What Readers Need to Know

- A SIPP is a UK pension wrapper with tax relief on contributions; a Lifetime ISA is an ISA with a 25% government Bonus.

- Lifetime ISAs can only be opened by UK residents aged 18 to 39, with contributions allowed until age 50.

- Lifetime ISA withdrawals before age 60 outside the qualifying first-home or terminal-illness rules incur a 25% government charge.

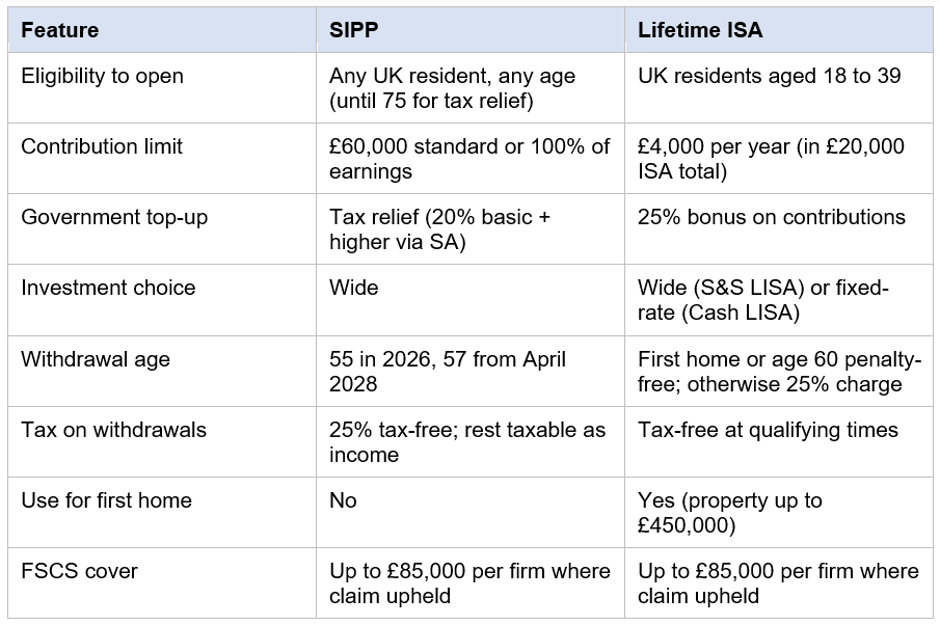

- SIPPs are accessible from the normal minimum pension age — 55 in 2026, rising to 57 from April 2028.

- Combining a SIPP and a Lifetime ISA is common, particularly for eligible younger savers.

Introduction

The Lifetime ISA was launched in April 2017 to support younger UK savers buying their first home or saving for later life. The Self-Invested Personal Pension has been around for more than three decades. The two have overlapping retirement goals but very different rules.

This article compares the SIPP and the Lifetime ISA as routes to UK retirement saving in the 2026/27 tax year. It is general information for UK readers and not personal advice. A regulated financial adviser can help match wrapper choice to personal goals.

What Is a SIPP?

A SIPP is a Self-Invested Personal Pension regulated by the FCA. Contributions attract pension tax relief — 20% at source plus higher rates via Self Assessment for higher-rate taxpayers. Investments grow free from UK income tax and CGT. Withdrawals are taxed as income at the saver's marginal rate, with up to 25% available tax-free subject to the Lump Sum Allowance (LSA) of £268,275. The normal minimum pension age is 55 in 2026, rising to 57 from 6 April 2028.

What Is a Lifetime ISA?

A Lifetime ISA (LISA) is a type of ISA designed to help with first-home purchase or retirement. UK residents aged 18 to 39 can open a Lifetime ISA, and contributions are allowed until age 50. The government adds a 25% bonus on contributions of up to £4,000 per tax year — a maximum bonus of £1,000 per year.

Lifetime ISA withdrawals fall into the qualifying first-home or age-60 rules, or attract a 25% government charge. The charge on non-qualifying withdrawals applies to the whole Withdrawal, including the contribution, the bonus and any growth — meaning it can leave the saver with less than they originally put in.

Eligibility Compared

- SIPP — any UK resident with relevant Earnings can contribute up to 100% of earnings or the £60,000 annual allowance; non-earners can contribute up to £3,600 gross.

- Lifetime ISA — UK residents aged 18 to 39 only at the point of opening; contributions allowed until age 50.

- SIPP has no upper age limit on opening or contributing (though tax relief stops at age 75).

- Lifetime ISA contributions count within the £20,000 overall ISA allowance.

Tax Relief vs Government Bonus

Pension tax relief at 20% is mathematically very similar to a 25% bonus on the net contribution. A £4,000 SIPP contribution by a basic-rate taxpayer becomes £5,000 once 20% relief is added at source. A £4,000 Lifetime ISA contribution receives a 25% bonus, taking it to £5,000. The percentages differ because the SIPP's 20% is calculated on the gross figure while the Lifetime ISA's 25% is calculated on the net figure — the cash result is the same.

