What Readers Need to Know

- SIPPs were introduced in 1989 by then-Chancellor Nigel Lawson and launched commercially in 1990.

- The 2006 'A-Day' pension simplification reforms removed many restrictions on contributions and investments.

- Pension freedoms in April 2015 expanded drawdown access and removed the requirement to buy an Annuity.

- The market is now regulated by the FCA, with rules tightened following high-profile cases of unsuitable investments.

- SIPPs remain personal pensions — they are not an unregulated Investment account.

Introduction

The Self-Invested Personal Pension was once a specialist product for wealthy investors with bespoke needs. Three decades later, it is one of the most familiar UK retirement wrappers, used by self-employed workers, contractors, family Business owners, higher earners and engaged investors. The journey says a lot about how UK Retirement Planning has evolved.

This article tells the SIPP story for UK readers in the 2026/27 tax year — how the wrapper began, the legislative milestones that shaped it, and the cases that prompted today's regulatory landscape. It is general information only and does not constitute personal advice. Anyone considering a SIPP should speak to a regulated financial adviser.

1989: The Birth of the SIPP

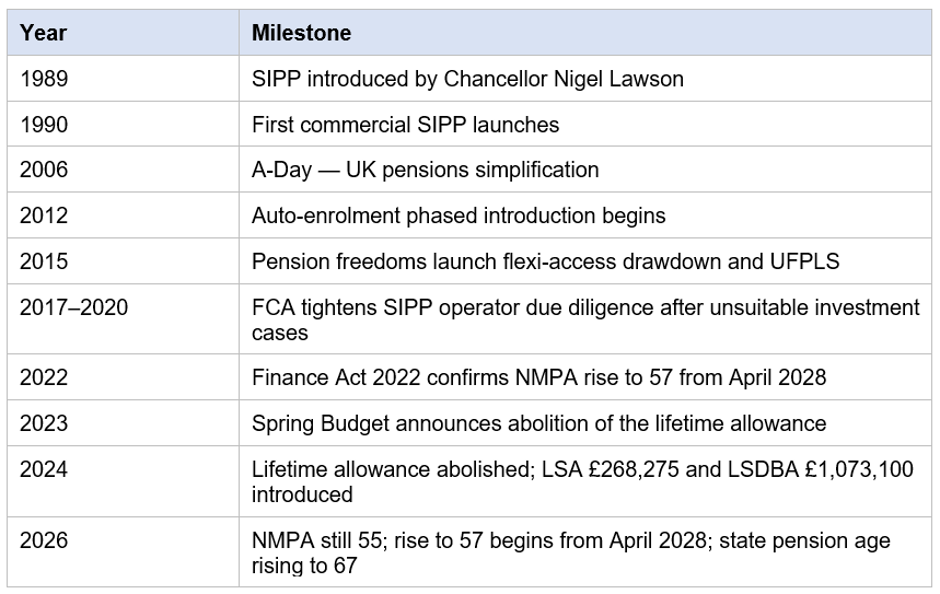

The SIPP traces its origins to a 1989 Budget speech by Chancellor Nigel Lawson. Aiming to give savers more control of their pension investments, the Treasury announced that personal pensions could allow members to manage their own choices, within HMRC limits. The Joint Office of Inland Revenue and the Department of Social Security followed with a Joint Office Memorandum setting out the practical rules.

The first commercial SIPP launched in 1990. Early take-up was modest — these were specialist products for high-net-worth investors with access to advice and an appetite for investment control.

The 1990s: A Specialist Market

Through the 1990s, SIPPs sat alongside Retirement Annuity Contracts and Personal Pensions as a self-direction option for those who wanted it. Charges were typically high. The investment menu was narrower than today's because UK platforms and modern fund distribution were still emerging.

Around this time, the Small Self-Administered Scheme — for business owners — was also evolving. SSAS schemes had their own legacy dating back further but were used in similar territory: pooled, flexible occupational pensions with property and loanback features.

