What Readers Need to Know

- A SIPP is a UK pension wrapper; a General Investment Account is a non-tax-advantaged investment account.

- SIPPs receive tax relief; GIAs do not.

- Investments in a GIA are subject to UK Capital Gains Tax and Dividend tax outside annual exempt amounts.

- GIAs offer unlimited contributions and full flexibility, while SIPPs cap contributions and lock money away.

- For most UK investors, SIPPs and ISAs are used before GIAs, with GIAs filling specific gaps.

Introduction

The General Investment Account (GIA) — sometimes called a 'general account' or simply a 'broker account' — is the everyday wrapper most UK platforms offer alongside SIPPs and ISAs. It has no contribution limits and no access restrictions, but it also has no Tax Shelter. That makes the SIPP vs GIA decision a straightforward question of trade-offs: tax efficiency versus flexibility.

This guide compares the two wrappers for UK readers in the 2026/27 tax year. It is general information only and does not constitute personal advice. Specific tax outcomes depend on individual circumstances and a regulated adviser or Accountant should be consulted.

What Is a SIPP?

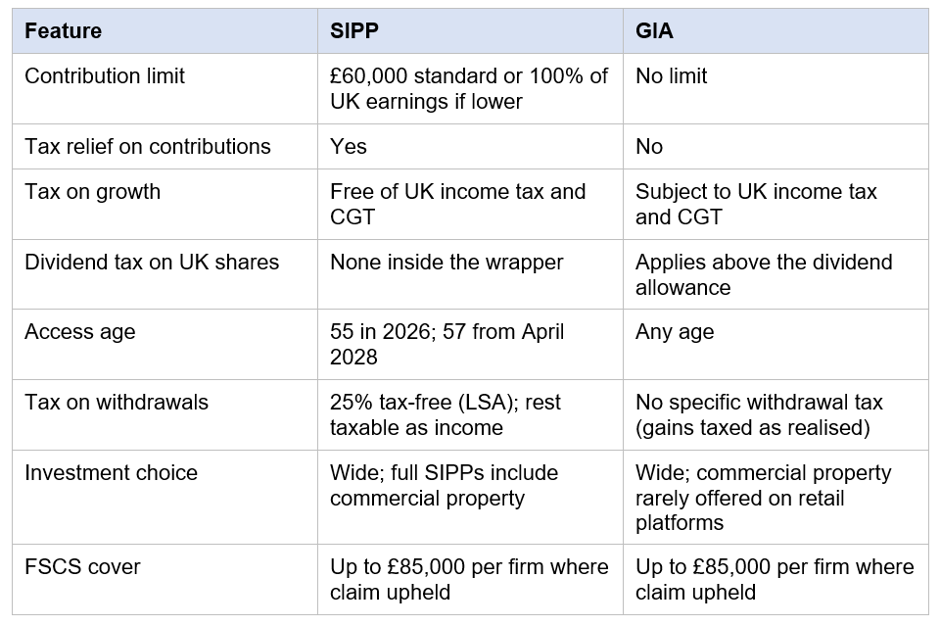

A SIPP is a UK-registered personal pension that offers wide investment choice. Contributions attract pension tax relief — 20% at source plus higher rates via Self Assessment for higher-rate taxpayers. Investments grow free from UK income tax and capital gains tax. Withdrawals are taxed as income at the saver's marginal rate, although up to 25% can be taken tax-free subject to the Lump Sum Allowance (LSA) of £268,275. Access is normally restricted until age 55 (rising to 57 from April 2028).

What Is a General Investment Account?

A General Investment Account is a non-tax-advantaged account through which an investor can buy shares, funds, ETFs, investment trusts, bonds and similar securities. There are no contribution limits and no restrictions on when money can be paid in or withdrawn. The investor pays UK tax on income and gains generated by investments held in the GIA.

Tax Treatment Side by Side

GIA

- Contributions: no tax relief; money is from taxed income.

- Income: dividends and interest taxed annually at the saver's marginal rate, subject to the dividend allowance and personal savings allowance.

- Capital gains: taxed when crystallised, subject to the annual exempt amount and prevailing CGT rates.

- Withdrawals: not taxed in themselves — but realised gains may already have been taxed.

Allowances Around the GIA

Even with these allowances, a sizeable GIA portfolio can produce material income tax and CGT bills, particularly for higher-rate and additional-rate taxpayers.

- Personal allowance for income tax — applied across all Taxable Income.

- Dividend allowance — a tax-free band for dividend income, recently reduced.

- Personal savings allowance — for interest from cash and bonds, varying by tax band.

- Capital gains tax annual exempt amount — covers a slice of realised gains each year.

- Marriage allowance and other personal reliefs — can affect GIA tax outcomes.

