What Readers Need to Know

- The annual allowance limits how much can be paid into UK pensions each tax year with tax relief.

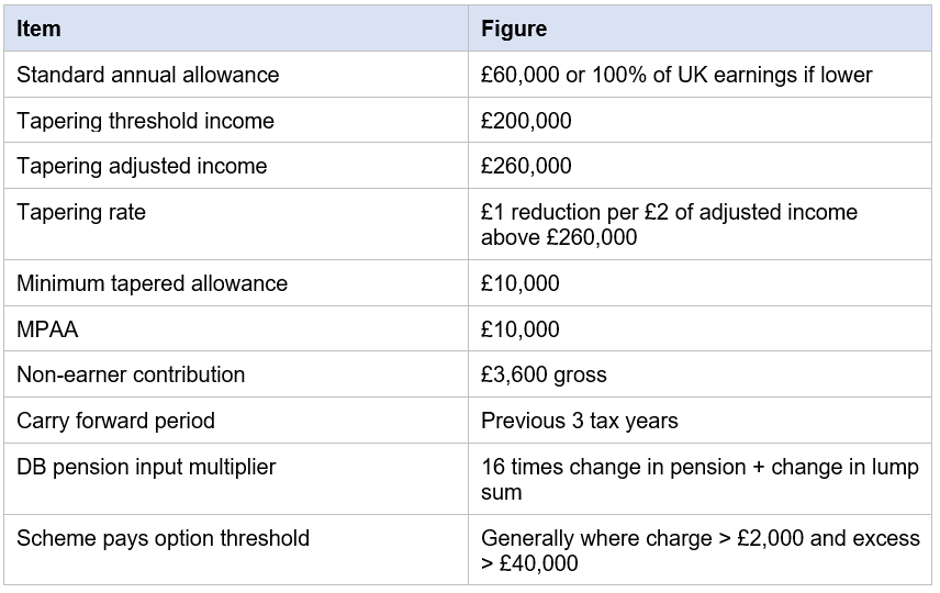

- The standard annual allowance for 2026/27 is £60,000 or 100% of UK Earnings if lower.

- Tapered annual allowance applies to high earners with adjusted income above £260,000.

- The MPAA caps DC contributions at £10,000 after flexible access.

- Carry forward can use unused allowance from the previous three tax years.

Introduction

The annual allowance is one of the most important — and most misunderstood — UK pension rules. It governs how much can be paid into UK registered pensions in a tax year with tax relief, and how much is subject to an annual allowance charge if exceeded.

This article explains the annual allowance for UK readers in the 2026/27 tax year, including the tapered annual allowance, the MPAA and carry forward. It is general information and not personal advice. Specific outcomes depend on personal circumstances and benefit from regulated advice or accountancy input.

The Annual Allowance in One Sentence

The annual allowance is the maximum amount of pension contributions — from the saver, employer and tax relief — that can be paid into UK registered pension schemes in a tax year before an annual allowance charge applies.

Standard Annual Allowance

For 2026/27, the standard annual allowance is £60,000. Personal contributions are also limited to 100% of relevant UK earnings, so a saver earning £40,000 can normally contribute up to £40,000 gross from personal contributions, not £60,000. Employer contributions are not constrained by earnings but count towards the £60,000 cap.

Why the Annual Allowance Exists

The annual allowance is the UK government's main lever for controlling the cost of pension tax relief. By capping the contributions that receive relief, it limits how much taxpayers can subsidise retirement saving for any one saver in a single year. The current £60,000 limit was set from April 2023, having previously stood at £40,000 for many years. Future changes would require legislation.

Who Is Affected

The annual allowance applies to anyone who is a member of a UK registered pension scheme — including SIPPs, personal pensions, stakeholder pensions, workplace pensions, SSAS schemes, and DB schemes.

Tapered Annual Allowance

Where both conditions are met, the annual allowance reduces by £1 for every £2 of adjusted income above £260,000, down to a minimum of £10,000. The taper bottoms out at adjusted income of £360,000.

- Threshold income exceeds £200,000 — total Taxable Income minus personal pension contributions.

- Adjusted income exceeds £260,000 — total taxable income plus employer pension contributions.

Money Purchase Annual Allowance (MPAA)

Once a saver flexibly accesses a defined contribution pension by taking taxable income, the MPAA of £10,000 replaces the standard annual allowance for DC contributions. Carry forward does not apply to the MPAA. Defined benefit accrual remains subject to a higher 'alternative annual allowance' but most savers in DB schemes are not affected.

Taking only the 25% tax-free cash from flexi-access drawdown does not normally trigger the MPAA. Small pots taken under the small lump sum rules also do not normally trigger the MPAA, subject to specific HMRC conditions.

