What Readers Need to Know

- A defined benefit pension promises a specific retirement income based on salary and service.

- The employer takes the Investment and longevity risk, not the saver.

- Public sector and some longer-serving private sector employees often have DB pensions.

- Transferring out of a DB pension exchanges guaranteed income for a one-off cash sum.

- The Pension Protection Fund provides compensation if a DB scheme cannot meet its commitments.

Introduction

Defined benefit pensions — once the standard UK workplace pension — have become rarer over the past two decades. They remain widely used in the public sector and still provide income for millions of UK retirees from older private sector schemes.

This article introduces defined benefit and final salary pensions for UK readers in the 2026/27 tax year. It is general information and does not constitute personal advice. Anyone considering a DB pension decision — particularly a transfer out — should speak with a regulated financial adviser with DB transfer permissions.

A Defined Benefit Pension in One Sentence

A defined benefit pension is a UK pension scheme that promises a specific retirement income to members, calculated by a formula based on salary and service, with the employer responsible for funding the promise.

How a DB Pension Calculates Income

The classic formula is: (Pensionable salary) x (Years of service) x (Accrual rate). The accrual rate is set by the scheme — common rates include 1/60, 1/80 and 1/100. For example, a member with 30 years of service in a 1/60 final salary scheme would receive 30/60 = 50% of pensionable salary as an annual pension for life.

Final salary schemes use salary at or near retirement. Career average revalued Earnings (CARE) schemes use the average salary over service, revalued for Inflation. Each year of service builds up a separate slice of pension, indexed forward to retirement.

Why DB Pensions Are Valuable

- Guaranteed income for life — predictable retirement income.

- No investment risk for the member — the employer bears market and longevity risk.

- Often inflation-linked — many DB pensions increase each year in line with inflation, capped at a defined rate.

- Spouse and dependant pensions — many DB schemes pay reduced pensions to surviving partners and children.

- Death-in-service benefits — DB schemes often pay lump sums and dependant pensions if a member dies in service.

Public Sector vs Private Sector

Public sector DB pensions — for teachers, NHS staff, civil servants, armed forces, police and others — remain widely available to new and existing employees. Most have moved from final salary to CARE structures over recent years, but the underlying DB promise remains.

In the private sector, DB schemes have largely been closed to new members and increasingly to future accrual since the 2000s, driven by rising costs and accounting rules. Many private sector employees still have deferred DB benefits from earlier employers.

Tax Treatment

DB pensions attract the same tax framework as other UK registered pensions. Contributions during accrual are not income-taxed; the calculated benefit is taxed as income in retirement. A tax-free lump sum of typically 25% of the value (calculated through the scheme's commutation Factor) is normally available, subject to the LSA of £268,275. The LSDBA of £1,073,100 caps the wider lifetime tax-free amount, including on death.

The Annual Allowance and DB Pensions

Annual allowance calculations differ for DB pensions. The 'pension input amount' is based on the change in the value of accrued benefits between the start and end of the tax year, using a standard multiplier (currently 16 times the change in pension plus the change in any separate lump sum). Tapering for high earners and the MPAA (where flexibly accessed DC pensions are in play) can affect DB members.

Taking a DB Pension

DB pensions are usually drawn at the scheme's 'normal retirement age', which may differ from the saver's preferred date. Early or late retirement is normally possible, with the income adjusted by 'actuarial factors' set by the scheme. Many DB schemes also offer the option to exchange (commute) part of the pension for a tax-free lump sum at retirement.

Transferring Out of a DB Pension

A DB pension can usually be transferred to a DC scheme (such as a SIPP) by exchanging the future income for a 'cash equivalent transfer value'. The transfer value can look attractive but the loss of guaranteed inflation-linked income is permanent.

UK rules require regulated advice for DB transfer values above £30,000. The FCA's default position is that DB transfers are not in the member's best interests unless the case for transfer is clear. Many advisers carry a 'preserve the DB' default. Several DB transfers in recent years have been the subject of high-profile FCA enforcement.

The Pension Protection Fund

The Pension Protection Fund (PPF) protects members of UK private sector DB pension schemes whose sponsoring employer becomes insolvent and cannot fund the promised benefits. The PPF takes over eligible schemes and pays compensation — typically 100% of benefits for members already at the scheme's normal retirement age and 90% of benefits, subject to a cap, for those who have not yet reached it. The PPF is funded by levies on DB schemes.

Risks to Weigh

- Transfer risk — exchanging guaranteed income for a cash value is permanent.

- Scheme funding risk — private sector DB schemes can become underfunded; the PPF provides a backstop but not at 100% for active members.

