What Readers Need to Know

- A defined contribution (DC) pension builds an individual pot based on contributions and Investment growth.

- The pot is invested and can rise or fall with markets.

- Most workplace pensions and all SIPPs are defined contribution pensions.

- At retirement, the pot can be used through drawdown, Annuity purchase or a combination.

- DC pensions are different from defined benefit (DB) pensions, which promise a specific income for life.

Introduction

Defined contribution pensions are the most common form of pension saving in the UK today. Auto-enrolment, modern personal pensions, SIPPs and most workplace schemes operated through master trusts are all DC arrangements.

This article gives a plain-English introduction to defined contribution pensions for UK readers in the 2026/27 tax year — how they work, how the pot grows, the tax treatment and the Options at retirement. It is general information and does not constitute personal advice.

A Defined Contribution Pension in One Sentence

A defined contribution pension is a UK pension wrapper where contributions are paid in over time, invested in a chosen fund or portfolio, and used to fund retirement income from the resulting pot.

How a DC Pension Builds Over Time

A DC pension grows from three sources: the saver's contributions, any employer contributions and the investment returns earned inside the wrapper. Tax relief is added in the standard UK way — basic-rate at source, with higher and additional-rate relief via Self Assessment for relief-at-source schemes. Net pay arrangements in some workplace pensions give higher-rate relief automatically through Payroll.

Over a working career, the combination of consistent contributions, employer matching, tax relief and compounded growth can build a substantial pot. The pot belongs to the saver and travels with them between employers, subject to scheme rules and possible transfers.

DC Pensions and Investment Risk

Unlike a defined benefit pension, a DC pension does not promise a specific income. The pot rises and falls with investment performance. Most workplace DC schemes invest in a default fund — often a 'lifestyle' or 'target-date' strategy that gradually de-risks as the saver approaches retirement. Many savers also have a 'self-select' range of alternative funds within the workplace scheme.

Where DC Pensions Sit in the UK Landscape

- Workplace pensions provided by employers — most under auto-enrolment.

- Personal pensions, including stakeholder pensions and SIPPs.

- Group personal pensions arranged by employers but contracted with insurers.

- Master trusts — large multi-employer occupational DC schemes governed by independent trustees.

- Other occupational DC schemes operated by individual employers or industry bodies.

Tax Relief and Allowances

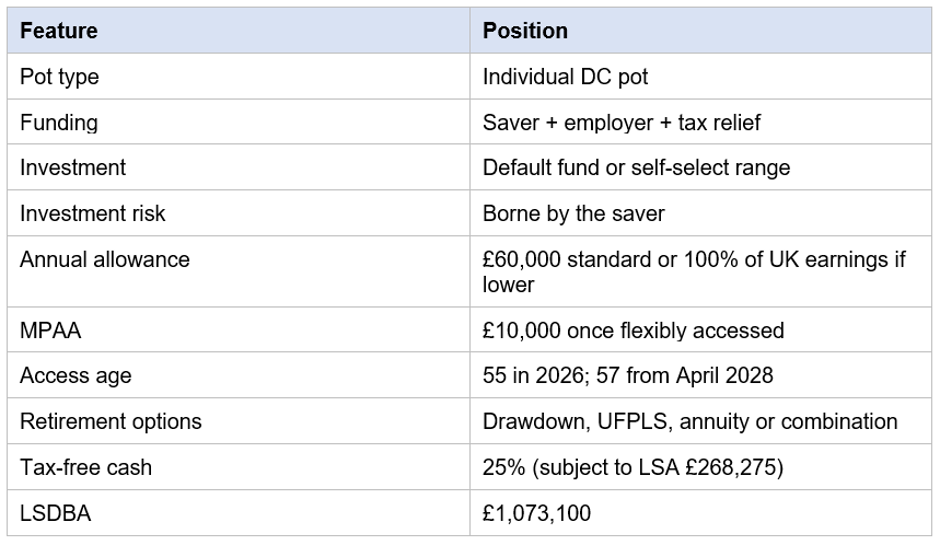

DC pension contributions benefit from UK pension tax relief. The standard annual allowance for 2026/27 is £60,000, with tapering for high earners and a £10,000 MPAA after flexible access. Non-earners can contribute up to £3,600 gross per year. Investment growth inside the wrapper is free from UK income tax and CGT.

Lifetime tax-free cash is capped by the LSA of £268,275 and the LSDBA of £1,073,100 following the abolition of the lifetime allowance from 6 April 2024.

Accessing a DC Pension

DC pensions can be accessed from the normal minimum pension age — 55 in 2026, rising to 57 from 6 April 2028. Pension freedoms in April 2015 introduced wide flexibility:

- Flexi-access drawdown — take up to 25% tax-free and draw the rest as Taxable Income.

- UFPLS — take ad-hoc lump sums where each is 25% tax-free and 75% taxable.

