What Readers Need to Know

- A SIPP is a UK personal pension that lets the saver choose their own investments.

- SIPPs are regulated by the Financial Conduct Authority.

- Pension tax relief applies in the usual UK way — basic at source, higher rates via Self Assessment.

- Money is locked until the normal minimum pension age — 55 in 2026, rising to 57 from April 2028.

- SIPPs are not suitable for every saver and benefit from regulated advice.

Introduction

Search trends in UK finance have made it clear: 'what is a SIPP' is one of the most common pension questions. The Self-Invested Personal Pension is one of the most popular retirement wrappers in the UK, and the rise of low-cost platforms has brought it to a much wider audience over the past decade.

This article gives a clear, general introduction to SIPPs for UK readers in the 2026/27 tax year — what they are, how they work, their tax treatment, the investments they can hold, the access rules and the main risks. It is general information and not personal advice. A regulated financial adviser, MoneyHelper guidance or a Pension Wise appointment can help readers test these ideas against their own goals.

A SIPP in One Sentence

A SIPP is a Self-Invested Personal Pension — a UK personal pension wrapper provided by an FCA-regulated firm, where the saver chooses the investments held inside the wrapper.

How a SIPP Works

Opening a SIPP normally takes minutes online with a UK platform. The saver makes contributions — by direct debit, lump sum or transfer in — and chooses investments from the provider's permitted Assets list. The SIPP operator handles HMRC reporting, claims basic-rate tax relief at source and administers the wrapper. Investments grow free of UK income tax and CGT. From the normal minimum pension age, the saver can take 25% tax-free cash (subject to the £268,275 LSA) and draw the rest as Taxable Income, buy an Annuity, or combine both.

Tax Relief Inside a SIPP

Pension tax relief is added in line with the UK pension framework. Basic-rate relief of 20% is normally added at source — a £80 contribution becomes £100. Higher-rate (40%) and additional-rate (45%) taxpayers can claim additional relief via Self Assessment. Employer contributions to a SIPP are usually paid gross and may be allowable for corporation tax.

The standard annual allowance for 2026/27 is £60,000 or 100% of relevant UK Earnings if lower. Tapered annual allowance applies to high earners with adjusted income above £260,000 and threshold income above £200,000. The Money Purchase Annual Allowance (MPAA) of £10,000 applies once a member has flexibly accessed a DC pension.

Investment Choice in a SIPP

HMRC rules apply to all SIPPs — most importantly, the 'taxable property' regime prohibits direct holdings of residential property and personal chattels in almost all cases. SIPP operators apply their own permitted assets list on top of HMRC rules.

- Authorised UK funds — OEICs and unit trusts.

- UK and overseas shares listed on recognised exchanges.

- Exchange-traded funds (ETFs) and exchange-traded commodities (ETCs).

- Investment trusts listed on the London Stock Exchange.

- UK government gilts and corporate bonds.

- Cash and Money Market funds.

- UK commercial property (in full SIPPs only).

- Certain insurance-backed pension contracts and structured products.

Access Rules

SIPP money is locked until the normal minimum pension age (NMPA). The NMPA is 55 in 2026 and rises to 57 from 6 April 2028 for most savers. Protected pension ages may preserve earlier access for some scheme members. Ill-health early access is possible under HMRC rules.

Tax-Free Cash and the Lump Sum Allowance

Most SIPP savers can take 25% of the value of the pension as tax-free cash on crystallisation. This is now capped by the Lump Sum Allowance (LSA) of £268,275 across all UK pensions, introduced from 6 April 2024 to replace the lifetime allowance. The Lump Sum and Death Benefit Allowance (LSDBA) of £1,073,100 governs the wider lifetime tax-free amount, including on death.

Drawdown, UFPLS and Annuities

From pension age, SIPP savers can take income in several ways:

- Flexi-access drawdown — take 25% tax-free up-front and leave the rest invested for variable taxable income.

- UFPLS — take ad-hoc lump sums where each is 25% tax-free and 75% taxable.

- Annuity purchase — exchange some or all of the pension for a guaranteed income for life or for a fixed term.

- A combination of these methods is common.

Who Tends to Use a SIPP?

- Self-employed workers and freelancers without a workplace pension.

- Higher earners who want more contribution capacity than a workplace plan provides.

- Engaged investors who want to choose their own funds, shares and ETFs.

- Savers consolidating old pension pots after taking advice.

- Limited Company directors and contractors using a SIPP as part of director pension planning.

Charges

SIPP charges typically combine a platform/administration fee, dealing charges, fund OCFs and (for full SIPPs) specialist fees for property and other assets. Charges vary widely between providers. Workplace pension default funds are capped at 0.75% per year; SIPPs are not. Total expected cost should be compared based on the saver's pot size and investment style rather than headline rates alone.

Risks to Weigh

- Investment risk — values can fall as well as rise.