Carry Forward

Carry forward is most useful for self-employed savers, directors and others with uneven income who can make larger contributions in a single year.

- The saver was a member of a UK registered pension scheme during each of the three previous tax years.

- The current year's annual allowance is used in full first.

- Personal contributions still cannot exceed 100% of relevant UK earnings in the current year.

- Tapered allowance and MPAA may limit the amount available.

Pension Input Amount and DB Pensions

For DB pensions, the 'pension input amount' is based on the change in the value of accrued benefits between the start and end of the tax year, using a standard multiplier (currently 16 times the change in pension plus the change in any separate lump sum). Pay rises during the year can therefore create significant pension input amounts.

Tax Year Timing

The annual allowance applies to the UK tax year — 6 April to 5 April. Contributions are normally counted in the tax year they are received by the pension scheme, although certain timing rules apply to pension input periods that align with the tax year for all UK registered pensions since 2016.

Higher-rate taxpayers using Self Assessment can claim relief on contributions made up to the end of the tax year. Last-minute contributions in late March or early April are common around tax year planning, especially among self-employed and director savers.

Worked Examples (Illustrative Only)

High earner subject to tapering

A saver with adjusted income of £300,000 has a tapered annual allowance of £40,000 (£60,000 reduced by £20,000, calculated as £40,000 of adjusted income above £260,000 divided by 2). Total contributions above £40,000 would attract an annual allowance charge.

Annual Allowance Charge

If contributions exceed the available annual allowance, the excess is subject to an annual allowance charge — added to the saver's taxable income and taxed at their marginal rate. The charge effectively claws back the tax relief on the excess.

In some cases — typically where the charge exceeds £2,000 and the excess is over £40,000 — the saver can ask the pension scheme to pay the charge from the pension under the 'scheme pays' option. This reduces the immediate cash impact but also reduces the eventual pension value.

Annual Allowance and Auto-Enrolment

Auto-enrolment workplace pension contributions are limited by the 8% minimum on qualifying earnings between £6,240 and £50,270 — well within the £60,000 annual allowance for most workers. Workers with larger pension contributions from employer matching, salary sacrifice, additional voluntary contributions or a SIPP need to track total contributions across all schemes to stay within the allowance.

Higher earners and directors are most likely to encounter the annual allowance limits, particularly when employer contributions to a SSAS or large SIPP are added to workplace pension accrual.

Tracking Contributions Across Schemes

UK pension providers send annual statements showing contributions in the previous tax year. Where a saver has multiple pensions, total contributions across all schemes count towards the annual allowance. Providers do not aggregate contributions across firms — it is the saver's responsibility to track totals. A simple spreadsheet or annual review with an adviser can support this.

Where the annual allowance is exceeded, providers may issue a 'pension savings statement' identifying the excess and the saver's potential annual allowance charge. The charge is reported through Self Assessment.

Practical Tips

- Track contributions across all pensions in the tax year — workplace, SIPP, SSAS and any other registered pensions count.

- Calculate tapered allowance carefully if income is near the £200,000 or £260,000 thresholds.

- Be careful about triggering the MPAA — flexible drawdown access can permanently reduce DC contribution capacity.

- Use carry forward for one-off larger contributions, ensuring the conditions are met.

- Speak with a regulated adviser or Accountant before significant contributions or transfers.

Common Annual Allowance Mistakes

- Contributing more than 100% of relevant UK earnings as personal contributions.

- Triggering the MPAA inadvertently by taking flexible drawdown.

- Misjudging tapered allowance for high earners with Bonus or Dividend income.

- Missing carry forward conditions and overstating the available allowance.

- Failing to track total contributions across multiple pensions.

- Forgetting to include employer contributions in the total.

Where to Get Help

MoneyHelper provides free guidance on pension allowances. HMRC publishes detailed guidance on the annual allowance, tapering and the MPAA on GOV.UK. For personalised calculations, a regulated financial adviser or accountant can model scenarios across multiple tax years.

Specialist advice is particularly valuable for high earners affected by tapering, Limited Company directors planning large employer contributions, savers approaching retirement who may trigger the MPAA, and anyone planning to use carry forward to maximise contributions in a single tax year. The FCA Register confirms whether an adviser is authorised to provide pension advice.

Annual Allowance Rules at a Glance (2026/27)

Key figures for UK pension annual allowance for 2026/27.

Key Takeaways

- The annual allowance limits UK pension contributions that receive tax relief.

- The standard allowance is £60,000 for 2026/27 or 100% of UK earnings if lower.

- Tapering reduces the allowance for high earners.

- The MPAA caps DC contributions at £10,000 after flexible access.

- Carry forward can use unused allowance from the previous three years.

- Contributions across all UK pensions count.

- Regulated advice or accountancy input is recommended for significant contributions.

Please wait processing your request...

Please wait processing your request...