- Annuity purchase — exchange the pot for a guaranteed income for life or for a fixed term.

- Leaving the pot invested — continue to grow the pension before drawing benefits.

- Mix and match — combine partial annuity, drawdown and lump sums.

The Money Purchase Annual Allowance

Once a saver flexibly accesses a DC pension by taking taxable income, the £10,000 Money Purchase Annual Allowance (MPAA) replaces the standard annual allowance for further DC contributions. Carry forward does not apply to the MPAA. Taking only the 25% tax-free cash from flexi-access drawdown does not normally trigger the MPAA.

DC Pensions vs DB Pensions

A defined benefit (DB) pension promises a specific income in retirement based on salary and service. The employer takes the investment and longevity risk. A DC pension does not promise income — the saver takes the risk and the upside. DB schemes are now rare in the private sector but remain common in the public sector.

Charges in a DC Pension

Charges depend on the wrapper. Workplace default funds in qualifying schemes are capped at 0.75% per year on fund management costs. Personal pensions, SIPPs and stakeholder pensions have varied charging structures — flat fees, percentages or capped charges. Even small differences in charges compound over decades.

Death Benefits

DC pensions can pay valuable death benefits to nominated beneficiaries. Death before age 75 normally allows benefits to pass tax-free up to the LSDBA; death after 75 means beneficiaries pay income tax at their marginal rate. The IHT treatment of pension death benefits is under government review and savers should follow current GOV.UK guidance.

Risks to Weigh

- Investment risk — the pot can fall as well as rise.

- Longevity risk — running out of money in later life if withdrawals are too high.

- Sequence-of-returns risk — early losses in drawdown can damage long-term income.

- Inflation risk — fixed contributions need to grow with inflation to keep value.

- Transfer risk — moving between DC schemes can lose features such as guarantees.

- Scam risk — pension scams have repeatedly targeted DC pension savers.

Investing Inside a DC Pension

Most workplace DC schemes invest in a default fund chosen by the trustees or provider. Defaults are typically diversified strategies designed for the average member, often using lifestyle or target-date approaches that gradually de-risk as the member approaches retirement. Some members prefer to self-select funds within the scheme's range, choosing higher-Equity, ethical or income-orientated strategies depending on their goals.

In SIPPs, investment choice is much wider — funds, shares, ETFs, investment trusts, gilts and corporate bonds, plus commercial property in full SIPPs. The wider choice comes with more responsibility for asset allocation, Diversification and ongoing review. Engaged investors often build a low-cost diversified portfolio across global equities and bonds; less engaged savers may benefit from a default or 'ready-made' portfolio.

Reviewing a DC Pension

DC pensions benefit from regular review. A useful discipline is an annual check covering: current pot value, contribution levels, employer matching where available, charges, investment performance against expectations and beneficiary nominations. Many UK savers schedule the review around the end of the tax year to coordinate with allowance planning and any Self Assessment claims. Free guidance via MoneyHelper supports the basic review; regulated advice helps with significant decisions.

Combining DC Pensions

Many UK workers accumulate several DC pots over a career. Consolidation into a single pension — often a SIPP — can simplify management and reduce charges, but advice is recommended to avoid losing valuable features. Active workplace pensions are usually best left in place because of ongoing employer contributions.

How DC Pensions Fit with the State Pension

DC pensions sit alongside the UK state pension in most retirement plans. The state pension is rising from 66 to 67 between April 2026 and April 2028 and is currently legislated to rise to 68 between 2044 and 2046 (subject to review). The state pension provides a baseline income; DC pensions provide flexibility on top, supporting the saver's chosen lifestyle. Coordinating DC withdrawals with state pension timing can support tax-efficient retirement income.

Tracking Old DC Pensions

After several Job moves, many UK workers have multiple DC pension pots from former employers. Statements may be sent to old addresses, and the saver may have lost track of providers altogether. The Pension Tracing Service, provided through MoneyHelper, can help locate forgotten pots. Once located, savers can choose to leave them in place, transfer to a current workplace pension, or consolidate into a SIPP after taking advice.

Where to Get Help

MoneyHelper (Money and Pensions Service) provides free guidance on UK pensions. Pension Wise, through MoneyHelper, offers free appointments for over-50s with DC pensions to discuss retirement options. The Pension Tracing Service helps find lost pots. For personalised recommendations, a regulated financial adviser should be engaged.

DC Pension Snapshot (2026/27)

Key features of a UK defined contribution pension in 2026/27.

Key Takeaways

- A DC pension is the most common UK pension type today.

- It builds an individual pot from contributions, employer matching and investment growth.

- The saver bears the investment and longevity risk.

- Tax relief on contributions and tax-free growth are core benefits.

- Pension freedoms in 2015 gave wide flexibility on retirement income.

- DC pensions are different from defined benefit pensions.

- Free guidance via MoneyHelper and regulated advice both help.

Please wait processing your request...

Please wait processing your request...