Higher-rate and additional-rate SIPP contributors can claim further relief through Self Assessment, taking effective relief to 40% or 45% on the gross contribution. Lifetime ISAs do not offer additional relief for higher earners — the bonus is fixed at 25%.

Access Rules

- SIPP — normal minimum pension age (55 in 2026; 57 from April 2028).

- Lifetime ISA — penalty-free for a first home of up to £450,000 (after holding the LISA for at least 12 months) or from age 60.

- Lifetime ISA — withdrawals outside the qualifying rules attract a 25% government charge.

- Lifetime ISA — terminal illness withdrawals may be allowed without the charge under HMRC rules.

Contribution Limits

- SIPP — £60,000 standard annual allowance for 2026/27 (or 100% of earnings if lower); tapering for high earners; £10,000 MPAA after flexible access; £3,600 gross for non-earners.

- Lifetime ISA — £4,000 per tax year, within the £20,000 ISA overall allowance.

- Junior ISA and Lifetime ISA cannot be paid into in the same year for the same individual under specific rules.

Investment Choice

Both SIPPs and Lifetime ISAs are available from FCA-regulated providers in stocks-and-shares versions. Investment choice is generally wide — funds, shares, ETFs, investment trusts — though some Lifetime ISA providers offer a narrower menu than a typical platform SIPP. Cash Lifetime ISAs are also available for savers who prefer guaranteed interest rather than market exposure.

Tax in Retirement

Lifetime ISA withdrawals from age 60 are tax-free in the same way as any other ISA. SIPP withdrawals are taxed as income at the saver's marginal rate above the 25% tax-free element. The combined effect can favour the SIPP for higher-rate taxpayers in the working years and the Lifetime ISA for steadier tax-free retirement income — but the comparison is sensitive to assumptions about future tax bands.

First Home Use Case

The Lifetime ISA's distinctive feature is the ability to use the savings — including the bonus — for a first home of up to £450,000 in the UK. The property must be the saver's only home, financed with a Mortgage and bought through a conveyancer. The property price cap has been in place since the scheme launched in 2017 and the £450,000 limit applies across all UK regions, which has attracted criticism as house prices have risen in some areas.

A SIPP cannot be used for a first home unless the saver waits until pension age — meaning a Lifetime ISA is unique in supporting both a first home and retirement from one pot.

When the Lifetime ISA Tends to Suit

- Younger savers who can take advantage of the 18 to 39 eligibility window.

- First-time buyers aiming at a UK home priced up to £450,000.

- Basic-rate taxpayers (or non-taxpayers) for whom 25% bonus equals or exceeds typical pension tax relief.

- Savers comfortable locking funds until a first home or age 60.

When the SIPP Tends to Suit

- Higher and additional-rate taxpayers, where 40% or 45% effective relief beats the 25% Lifetime ISA bonus.

- Savers who have already used the Lifetime ISA or are over the age limit.

- Savers wanting the wider contribution capacity of the £60,000 annual allowance.

- Savers prioritising long-term retirement income over flexibility around a first home.

Risks and Practical Considerations

Both wrappers carry investment risk where invested in stocks-and-shares form. Cash Lifetime ISAs do not carry Market Risk but pay variable interest. The Lifetime ISA's 25% government charge on non-qualifying withdrawals is the headline risk for younger savers — life circumstances can change, and a withdrawal a few years after contributing can leave the saver with less than they originally paid in.

SIPP money is locked until pension age, which is a feature for retirement discipline and a constraint for any pre-retirement need. Tax rules around both wrappers have changed in the past and may change again; planning around historic rules without ongoing review is risky.

Using Both Wrappers

Many UK savers under 40 use a Lifetime ISA alongside a SIPP. The Lifetime ISA contribution of up to £4,000 captures the government bonus; the SIPP carries additional tax-relieved contributions. Combining both gives flexibility on first-home purchase, tax-free withdrawals at 60 and tax-relieved retirement saving.

SIPP vs Lifetime ISA — Headline Comparison

Key features for UK savers in 2026/27.

Key Takeaways

- SIPPs and Lifetime ISAs both support retirement saving but have different rules.

- Lifetime ISAs are limited to savers aged 18 to 39 to open and 18 to 50 to contribute.

- The Lifetime ISA's 25% bonus is similar in cash terms to basic-rate pension tax relief.

- Higher-rate taxpayers typically benefit more from SIPP contributions.

- Lifetime ISA withdrawals outside the qualifying rules attract a 25% government charge.

- Combining both wrappers is common for eligible younger savers.

- Personal advice is recommended for significant decisions.

_05_25_2026_04_11_58_194276.jpg)

_05_25_2026_04_09_41_320925.jpg)

Please wait processing your request...

Please wait processing your request...