What Readers Need to Know

- A SIPP is a UK-registered pension; an ISA is a tax-efficient savings or Investment account.

- SIPPs benefit from pension tax relief on contributions; ISAs offer tax-free growth and withdrawals.

- ISA money is accessible at any age; SIPP money is locked away until at least the normal minimum pension age.

- The standard ISA allowance is £20,000 for 2026/27; the SIPP annual allowance is £60,000 (or 100% of Earnings if lower).

- Many UK savers use both products together rather than choosing one over the other.

Introduction

The SIPP and the ISA are arguably the two most powerful long-term investment wrappers available to UK savers. Both shield investments from UK tax. Both offer wide investment choice. Both can be opened with relatively modest sums.

Yet the two work in fundamentally different ways. A SIPP wraps a pension around the investment — tax relief on the way in, Taxable Income on the way out, with access rules tied to pension age. An ISA wraps tax-free growth around the same kind of investments — no tax relief on contributions, no tax on withdrawals, and access at any age. This article compares the two as long-term retirement investing vehicles for the 2026/27 tax year. It is general information only and does not constitute personal advice.

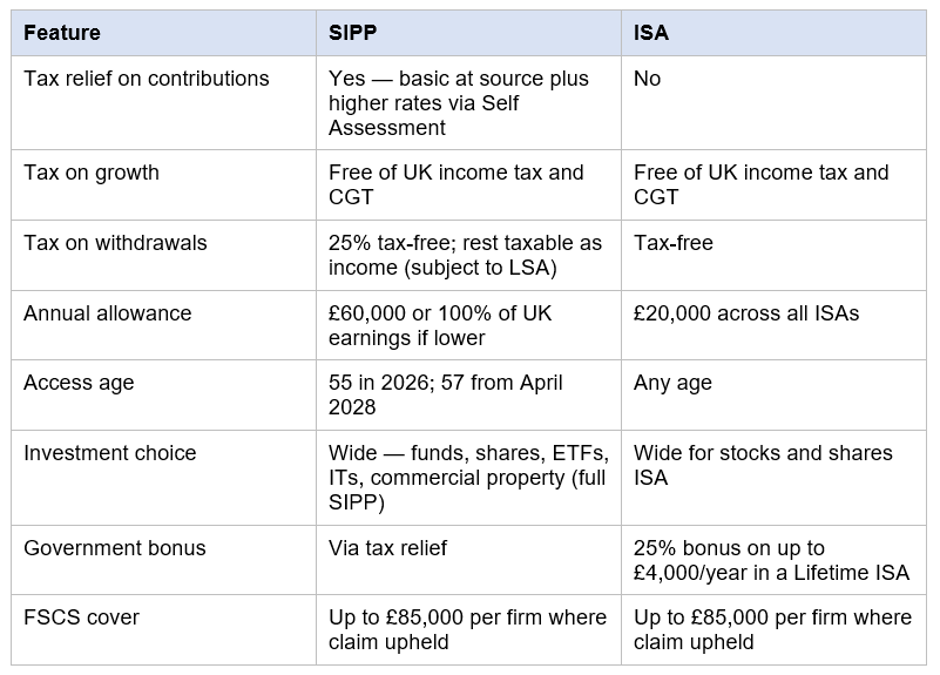

What Is a SIPP?

A SIPP is a UK-registered personal pension provided by an FCA-regulated firm. Contributions attract pension tax relief — typically 20% added at source, with higher and additional-rate taxpayers claiming further relief through Self Assessment. Investments inside the SIPP grow free of UK income tax and Capital Gains Tax. Withdrawals are taxed as income at the saver's marginal rate, although up to 25% can normally be taken tax-free, subject to the Lump Sum Allowance (LSA) of £268,275.

What Is an ISA?

An Individual Savings Account (ISA) is a UK tax-efficient savings or investment account. ISAs come in several flavours — Cash ISA, Stocks and Shares ISA, Lifetime ISA and Innovative Finance ISA — each governed by HMRC rules. Contributions are made from taxed income, so there is no tax relief. Growth and withdrawals are free from UK income tax and capital gains tax.

From 6 April 2027, the Cash ISA allowance for under-65s is scheduled to reduce from £20,000 to £12,000 following announcements in the 2025 Autumn Budget. The wider £20,000 ISA allowance for stocks and shares ISAs and ISA savings overall remains in place; savers should monitor announcements before the 2026/27 tax year closes.

Side-by-Side Comparison

Access

The clearest way to think about SIPP vs ISA is through the four headline pillars: contributions, growth, withdrawals and access.

- SIPP: normal minimum pension age — 55 in 2026, 57 from 6 April 2028.