2006: A-Day and Pensions Simplification

On 6 April 2006 — known as 'A-Day' — the UK introduced sweeping pensions simplification. The reforms unified the tax framework for registered pension schemes, introduced the annual allowance and lifetime allowance, and allowed wider categories of investment inside pensions. The reforms expanded the appeal of SIPPs to a much broader audience.

Around the same time, the rise of digital investment platforms made SIPPs more accessible. New 'platform SIPPs' targeted retail investors with low cost, broad fund choice and online execution. The market began to fragment between traditional 'full SIPPs' (with property and specialist Assets) and platform SIPPs.

Auto-Enrolment and the Workplace Pension Era

From 2012 onwards, the introduction of auto-enrolment brought millions of UK workers into workplace pension saving for the first time. Default fund design, the 0.75% charge cap and master trusts shaped much of the market. The SIPP did not replace workplace pensions — it complemented them, offering wider investment choice for those who wanted to top up or consolidate.

2015: Pension Freedoms

Chancellor George Osborne's pension freedoms, introduced in April 2015, may be the single most influential change to UK pensions in the SIPP era. The reforms removed the effective requirement to buy an annuity, allowed flexi-access drawdown and UFPLS from DC pensions, and let savers shape their own retirement income strategy.

Pension freedoms drove substantial inflows into SIPPs as savers consolidated old pots and chose drawdown-friendly platforms. The reforms also created the MPAA — the £10,000 cap on DC contributions for anyone who flexibly accesses their pension — and triggered the launch of Pension Wise, the free guidance service for over-50s.

2017–2020: Regulatory Tightening

Alongside its growth, the SIPP market produced high-profile cases of unsuitable investments — overseas property bonds, store pods, car park investments and unregulated collective investment schemes (UCIS) — held inside SIPP wrappers and often sold via cold calls or 'free pension reviews'.

The FCA tightened SIPP operator Due Diligence requirements, the Financial Ombudsman Service upheld a wave of complaints, and the FSCS paid substantial compensation. Several SIPP operators withdrew from non-mainstream investments altogether. The market that emerged is more cautious, with operators applying stricter permitted-assets lists.

2022–2024: Pension Age and Tax Changes

The Finance Act 2022 confirmed the rise of the Normal Minimum Pension Age to 57 from 6 April 2028. The 2023 Spring Budget announced the abolition of the lifetime allowance, with the Finance Act 2024 introducing replacement Lump Sum Allowances from 6 April 2024 — the LSA of £268,275 and the LSDBA of £1,073,100.

These changes simplified the rules around the largest pensions but kept the focus on tax-free cash and death benefits caps. SIPP providers updated their administration to handle the new framework.

Today's SIPP Market

The 2026/27 SIPP market is large, varied and competitive. Headlines include:

- Hundreds of thousands of UK savers hold SIPPs across mainstream platforms.

- Charges have generally fallen, with percentage and flat-fee structures both common.

- Investment menus run from index trackers to investment trusts to UK commercial property.

- Drawdown is the dominant income strategy, with annuities re-emerging as interest rates have changed.

- FCA due diligence rules and tighter operator permitted-asset lists have reduced exposure to non-mainstream assets.

- Pension Wise and MoneyHelper provide free guidance; regulated advisers provide personalised advice.

The Growth of Drawdown

Before pension freedoms, the typical retirement decision for a DC pension was when to buy an annuity. Annuity rates set the income for life. Drawdown existed but was hemmed in by Government Actuary's Department (GAD) limits and was used by a minority of savers. The 2015 reforms removed the effective requirement to annuitise, allowed flexi-access drawdown and let savers shape their own income strategy. Within a few years, drawdown overtook annuities as the most common retirement income choice.

The growth of drawdown placed more responsibility on savers — managing investment risk, sequence-of-returns risk, longevity risk and the MPAA. Many platforms responded with drawdown-friendly account features, investment pathways for non-advised savers and clearer integration with Pension Wise guidance.