- Inflation risk — caps on DB increases mean very high inflation can still erode real income.

- Scam risk — DB transfers have been targeted by pension scammers; the FCA's ScamSmart resource is essential reading.

- Tax risk — pension tax rules and allowances can change.

The Move from Final Salary to Career Average

Many UK public sector DB schemes — for teachers, NHS staff, civil servants and others — moved from final salary structures to career average revalued earnings (CARE) structures over the past decade. Under a CARE scheme, each year of service builds up a pension based on that year's salary, with the resulting slice revalued each year by an index (often CPI plus a Margin) until benefits are drawn.

The move was driven by concerns over rising costs, longevity and fairness across long-serving employees. CARE schemes remain defined benefit — the income is still guaranteed — but the formula is different. Members with both final salary and CARE accrual have multiple slices of pension that combine on retirement.

Inflation Increases on DB Pensions

Most UK DB pensions provide some form of inflation linkage during retirement. Public sector schemes typically index by CPI; many private sector schemes use CPI or RPI subject to annual caps (commonly 2.5% or 5%). High inflation can erode real income where caps are tight. Members should check the specific increase rules in their scheme.

Some legacy schemes also distinguish between pre-1997, 1997-2005 and post-2005 accrual, with different statutory minimum increases applying to each. This can make individual DB pensions complex to interpret, particularly for long-serving members.

Combining DB and DC Pensions

Many UK savers have both DB and DC pensions — perhaps a frozen DB scheme from an earlier employer and a current DC workplace pension. Retirement Planning should consider both: when to draw each, how they interact with the state pension and tax bands, and how to coordinate income.

Where to Get Help

MoneyHelper (Money and Pensions Service) provides free guidance on UK pensions, including DB schemes. The Pensions Regulator publishes information on DB scheme funding and the PPF. For DB transfer decisions, only an FCA-authorised adviser with the relevant DB transfer permission can provide advice. The FCA Register confirms permissions.

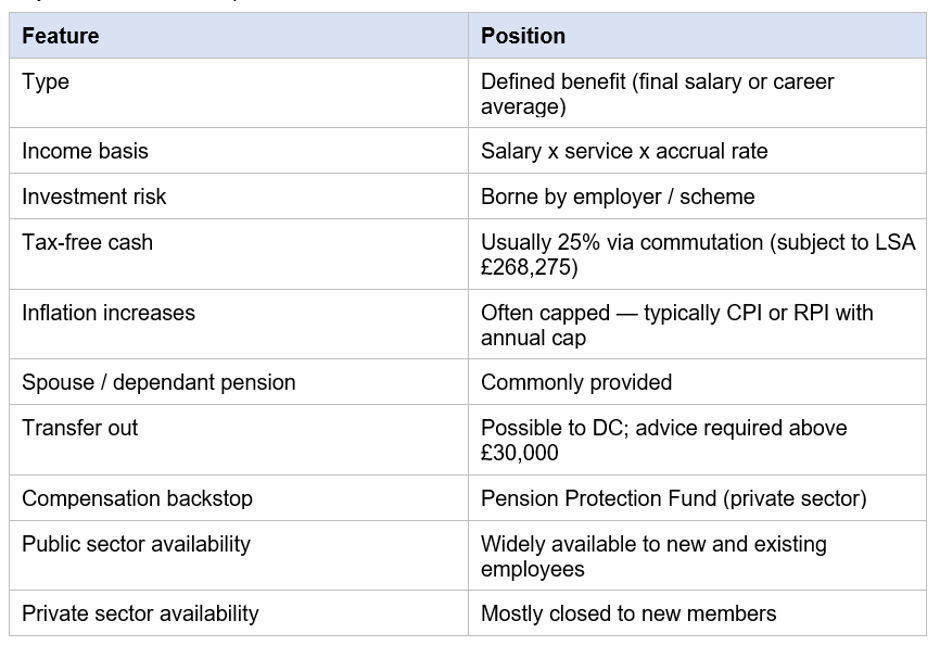

Defined Benefit Pension Snapshot (2026/27)

Key features of UK DB pensions in 2026/27.

Key Takeaways

- A DB pension promises a defined retirement income, calculated by a formula.

- The employer takes the investment and longevity risk.

- Public sector DB pensions remain widely available; private sector DB schemes are increasingly closed.

- DB transfers exchange guaranteed income for a one-off cash value — usually a permanent decision.

- The Pension Protection Fund provides compensation if a private DB scheme fails.

- DB transfers above £30,000 require regulated advice.

- Specialist advice is essential before any DB decision.

Please wait processing your request...

Please wait processing your request...