- ISA: any time.

Allowances for 2026/27

SIPP and ISA allowances operate independently and have very different scales.

- SIPP annual allowance: £60,000 or 100% of UK earnings if lower; tapering for high earners with adjusted income above £260,000.

- MPAA: £10,000 once a DC pension is flexibly accessed.

- ISA allowance: £20,000 total across ISAs.

- Lifetime ISA cap: £4,000 per year (counted within the £20,000 overall allowance).

- Junior ISA allowance: £9,000 per year (for under-18s).

How the Same Investment Performs in Each Wrapper

The fundamental difference between a SIPP and an ISA shows up most clearly in the effective tax outcome over a lifetime. As a simplified illustration only: a basic-rate taxpayer who contributes £80 to a SIPP receives £100 in the pension after relief. Withdraw 25% tax-free and 75% taxed at basic rate — assuming the same tax band in retirement — and the after-tax outcome can be similar to or better than an equivalent ISA contribution. A higher-rate taxpayer who would draw at basic rate in retirement is typically better off in a SIPP for the working years, all else equal.

However, ISAs win on flexibility and certainty: tax-free Withdrawal at any age, no allowance interactions, and no income tax exposure on the money taken out. They are particularly powerful where the saver expects to draw before 55/57 or expects to be in the same or a higher tax band in retirement.

Tax Outcomes in Retirement

SIPP withdrawals are taxed as income, which means they interact with the personal allowance, the state pension, savings income and other taxable income. Drawing a SIPP carefully across the personal allowance and basic-rate band can keep the effective rate of tax low. ISAs do not feature in the tax calculation, which can support steadier retirement income planning.

For Inheritance Tax (IHT) planning purposes, pensions and ISAs have been treated differently from a personal estate, but the government has announced changes affecting the IHT treatment of pension death benefits with effect from a future date. Specific IHT outcomes depend on individual circumstances and the latest rules — professional advice is essential.

Using a SIPP and an ISA Together

Many UK savers use both products as complementary parts of a long-term plan. A SIPP can lock away long-dated retirement money with tax relief at the saver's highest marginal rate. An ISA can build a more flexible pot for medium-term goals, pre-retirement spending bridges or simply as a tax-efficient store of Wealth.

Couples can plan across both wrappers to make use of each partner's allowances. Higher earners with limited remaining annual allowance often prioritise SIPPs for tax relief and ISAs for flexibility. Self-employed workers sometimes use a mix of SIPP, Lifetime ISA and Stocks and Shares ISA depending on age and goals.

A Worked Example (Illustrative Only)

Imagine a higher-rate taxpayer who has £100 of gross income left to invest at the end of the month. Routed through a SIPP, the entire £100 enters the pension after tax relief — £80 contributed net plus £20 reclaimed at source, with the remaining £20 of higher-rate relief claimed via Self Assessment. Routed through an ISA, the saver takes home only £60 after 40% income tax and invests that. Both wrappers then grow tax-free. At retirement, the SIPP allows 25% tax-free and 75% taxed at the saver's marginal rate; the ISA is fully tax-free. The same gross sum can therefore produce different after-tax outcomes depending on assumed rates in retirement. This is an illustration and not a recommendation.

Risks and Limitations

- Investment risk applies to both — values can fall as well as rise.

- SIPPs lock money away until at least 55 (57 from 2028); ISAs offer flexibility but no tax relief.

- Lifetime ISA withdrawals outside the rules attract a 25% government charge.

- Pension tax rules can change; the LSA, LSDBA and tapered annual allowance are subject to future legislation.

- ISA tax rules can change; the 2025 Autumn Budget announced a future reduction in the Cash ISA allowance for under-65s from April 2027.

- Both wrappers are subject to FSCS protection limits in the event a regulated firm fails.

SIPP vs ISA Comparison (2026/27)

Headline differences between SIPPs and ISAs for UK savers.

Key Takeaways

- SIPPs offer tax relief on the way in but lock money away until pension age.

- ISAs offer flexibility, tax-free growth and tax-free withdrawals but no tax relief.

- The standard SIPP annual allowance is £60,000 in 2026/27; the ISA allowance is £20,000.

- Lifetime ISAs add a 25% government Bonus on up to £4,000 per year for eligible savers.

- Future legislation may change either or both regimes; the Cash ISA allowance for under-65s is scheduled to reduce from 6 April 2027.

- Most savers benefit from using both wrappers in combination.

- Decisions on contributions, allocation and withdrawals are best made with a regulated financial adviser.

_05_25_2026_04_11_58_194276.jpg)

_05_25_2026_04_09_41_320925.jpg)

Please wait processing your request...

Please wait processing your request...