- Charges — fees compound over decades.

- Transfer risk — moving from a workplace or DB pension can mean losing valuable features.

- Scam risk — pension cold calls are banned in the UK; unusual investments deserve extra Due Diligence.

- Access risk — money is locked until NMPA; pension liberation schemes are dangerous.

- Drawdown risk — longevity, sequence of returns and Inflation matter in retirement.

How a SIPP Is Set Up and Run

Setting up a SIPP today is normally a matter of minutes online. The saver chooses a provider, completes a short application, sets up a direct debit or makes an initial transfer, and selects investments. Most modern SIPPs are managed entirely online, with portfolio data, dealing tools and statements all available through a single portal.

Ongoing administration is handled by the SIPP operator. Contributions, transfers in, dealing instructions, drawdown set-up and benefit payments all flow through the operator's systems. The saver's role is to make investment decisions, monitor charges and review the pension at regular intervals — typically annually or after any significant change in circumstances.

Choosing a SIPP Provider

SIPP providers in the UK range from large online platforms to specialist full-SIPP firms. The right choice depends on the investment menu the saver actually wants, the charging structure that suits their pot size and trading style, the quality of online tools and Customer Service, and the drawdown features required. Most engaged investors compare two or three providers in detail before deciding, and review the choice every few years as pot size or strategy changes. The FCA Register confirms whether a provider is authorised to offer SIPPs.

How a SIPP Fits with Other Pensions

A SIPP usually sits alongside a workplace pension, the state pension and possibly other personal pensions or ISAs. Total contributions across all schemes count towards the £60,000 annual allowance. Many UK savers run a workplace pension and a SIPP in parallel — the workplace pension for the employer contribution and the SIPP for additional flexible saving.

Reviewing a SIPP Over Time

A SIPP is not a 'set and forget' product. Charges, investments, contributions and beneficiary nominations should all be reviewed regularly — typically once a year and after any significant life event. Many UK savers schedule a review around the end of the tax year to align with allowance planning and any Self Assessment claims.

Where to Get Help

Free guidance is available through MoneyHelper (Money and Pensions Service). Pension Wise, through MoneyHelper, offers free appointments for over-50s with DC pensions, including SIPPs. Personalised recommendations require a regulated financial adviser. The FCA Register lists authorised advisers and firms.

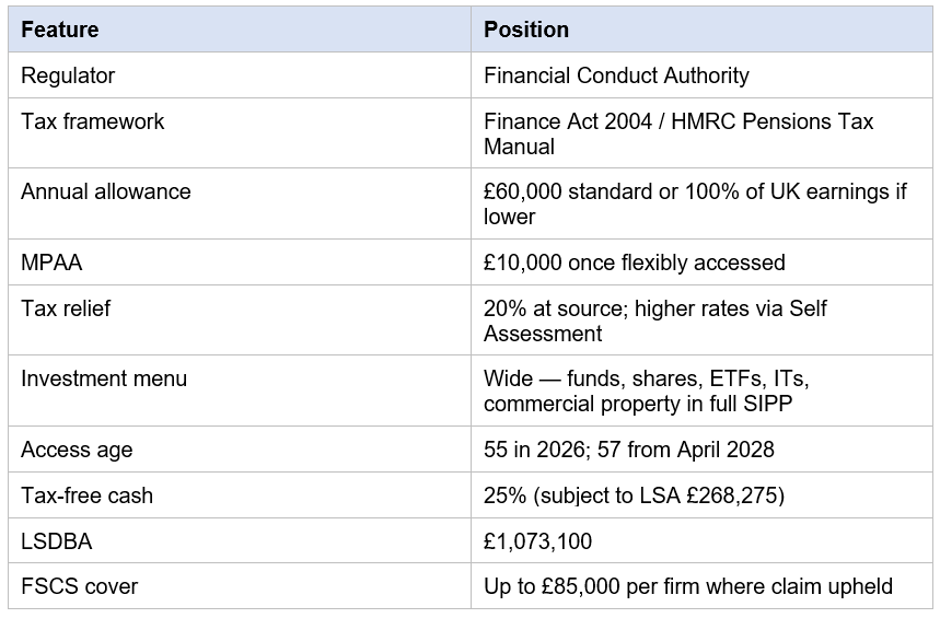

SIPP Snapshot (2026/27)

Headline features of a UK SIPP for 2026/27.

s

Key Takeaways

- A SIPP is a UK personal pension with wide investment choice.

- It is regulated by the FCA, with tax rules set by HMRC.

- Contributions benefit from pension tax relief.

- Money is locked until pension age and 25% can be taken tax-free (subject to LSA).

- Charges, transfers and investment choices need careful consideration.

- SIPPs typically sit alongside workplace pensions and ISAs in a UK retirement plan.

- Free guidance through MoneyHelper and regulated advice both help.

Please wait processing your request...

Please wait processing your request...