated adviser can model the alternatives.

Junior ISA and Children's Pensions

Parents and grandparents in the UK have two main wrappers to save for a child: the Junior ISA and a children's pension. The Junior ISA allowance is £9,000 per child for 2026/27, and the funds become the child's at age 18 to use as they choose. A children's pension is technically a SIPP for the child — a non-earner SIPP allows up to £3,600 gross per year, with the child receiving 20% basic-rate tax relief at source. The child cannot access the pension until the NMPA, so the contributions support very long-term compounding. Each wrapper has its own role, and the two can run alongside each other.

Combining a SIPP and an ISA

Most UK savers do not have to choose. A common approach is to use both each tax year, in proportions tailored to the saver's tax band, time horizon and access needs.

- Maximise the SIPP for tax relief, particularly if a higher-rate taxpayer.

- Use the ISA for flexibility and tax-free withdrawals at any age.

- Coordinate withdrawals in retirement to keep marginal rates as low as possible.

- Plan around the LSA, LSDBA, MPAA and tapered annual allowance.

SIPP vs ISA — Tax, Access and Investments (2026/27)

Headline differences for UK savers.

Key Takeaways

- SIPPs offer tax relief but lock money away until pension age.

- ISAs offer tax-free withdrawals at any age but no tax relief on contributions.

- Investment choice is similar for mainstream assets; SIPPs add commercial property in full SIPPs.

- Higher-rate taxpayers typically benefit more from a SIPP in the working years.

- ISAs are particularly powerful for flexibility and tax-free retirement income.

- Combining both wrappers is common and usually advantageous.

- Personal advice is recommended for significant decisions and transfers.

_05_25_2026_04_11_58_194276.jpg)

_05_25_2026_04_09_41_320925.jpg)

Please wait processing your request...

Please wait processing your request...