Where SIPPs Sit Alongside Other Wrappers

Today's UK retirement planning landscape rarely uses a single wrapper. Workplace pensions, SIPPs, SSAS schemes (for business owners), ISAs and Lifetime ISAs combine to serve different goals. SIPPs sit firmly in the 'individual self-direction' category — flexible investment choice and tax relief, balanced against the responsibilities of choosing investments and managing charges over decades.

How SIPPs Compare with International Self-Direction

UK readers sometimes ask how the SIPP compares with self-directed retirement structures abroad. The Australian Self-Managed super fund (SMSF) is the most frequent comparison. The headline similarities — wider investment choice than a default scheme, more individual responsibility — are real. The detail is entirely different. SMSFs sit under Australian regulation by the Australian Taxation Office and APRA, with their own contribution caps, investment restrictions and audit regime. UK SIPPs sit under HMRC and FCA rules. Tax treatment, access ages and reporting are not interchangeable.

The same caution applies to US, Canadian and European structures. Cross-border savers — particularly those returning to or leaving the UK — should take specialist international pension advice rather than assume similar rules apply.

Lessons from 35 Years of SIPPs

- Investment choice is valuable but not the same as good outcomes.

- Charges matter — they compound over decades.

- Due diligence on operators and investments protects savers.

- Cold calls and 'free pension reviews' remain warning signs.

- Defined benefit transfers usually require regulated advice.

- Long-term saving discipline often beats clever investment moves.

- Regular review of allowances, charges and investments keeps plans on track.

SIPP Timeline at a Glance

Key UK milestones in the SIPP story.

Key Takeaways

- SIPPs were introduced in 1989 and launched in 1990.

- A-Day in 2006 simplified the UK pensions framework and broadened SIPP appeal.

- Pension freedoms in 2015 made drawdown the default income strategy for many.

- Regulatory action since 2017 has tightened operator due diligence and protected savers.

- Today's SIPP market combines low-cost platforms with full SIPPs for specialist needs.

- SIPPs are one piece of a wider UK retirement toolkit alongside workplace pensions, SSAS, ISAs and the Lifetime ISA.

Frequently Asked Questions

Q: Who introduced the SIPP?

A: Then-Chancellor Nigel Lawson announced the SIPP in his March 1989 Budget speech, with implementing rules following from the Joint Office of Inland Revenue and the Department of Social Security. The first SIPP launched commercially in 1990.

Q: What were pension freedoms?

A: Pension freedoms came into force in April 2015 under Chancellor George Osborne. They removed the effective requirement to buy an annuity at retirement, allowed flexi-access drawdown and UFPLS from DC pensions, and introduced the MPAA.

Q: How is the SIPP market regulated today?

A: SIPP operators are regulated by the FCA. SIPP investments must comply with HMRC rules including the taxable property regime. The FCA has tightened due diligence requirements over the past decade and the FSCS may pay compensation in cases of upheld claims.

Q: Are SIPPs still relevant after auto-enrolment?

A: Yes. Auto-enrolment brought millions of UK workers into workplace pension saving but SIPPs continue to play a role in consolidation, additional contributions, wider investment choice and self-employed pension planning.

Q: How has the lifetime allowance change affected SIPPs?

A: The lifetime allowance was abolished from 6 April 2024 and replaced by the LSA of £268,275 and LSDBA of £1,073,100. Tax-free cash and death benefits are now capped by those allowances. SIPP administrators handle the new framework as part of standard scheme reporting.

Q: Where can I learn more about SIPPs?

A: GOV.UK pension pages, the HMRC Pensions Tax Manual, the FCA's information for consumers, MoneyHelper and Pension Wise all provide free guidance. Personalised recommendations require a regulated financial adviser.

Please wait processing your request...

Please wait processing your request...