Where the GIA Fits in a UK Investor's Toolkit

For most UK investors, the typical order of priorities is: workplace pension up to at least the employer match; ISA up to the £20,000 annual allowance (where appropriate); SIPP for additional tax-relieved pension saving; GIA for any further investment beyond those limits.

- Higher earners who have already used the SIPP annual allowance and ISA allowance may use a GIA for additional long-term investing.

- Investors who need money before pension age and have used their ISA allowance may use a GIA as the short-to-medium-term wrapper.

- Business owners may use a GIA in conjunction with company-held investments and personal pensions.

- Trust and estate planning sometimes uses a GIA where ISA or SIPP wrappers are not available to the entity.

Investment Choice

Investment choice in a GIA is broadly similar to a platform SIPP, including UK and overseas shares, authorised funds, ETFs, investment trusts and bonds. A GIA is not subject to the HMRC taxable property regime that applies to SIPPs and SSAS schemes, but most GIAs on retail platforms do not accept direct UK commercial property in any case.

Access and Flexibility

Access is the headline advantage of the GIA. Money can be added or withdrawn at any time, in any amount. There are no early-Withdrawal penalties beyond any platform-specific fees. This flexibility is particularly valuable for shorter horizons, emergency reserves above cash savings or unexpected funding needs.

By contrast, SIPP money is locked until the normal minimum pension age — 55 in 2026, rising to 57 in April 2028 for most members. That lock can be a strength, building disciplined long-term saving, or a weakness, depending on the saver's circumstances.

Capital Gains Tax and Dividend Tax in More Detail

Capital gains realised inside a GIA are taxed when an asset is sold (or where an event such as a corporate action triggers a disposal). The annual exempt amount covers a slice of gains each year; the rest is taxed at applicable CGT rates depending on the saver's income band and asset type. Frequent trading can quickly generate taxable gains in a GIA, where in a SIPP or ISA the same trades would not. Some investors use a 'Bed and ISA' strategy — selling an asset in the GIA and immediately repurchasing it inside an ISA — to use the annual exempt amount and gradually move holdings into a tax shelter.

Dividends received in a GIA are taxed alongside other income, subject to the dividend allowance. Bonds and cash held in a GIA generate interest taxed under the personal savings allowance rules. Overseas dividends may also be subject to Withholding tax depending on the country of issue, with double taxation agreements potentially reducing the headline rate.

Where the SIPP Wins

- Tax relief on contributions — particularly for higher and additional-rate taxpayers.

- Tax-free compounding inside the wrapper.

- 25% tax-free cash on withdrawal (subject to LSA).

- Useful estate planning features (subject to changing rules).

- Discipline of locking money away until pension age.

Where the GIA Wins

- Unlimited contributions — beyond pension and ISA allowances.

- Full flexibility on access at any age.

- No specific HMRC investment restrictions (taxable property aside).

- Can be used by entities such as trusts and companies that cannot hold pensions or ISAs.

- Useful for short and medium-term goals where pension money is unsuitable.

Worked Example (Illustrative Only)

Consider a higher-rate taxpayer comparing a £10,000 gross investment over 20 years. Inside a SIPP, the contribution attracts 40% relief in total — basic-rate at source and higher-rate via Self Assessment — and grows tax-free. Inside a GIA, the £10,000 is from already-taxed income; growth is subject to dividend tax above the dividend allowance and CGT above the annual exempt amount each time gains are realised. Even before considering tax-free cash on withdrawal, the SIPP typically produces a meaningfully larger after-tax pot if the saver expects to be at the same or a lower marginal rate in retirement. Figures depend on assumed returns and tax rates and should be illustrated by a regulated adviser, who can model the cash flows across different scenarios and tax bands with the saver's specific position in mind.

Risks and Practical Considerations

- Investment risk — values can fall as well as rise in any wrapper.

- Tax-rule risk — both the SIPP and GIA tax regimes can change.

- Discipline risk — easy access to a GIA can make withdrawal tempting at the wrong time.

- Record-keeping risk — GIA gains and dividends must be tracked for Self Assessment.

- Complexity risk — combining wrappers requires planning and sometimes professional input.

SIPP vs GIA at a Glance (2026/27)

A simple summary of headline differences.

Key Takeaways

- SIPPs offer tax relief but lock money away and cap contributions.

- GIAs offer unlimited flexibility but full UK tax exposure on income and gains.

- Most UK investors prioritise pensions and ISAs before using a GIA.

- Higher-rate taxpayers usually find SIPPs more efficient for long-term saving.

- GIAs are useful where SIPP and ISA allowances are exhausted or where access is needed.

- Combining wrappers strategically is common and can be very effective.

- Personal tax outcomes depend on circumstances — regulated advice is recommended.

_05_25_2026_04_11_58_194276.jpg)

_05_25_2026_04_09_41_320925.jpg)

Please wait processing your request...

Please wait processing your request...